Define the second order properties of a random walk

Define the backward shift operator

Use the backward shift operator to state a random walk as a sequence of white noise realizations

Define a random walk with drift

Simulate realizations from basic time series models in R

Simulate a random walk

Plot a random walk

Fit time series models to data and interpret fitted parameters

Motive the need for differencing in time series analysis

Define the difference operator

Explain the relationship between the difference operator and the backward shift operator

Test whether a series is a random walk using first differences

Explain how to estimate a random walk with increasing slope using Holt-Winters

Estimate the drift parameter of a random walk

Preparation

Read Sections 4.3.6-4.3.7 and 4.4

Learning Journal Exchange (10 min)

Review another student’s journal

What would you add to your learning journal after reading another student’s?

What would you recommend the other student add to their learning journal?

Sign the Learning Journal review sheet for your peer

Packages

# Extra packages this lessonpacman::p_load( plotly, # plot_ly() tidyquant # tq_get())

pacman::p_load( tidyverse, # ggplot, mutate(), cleaning... tsibble, # as_tsibble() fable, # model(...), forecast(), tidy(), glance()... feasts, # ACF(), PACF() ggtime, # autoplot() for tsibbles patchwork, # + and / for ggplots rio # import())

Note: the plotly package causes conflicts with tidyverse. Click below if you have code issues.

If you have code issues

# The plotly package creates conflicts with functions from the tidyverse package# This makes sure it defaults to the tidyverse version# Alternatively, using dplyr::select(), or loading plotly before pacman resolves the issuepacman::p_load(conflicted)conflict_prefer("select", "dplyr")conflict_prefer("filter", "dplyr")conflict_prefer("lag", "dplyr")conflict_prefer("layout", "plotly")

Class Activity: Differencing a Time Series (15 min)

Example: McDonald’s Stock Prices

Computing the difference between successive terms of a random walk leads to a discrete white noise series.

In many cases, differencing sequential terms of a non-stationary process can lead to a stationary process of differences. We can use the code below to obtain the daily closing stock prices for any publicly-traded company.

Show the code

library(tidyquant)# Set symbol and date rangesymbol <-"MCD"company <-"McDonald's"date_start <-"2020-07-01"date_end <-"2024-01-01"# Fetch stock prices (can be used to get new data)stock_df <-tq_get(symbol, from = date_start, to = date_end, get ="stock.prices")# Transform data into tsibblestock_ts <- stock_df %>%mutate(dates = date, value = adjusted ) %>% dplyr::select(dates, value) %>%as_tibble() %>%arrange(dates) |>mutate(diff = value -lag(value)) |>as_tsibble(index = dates, key =NULL)

The time plot in Figure 1 presents the closing price of McDonald’s stock from 01/07/2020 to 01/01/2024. Figure 2 gives the differences in the closing prices of the stock as a time series.

Show the code

plot_ly(stock_ts, x =~dates, y =~value, type ='scatter', mode ='lines') %>%layout(xaxis =list(title =paste0("Dates (", format(ymd(date_start), "%d/%m/%Y"), " to ", format(ymd(date_end), "%d/%m/%Y"), ")" ) ),yaxis =list(title ="Closing Price (US$)"),title =paste0("Time Plot of ", symbol, " Daily Closing Price") )

Figure 1: Plot of the daily closing price of the stock

Show the code

# Generate time series plot using plot_lyplot_ly(stock_ts, x =~dates, y =~diff, type ='scatter', mode ='lines') %>%layout(xaxis =list(title =paste0("Dates (", format(ymd(date_start), "%d/%m/%Y"), " to ", format(ymd(date_end), "%d/%m/%Y"), ")" ) ),yaxis =list(title ="Closing Price (US$)"),title =paste0("Difference of ", symbol, " Daily Closing Price") )

Figure 2: Plot of the stock price differences

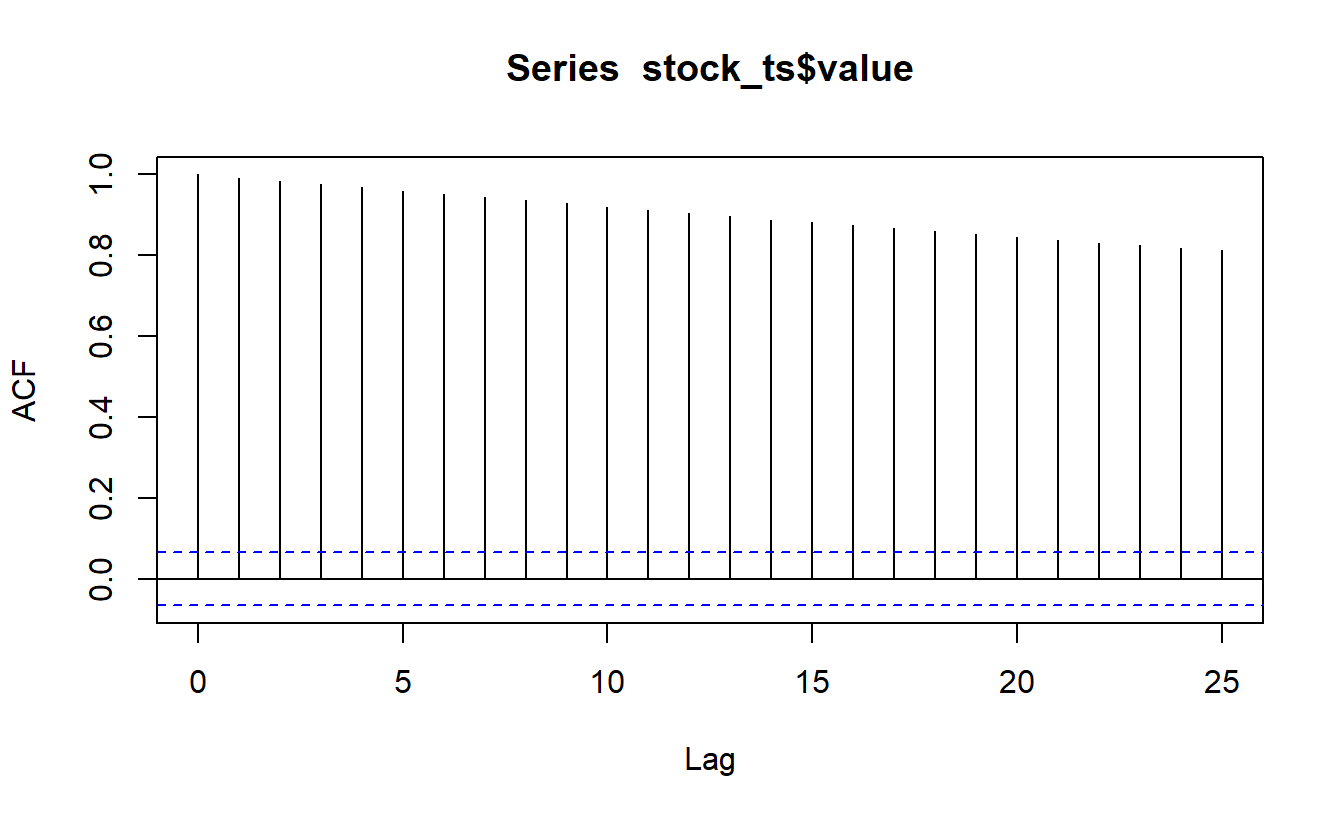

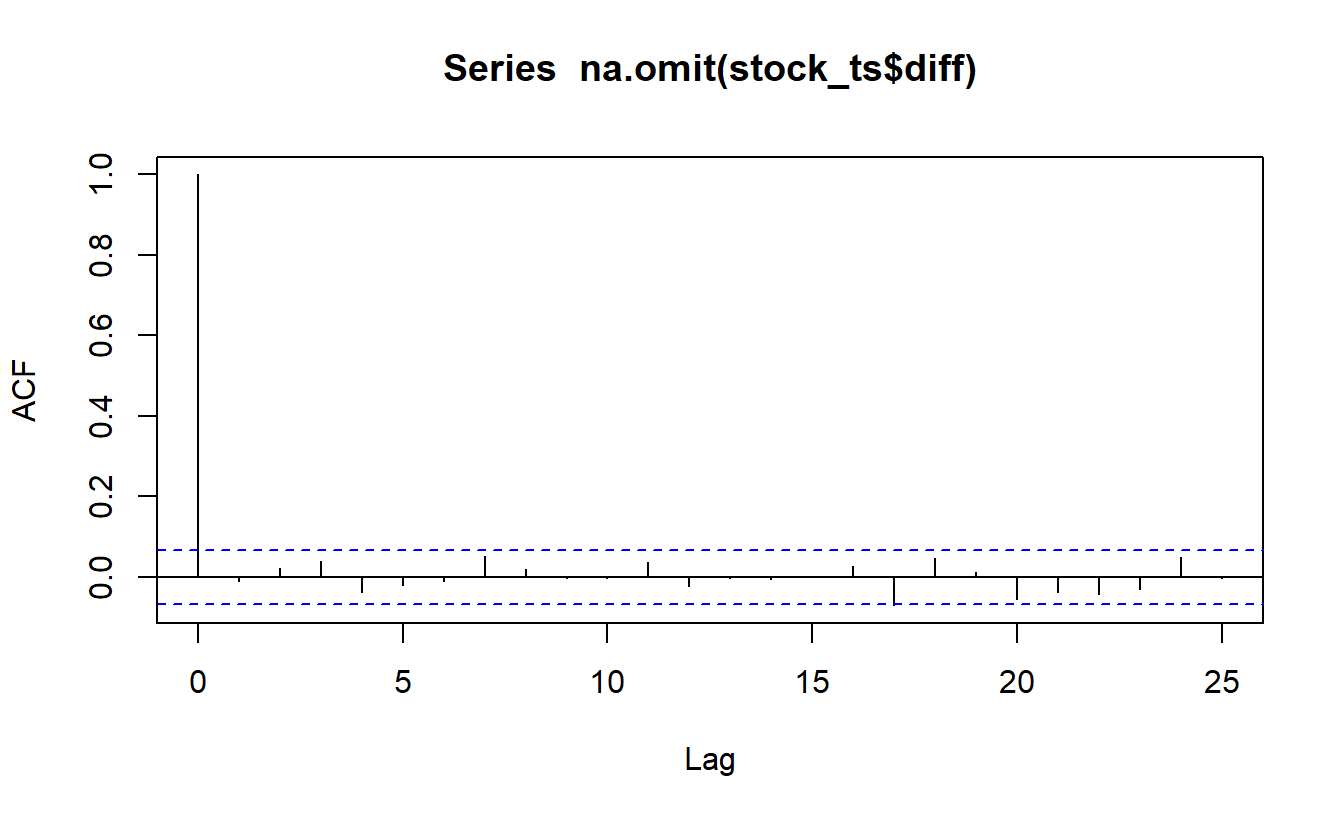

Figure 3 is the correlogram for the original McDonald’s stock price time series. Figure 4 gives the correlogram for the differences in successive closing stock prices.

Show the code

acf(stock_ts$value, plot=TRUE, type ="correlation", lag.max =25)

Figure 3: Correlogram of the stock prices

Show the code

acf(stock_ts$diff |>na.omit(), plot=TRUE, type ="correlation", lag.max =25)

Figure 4: Correlogram of the stock prices

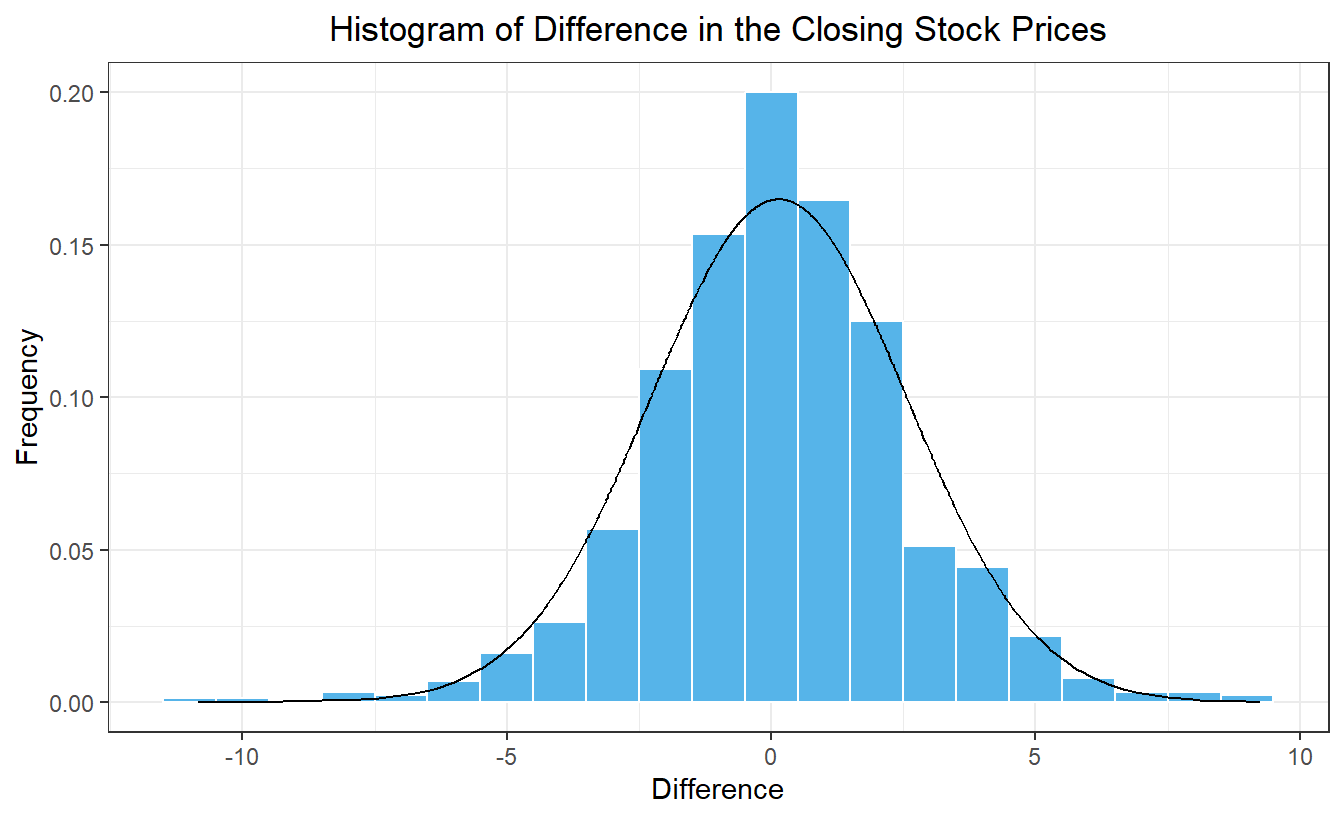

Figure 5 is a histogram of the differences. On the right, we give the variance of the differences in the stock prices. This is a simple measure of the volatility of the stock, or in other words, how much the price changes in a day.

Show the code

# Histogram of differences in stock pricesstock_ts |>mutate(density =dnorm(diff, mean(stock_ts$diff, na.rm =TRUE), sd(stock_ts$diff, na.rm =TRUE)) ) |>ggplot(aes(x = diff)) +geom_histogram(aes(y =after_stat(density)),color ="white", fill ="#56B4E9", binwidth =1) +geom_line(aes(x = diff, y = density)) +theme_bw() +labs(x ="Difference",y ="Frequency",title ="Histogram of Difference in the Closing Stock Prices" ) +theme(plot.title =element_text(hjust =0.5) )

Figure 5: Histogram of the stock price differences

The variance of the differences is 5.388.

Notice that the values in the correlogram of the stock prices start at 1 and slowly decay as \(k\) increases. There are no significant autocorrelations in the differenced values. This is exactly what we would expect from a random walk. It is also interesting that the differences are nearly normally distributed and uncorrelated.

Defintion of the Difference Operator

Differencing nonstationary time series often leads to a stationary series, so we will define a formal operator to express this process.

NoteDefinition of the Difference Operator

The difference operator, \(\nabla\), is defined as:

To see what this expression gives us, note that \(\nabla\) gives a new time series that is comprised of the differences between successive terms of the original time series. The operator \(\nabla^2\) generates a time series that is comprised of the differences between successive terms of the differenced time series. It is the difference of the differences, or the second difference.

Fill in the missing steps: \[\begin{align*}

\nabla^2 x_8 &= (1-\mathbf{B} )^2 x_8 \\

&= (1-\mathbf{B} ) \left[ (1-\mathbf{B} ) x_8 \right] \\

& ~~~~~~~~~~~~~~~~~~~~~~ ⋮ \\

&= (x_8-x_7)-(x_7-x_6)

\end{align*}\] and check that this is equal to the last term in the sequence of second differences.

$$t$$

$$x_t$$

$$\nabla x_t$$

$$\nabla^2 x_t$$

1

5

2

10

3

13

4

8

5

4

6

3

7

9

8

2

Small-Group Activity: Computing Differences

The difference operator can be helpful in identifying the functional underpinnings of a trend. If a function is linear, then the first differences of equally-spaced values will be constant. If a function is quadratic, then the second differences of equally-spaced values will be constant. If a function is cubic, then the third differences of equally-spaced values will be constant, and so on.

In this activity, you will apply what you have learned to a new stock.

TipCheck Your Understanding

Modify the code used to get the prices of McDonald’s stock to download closing stock prices for a different publicly-traded company over a time period of your choice.

Show the code

# Set symbol and date rangesymbol <-"MCD"# Stock trading symbol for McDonald'sdate_start <-"2020-07-01"date_end <-"2024-01-01"# Fetch stock prices (can be used to get new data)stock_df <-tq_get(symbol, from = date_start, to = date_end, get ="stock.prices")# Transform data into tsibblestock_ts <- stock_df %>%mutate(dates = date, value = adjusted ) %>% dplyr::select(dates, value) %>%as_tibble() %>%arrange(dates) |>mutate(diff = value -lag(value)) |>as_tsibble(index = dates, key =NULL)plot_ly(stock_ts, x =~dates, y =~value, type ='scatter', mode ='lines') %>%layout(xaxis =list(title =paste0("Dates (", format(ymd(date_start), "%d/%m/%Y"), " to ", format(ymd(date_end), "%d/%m/%Y"), ")" ) ),yaxis =list(title ="Closing Price (US$)"),title =paste0("Time Plot of ", symbol, " Daily Closing Price") )# Generate time series plot using plot_lyplot_ly(stock_ts, x =~dates, y =~diff, type ='scatter', mode ='lines') %>%layout(xaxis =list(title =paste0("Dates (", format(ymd(date_start), "%d/%m/%Y"), " to ", format(ymd(date_end), "%d/%m/%Y"), ")" ) ),yaxis =list(title ="Closing Price (US$)"),title =paste0("Difference of ", symbol, " Daily Closing Price"))# Autocorrelation function for stock pricesacf(stock_ts$value, plot=TRUE, type ="correlation", lag.max =25)# Autocorrelation function for differencesacf(stock_ts$diff |>na.omit(), plot=TRUE, type ="correlation", lag.max =25)# Histogram of differences in stock pricesstock_ts |>mutate(density =dnorm(diff, mean(stock_ts$diff, na.rm =TRUE), sd(stock_ts$diff, na.rm =TRUE)) ) |>ggplot(aes(x = diff)) +geom_histogram(aes(y =after_stat(density)),color ="white", fill ="#56B4E9", binwidth =1) +geom_line(aes(x = diff, y = density)) +theme_bw() +labs(x ="Difference",y ="Frequency",title ="Histogram of Difference in the Closing Stock Prices" ) +theme(plot.title =element_text(hjust =0.5) )# Variance of the differencesvar(stock_ts$diff, na.rm =TRUE)|>round(3)

Do the following.

Indicate which company you have chosen, the stock symbol, and the time period.

Create a time plot of the daily closing stock prices.

Produce a time plot of the differences in the daily closing stock prices.

Create a correlogram of the stock prices

Create a correlogram of the differences

Generate a histogram of the difference in the stock prices and superimpose the corresponding normal density.

Compute the variance of the differences

Compare your results with those from the other teams of students.

Optional Activity: Integrated Autoregressive Model (10 min)

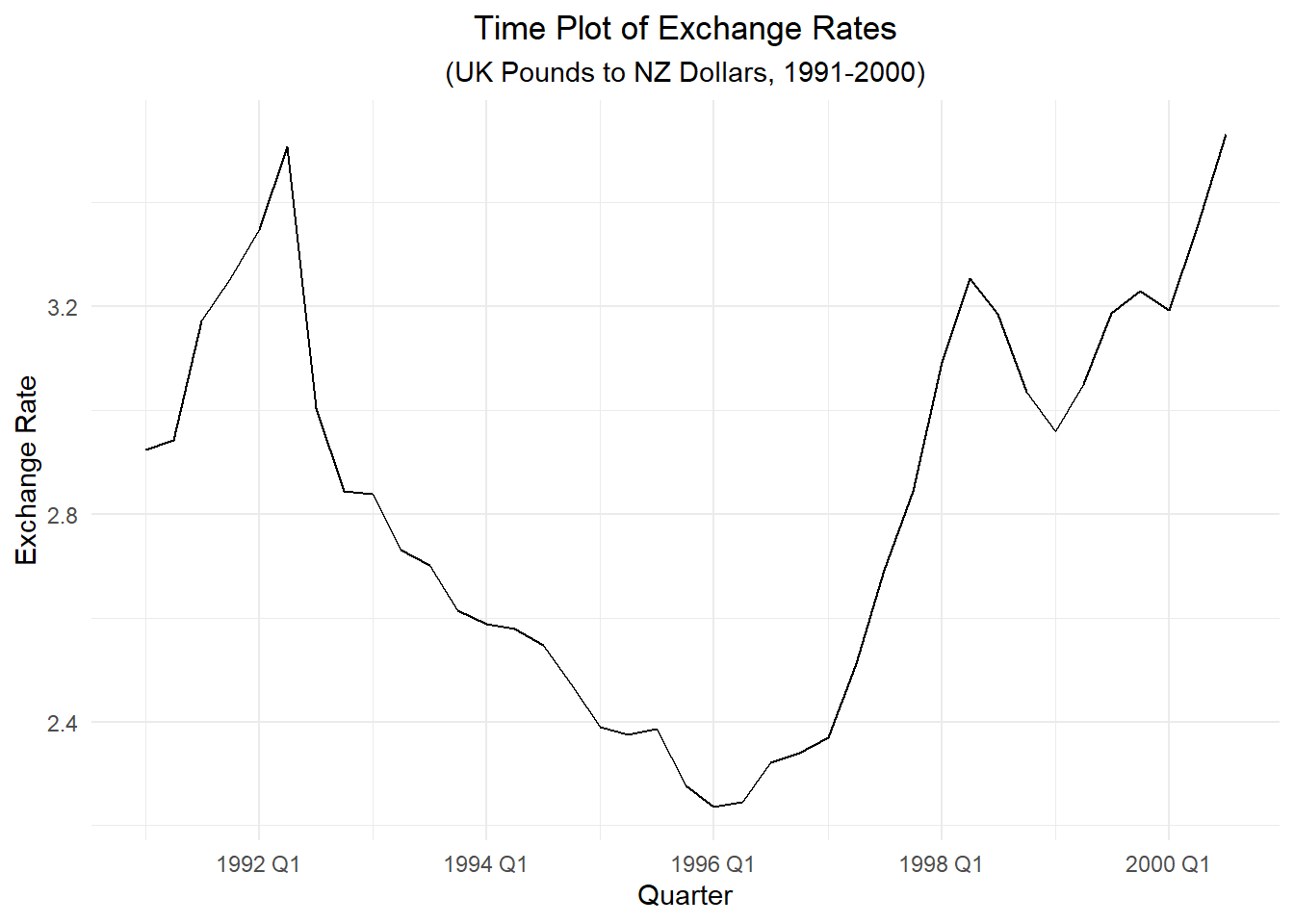

Consider the correlogram of the first differences in the exchange rates.

Show the code

z_ts |>mutate(diff = xrate -lag(xrate)) |>ACF(diff) |>autoplot() +labs(title =paste("Correlogram of First Differences of Exchange Rates"),x ="Lag",y ="Difference" ) +theme_minimal() +theme(plot.title =element_text(hjust =0.5))

Notice that for a lag of \(k=1\), there is still a significant autocorrelation in the differences. This suggests that a more sophisticated model might be necessary. Note that for \(k>1\), the autocorrelations in the differences are not significant. So, a random walk might be a good model for the differences.

We can add an additional terms to the random walk model using the slope estimate from Holt-Winters. Assume the next term in the time series can be modeled as the previous term plus an estimated slope plus a white noise component. This gives us the first equation below. We will use the Holt-Winters update equation to estimate the slope. This is the second equation below.

Note: The value of beta obtained using the feasts model() statement is 0.155. This is slightly different than the value obtained using the base R HoltWinters() command: 0.167. This is likely due to differences in the implementation of the Holt-Winters model, including the initial conditions.

Start with the fitted system of equations \[

\begin{cases}

~~~x_t = x_{t-1} + b_{t-1} + w_t \\

b_{t-1} = 0.155 \left( x_{t-1} - x_{t-2} \right) + 0.845 ~ b_{t-2}

\end{cases}

\] Show that it can be written as \[

\left( 1 - \mathbf{B})^2 x_t = (1 - 0.845 \mathbf{B} \right) w_t

\] by completing the following steps.

Write the system of equations in terms of the backward shift operator.

Solve for the term \(\mathbf{B} b_t\) in the first equation and substitute the resulting expression into the second equation.

Combine like terms and simplify.

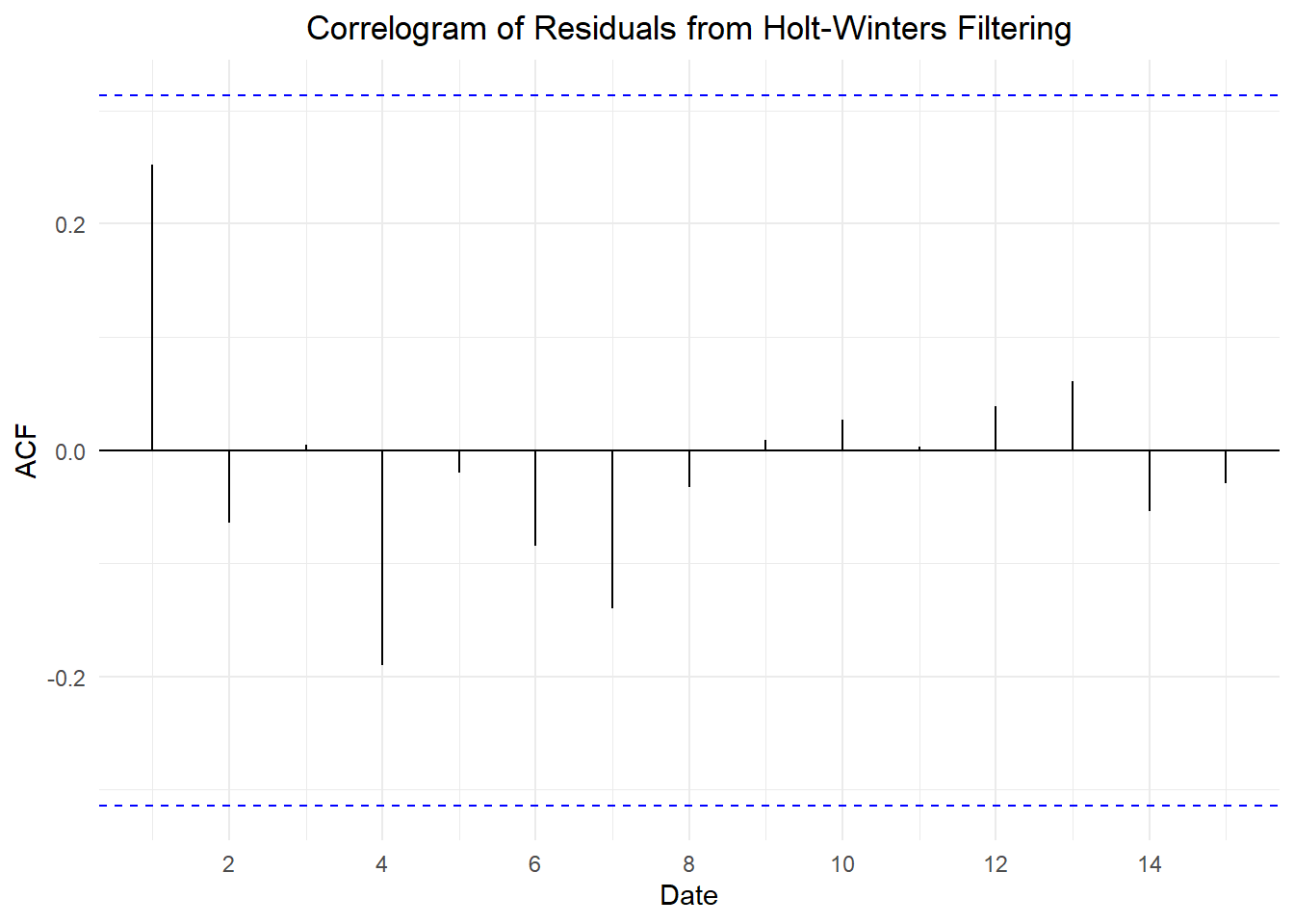

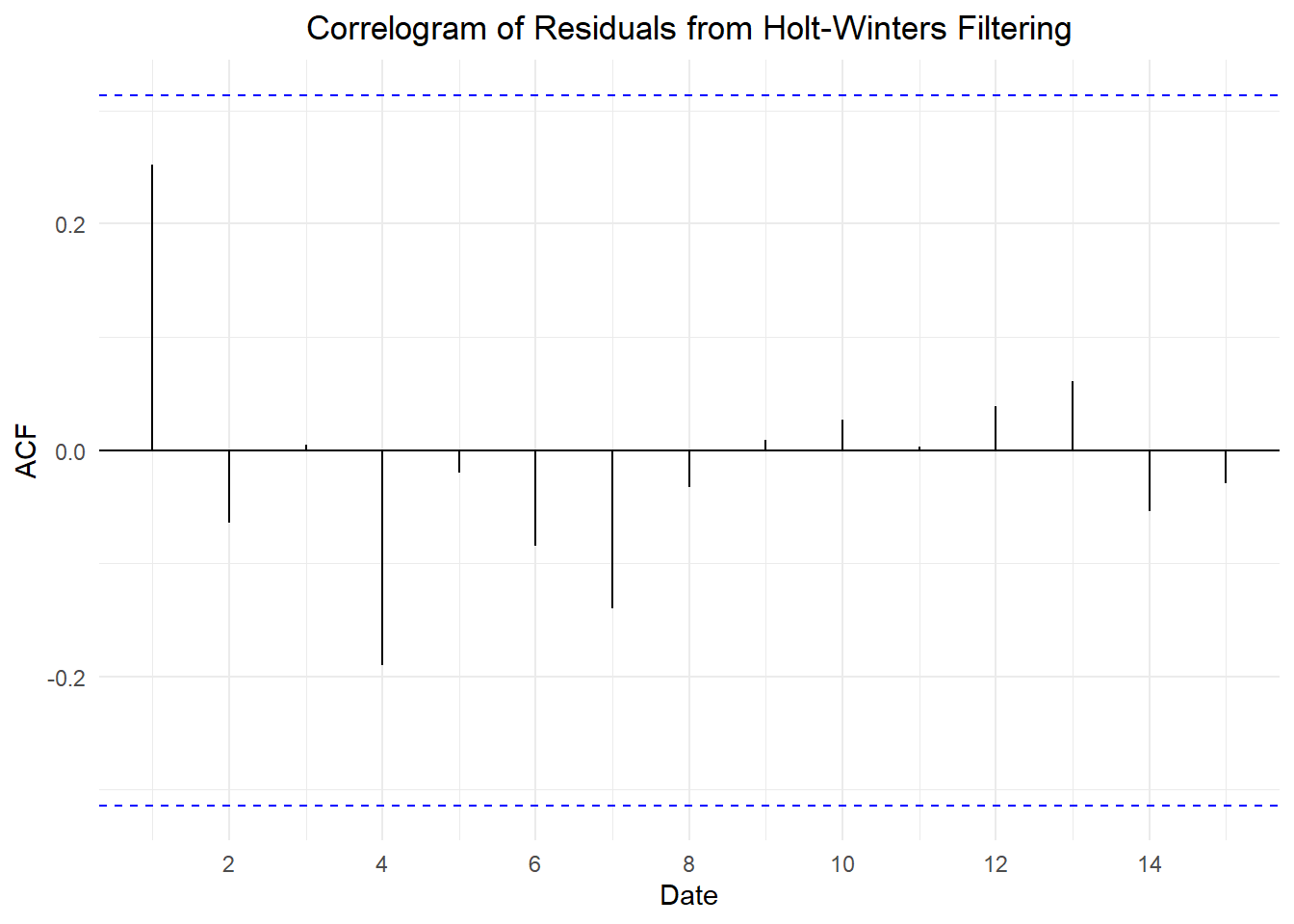

We will examine the residuals from the Holt-Winters model:

Show the code

z_hw <- z_model |>residuals()ACF(z_hw, .resid) |>autoplot() +labs(title =paste("Correlogram of Residuals from Holt-Winters Filtering"),x ="Date",y ="ACF" ) +theme_minimal() +theme(plot.title =element_text(hjust =0.5))

Notice that there are no significant autocorrelations, so we conclude that the Holt-Winters model yields reasonable estimates of the time series.

Class Activity: Random Walk with Drift (15 min)

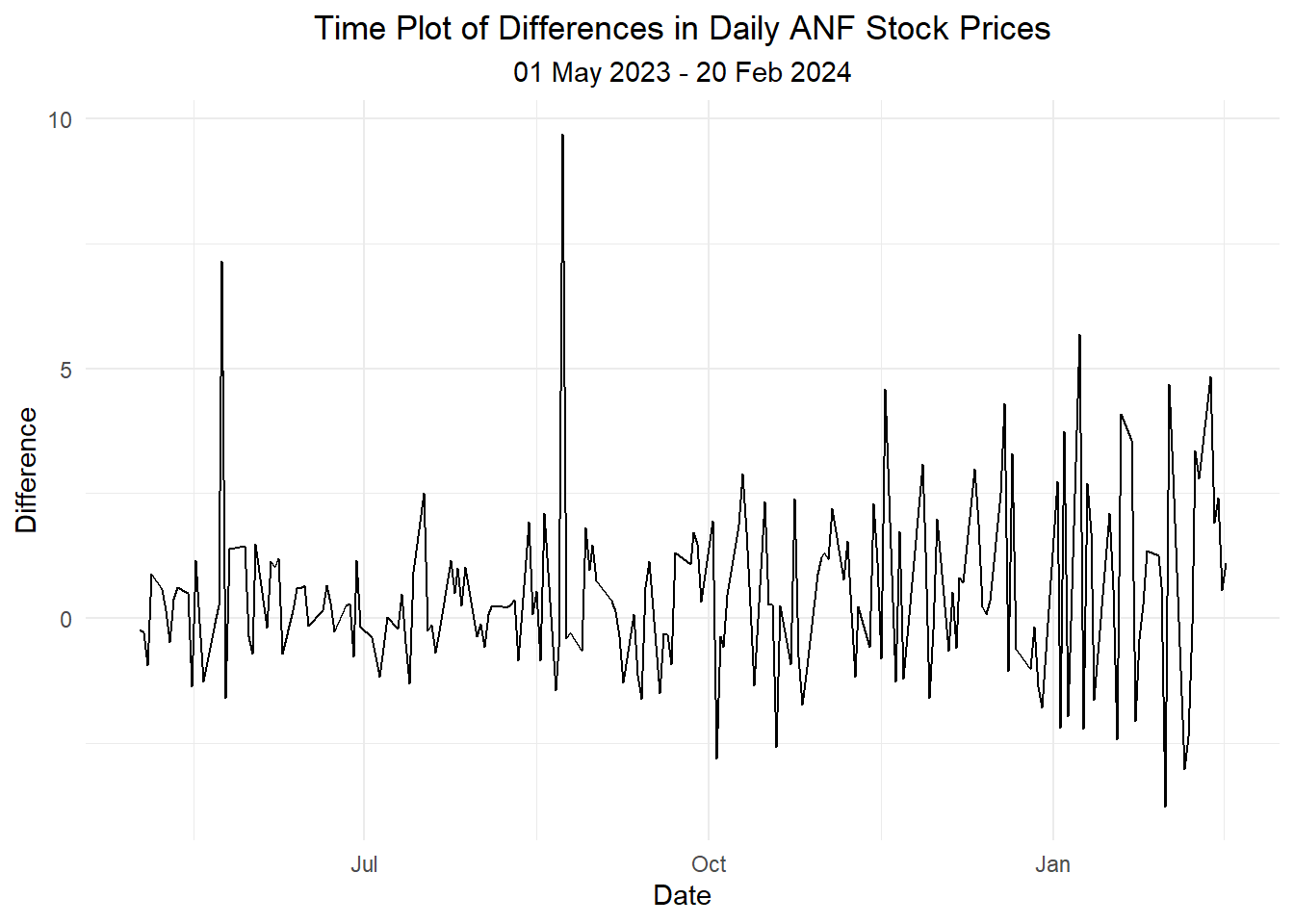

We will now consider the daily closing price of Abercrombie & Fitch stock (Symbol = ANF). Here is a time series plot of the closing stock prices.

Show the code

# Set symbol and date rangesymbol <-"ANF"# Abercrombie & Fitch stock trading symboldate_start <-"2023-05-01"date_end <-"2024-02-20"# Fetch stock pricesdf_stock <-tq_get(symbol, from = date_start, to = date_end, get ="stock.prices")# Transform data into tsibbledf_tsibble <- df_stock |>mutate(dates = date, value = close ) |> dplyr::select(dates, value) |>as_tibble() |>arrange(dates) |>as_tsibble(index = dates, key =NULL)# Generate time series plot using plot_lyplot_ly(df_tsibble, x =~dates, y =~value, type ='scatter', mode ='lines') |>layout(xaxis =list(title ="Date"),yaxis =list(title ="Value"),title =paste0("Time Plot of ", symbol, " Daily Closing Price (", format(ymd(date_start), "%d %b %Y"), " - ", format(ymd(date_end), "%d %b %Y"),")") )

Figure 6: Time plot of the daily prices of ANF stock

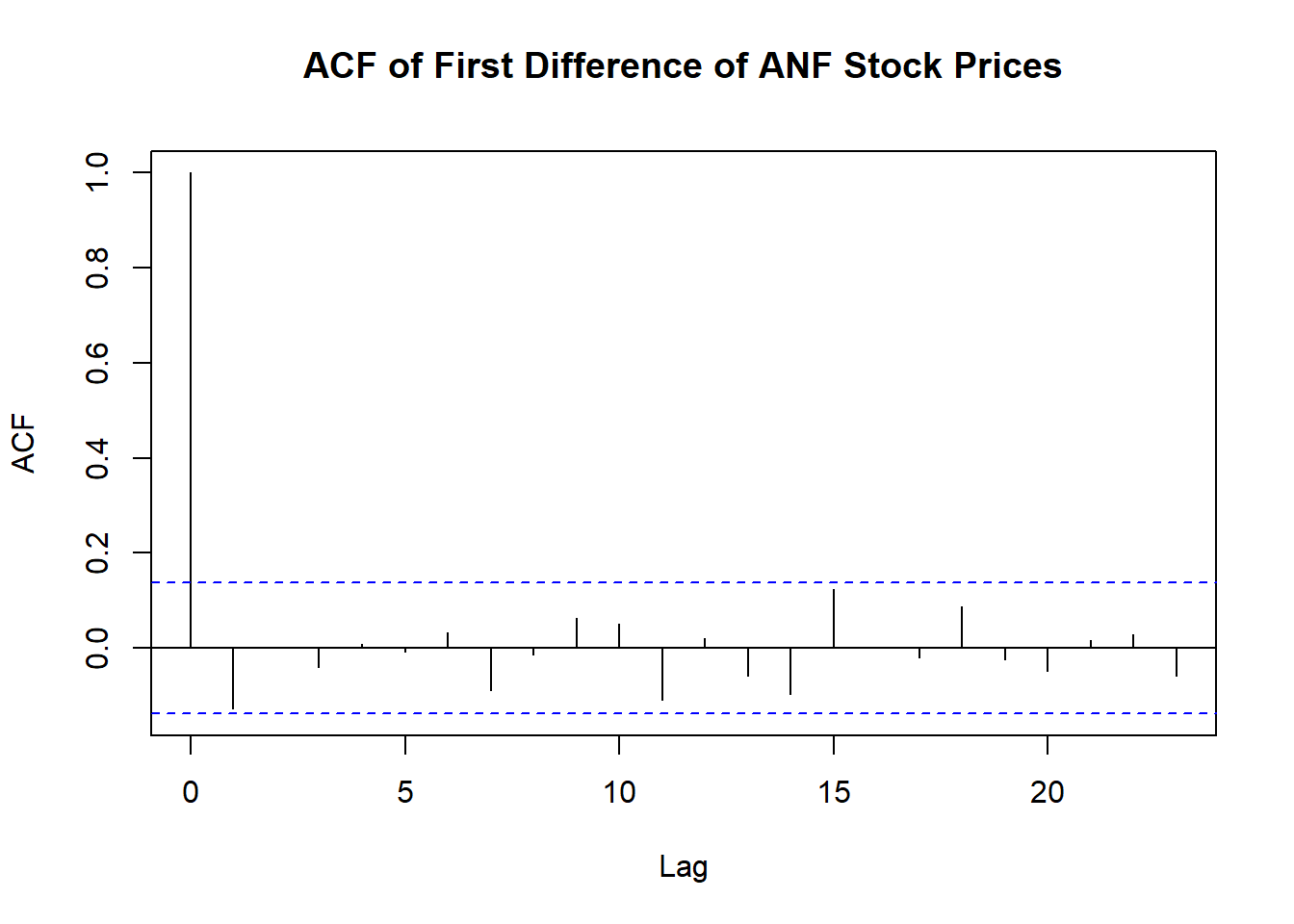

We now generate a time plot and a correlogram of the differences. (No stock prices are recorded on weekends or holidays. Due to the gaps in the data, we will use the base R acf command, rather than the feasts ACF command.)

The mean of the differences is 0.486. The standard deviation of the differences is 1.732. There are 201 differences.

We can use the t-distribution to create a 95% confidence interval for the drift parameter. The critical \(t\) value is given by qt(0.975, df = 201 - 1), yielding a value of \(t^*_{0.975} = 1.972\).

This confidence interval does not contain 0, so we conclude that there is evidence of a positive drift in the price of Abercrombie & Fitch stock over this period.

TipCheck Your Understanding

Use the McDonald’s stock price data to do the following.

What is the estimate of the drift parameter?

What is the standard deviation of the differences?

What is the 95% confidence interval for the drift parameter?

Is there evidence to suggest that the time series can be modeled as a random walk with drift? Why or why not?

\[

\nabla^2 x_8

= \nabla \left( \nabla x_8 \right)

= ( x_8 - x_7 ) - ( x_7 - x_6 )

= (2 - 9) - (9 - 3) \\

= -13

\] This is the value of the last term in the sequence of second differences.

Start with this fitted system of equations. Show that it can be written as \[

(1 - \mathbf{B})^2 x_t = (1 - 0.845) w_t

\] by completing the following steps.

Use the McDonald’s stock price data to do the following.

What is the estimate of the drift parameter?

As seen above, there is no significant autocorrelation in the differences of the McDonald’s stock prices. They appear to be modeled well by white noise.

We now compute the mean and standard deviation of the differences.

mean(stock_ts$diff, na.rm =TRUE)

[1] 0.1347897

What is the standard deviation of the differences?

sd(stock_ts$diff, na.rm =TRUE)

[1] 2.321252

What is the 95% confidence interval for the drift parameter?

The number of differences, \(n\), is given by:

length(stock_ts$diff |>na.omit())

[1] 880

The mean of the differences is 0.135. The standard deviation of the differences is 2.321. There are 880 differences.

We can use the t-distribution to create a 95% confidence interval for the drift parameter. The critical \(t\) value is given by qt(0.975, df = 880 - 1), yielding a value of \(t^*_{0.975} = 1.963\).