pacman::p_load(

tidyverse, # ggplot, mutate(), cleaning...

tsibble, # as_tsibble()

fable, # model(...), forecast(), tidy(), glance()...

feasts, # ACF(), PACF()

ggtime, # autoplot() for tsibbles

patchwork, # + and / for ggplots

rio # import()

)Seasonal ARIMA Models

Chapter 7: Lesson 2

Learning Outcomes

Identify seasonal ARIMA models

- Define seasonal ARIMA models and their notation (p, d, q)(P, D, Q)[m]

- Identify the need for seasonal ARIMA models in time series with seasonal patterns

Apply the fitting procedure for seasonal ARIMA models

- Describe the steps involved in fitting seasonal ARIMA models

- Determine the appropriate order of differencing (d and D) based on ACF/PACF plots

- Select the order of AR and MA terms (p, q, P, Q) using ACF/PACF plots and model selection criteria

Fit seasonal ARIMA models to time series data using R

- Use R to fit seasonal ARIMA models

- Interpret the output for the ARIMA models, including coefficients and model diagnostics

- Forecast future values using the fitted seasonal ARIMA model

Preparation

- Read Section 7.3

Learning Journal Exchange (10 min)

Review another student’s journal

What would you add to your learning journal after reading another student’s?

What would you recommend the other student add to their learning journal?

Sign the Learning Journal review sheet for your peer

Packages

Definition of Seasonal ARIMA (SARIMA) Models

We can add a seasonal component to an ARIMA model. We call this model a Seasonal ARIMA model, or a SARIMA model. We use differencing at a lag equal to the number of seasons, \(s\). This allows us to remove additional seasonal effects that carry over from one cycle to another.

Recall that if we use a difference of lag 1 to remove a linear trend, we introduce a moving average term. The same thing happens when we introduce a difference with lag \(s\). For the lag \(s\) values, we can apply an autoregressive (AR) component at lag \(s\) with \(P\) parameters, an integrated (I) component with parameter \(D\), and a moving average (MA) component with \(Q\) terms. This yields the full SARIMA model.

Looking closely at this model, we can see it is the combination of the ARIMA model \[ \theta_p \left( \mathbf{B} \right) \left( 1 - \mathbf{B} \right)^d x_t = \phi_q \left( \mathbf{B} \right) w_t \] and the same model, after applying a difference across \(s\) seasons \[ \Theta_P \left( \mathbf{B}^s \right) \left( 1 - \mathbf{B}^s \right)^D x_t = \Phi_Q \left( \mathbf{B}^s \right) w_t \]

Special Cases of a Seasonal ARIMA Model

Stationary SARIMA Models

A Simple AR Model with a Seasonal Period of \(s\) Units

\(ARIMA(0,0,0)(1,0,0)_{s}\) is given as

\[ x_t = \alpha x_{t-s} + w_t \] This model would be appropriate for data where there are \(s\) seasons and the value in the season exactly one cycle prior affects the current value. This model is stationary when \(\left| (1/\alpha)^{1/s} \right| > 1\).

Stochastic Trends with Seasonal Influences

Many time series with stochastic trends also have seasonal influences. We can extend the previous model as:

\[ x_t = x_{t-1} + \alpha x_{t-12} - \alpha x_{t-(12+1)} + w_t \]

This is equivalent to \[ \underbrace{\left( 1 - \alpha \mathbf{B}^{12} \right)}_{\Theta_1 \left( \mathbf{B}^{12} \right)} \left( 1 - \mathbf{B} \right) x_t = w_t \]

which is \(ARIMA(0,1,0)(1,0,0)_{12}\).

Note that we could have written this model as: \[ \nabla x_t = \alpha \nabla x_{t-12} + w_t \]

This makes it clear that under this model, the change at time \(t\) depends on the change at the corresponding time in the previous cycle.

Note that \(\left( 1 - \mathbf{B} \right)\) is a factor in the characteristic polynomial, so this model will be non-stationary.

Simple Quarterly Seasonal Moving Average Model (with no Trend)

We can write a simple quarterly seasonal moving average model as

\[ x_t = \underbrace{w_t + \beta w_{t-4}}_{\left( 1 + \beta \mathbf{B}^{4} \right) w_t} \]

This is an \(ARIMA(0,0,0)(0,0,1)_4\) model.

Quarterly Seasonal Moving Average Model with a Stocastic Trend

We can add a stochastic trend to the previous model by including first-order differences:

\[ x_t = x_{t-1} + w_t + \beta w_{t-4} \] This is an \(ARIMA(0,1,0)(0,0,1)_4\) model.

Quarterly Seasonal Moving Average Model where the Seasonal Terms Contain a Stocastic Trend

We can allow the seasonal components to include a stochastic trend. We apply differencing at the seasonal period. This yields the model

\[ x_t = x_{t-4} + w_t + \beta w_{t-4} \]

This is an \(ARIMA(0,0,0)(0,1,1)_4\) process.

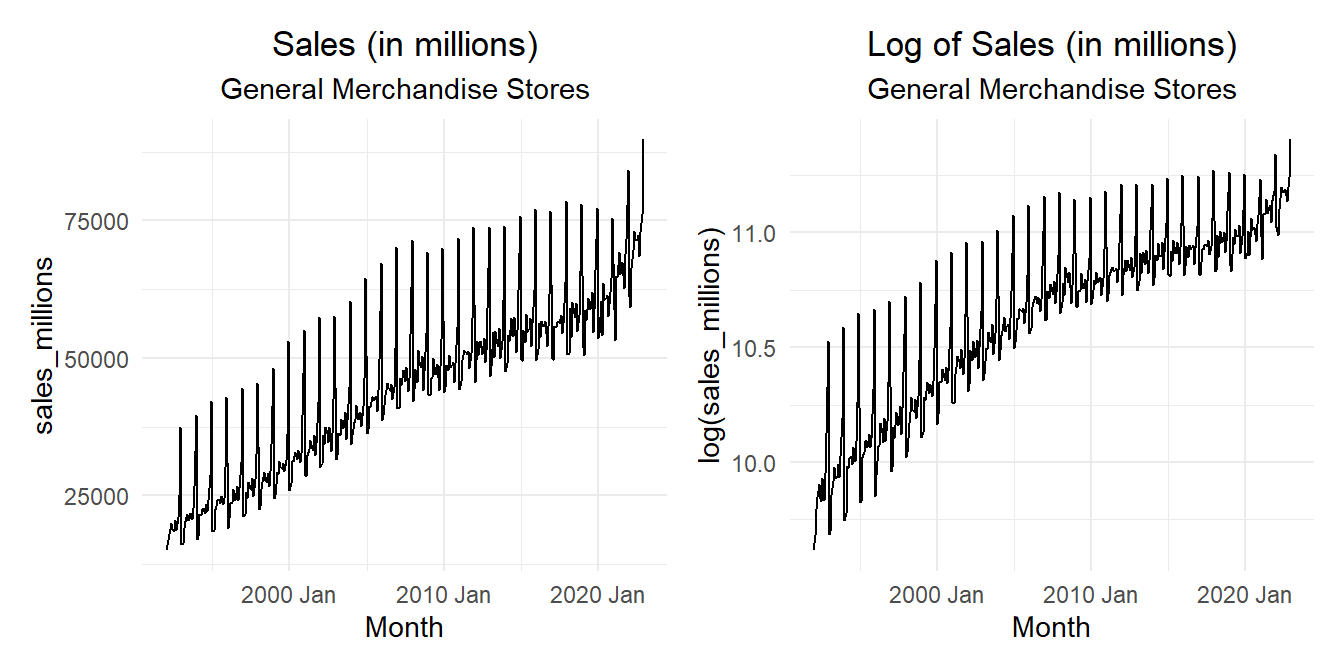

Class Activity: Seasonal ARIMA Models - Retail: General Merchandise Stores (10 min)

Show the code

# Read in retail sales data for "Full-Service Restaurants"

retail_ts <- rio::import("https://byuistats.github.io/timeseries/data/retail_by_business_type.parquet") |>

filter(naics == 452) |>

mutate( month = yearmonth(as_date(month)) ) |>

na.omit() |>

as_tsibble(index = month)

retail_plot_raw <- retail_ts |>

autoplot(.vars = sales_millions) +

labs(

x = "Month",

y = "sales_millions",

title = "Sales (in millions)",

subtitle = "General Merchandise Stores"

) +

theme_minimal() +

theme(

plot.title = element_text(hjust = 0.5),

plot.subtitle = element_text(hjust = 0.5)

)

retail_plot_log <- retail_ts |>

autoplot(.vars = log(sales_millions)) +

labs(

x = "Month",

y = "log(sales_millions)",

title = "Log of Sales (in millions)",

subtitle = "General Merchandise Stores"

) +

theme_minimal() +

theme(

plot.title = element_text(hjust = 0.5),

plot.subtitle = element_text(hjust = 0.5)

)

retail_plot_raw | retail_plot_log

Here are a few models we could fit to this time series.

Show the code

retail_ts |>

model(

ar_model = ARIMA(sales_millions ~ 1 +

pdq(1, 1, 0) +

PDQ(1, 0, 0), approximation = TRUE),

ma_model = ARIMA(sales_millions ~ 1 +

pdq(0, 1, 1) +

PDQ(0, 0, 1), approximation = TRUE),

arima_102012 = ARIMA(sales_millions ~ 1 +

pdq(1, 0, 2) +

PDQ(0, 1, 2), approximation = TRUE),

arima_102102 = ARIMA(sales_millions ~ 1 +

pdq(1, 0, 2) +

PDQ(1, 0, 2), approximation = TRUE),

arima_112112 = ARIMA(sales_millions ~ 1 +

pdq(1, 1, 2) +

PDQ(1, 1, 2), approximation = TRUE),

arima_012012 = ARIMA(sales_millions ~ 1 +

pdq(0, 1, 2) +

PDQ(0, 1, 2), approximation = TRUE),

arima_111111 = ARIMA(sales_millions ~ 1 +

pdq(1, 1, 1) +

PDQ(1, 1, 1), approximation = TRUE),

) |>

glance()| .model | sigma2 | log_lik | AIC | AICc | BIC |

|---|---|---|---|---|---|

| ar_model | 1887684 | -3227.047 | 6462.094 | 6462.204 | 6477.759 |

| ma_model | 15542235 | -3605.992 | 7219.985 | 7220.094 | 7235.650 |

| arima_102012 | 1264061 | -3038.772 | 6091.544 | 6091.862 | 6118.747 |

| arima_112112 | 1272651 | -3030.991 | 6077.982 | 6078.393 | 6109.048 |

| arima_012012 | 1266582 | -3031.167 | 6074.333 | 6074.572 | 6097.633 |

| arima_111111 | 1270495 | -3031.753 | 6075.506 | 6075.745 | 6098.806 |

Here is the model automatically selected by R.

Show the code

best_fit_retail <- retail_ts |>

model(

ar_model = ARIMA(sales_millions ~ 1 +

pdq(0:2, 0:2, 0:2) +

PDQ(0:2, 0:2, 0:2), approximation = TRUE))

best_fit_retail# A mable: 1 x 1

ar_model

<model>

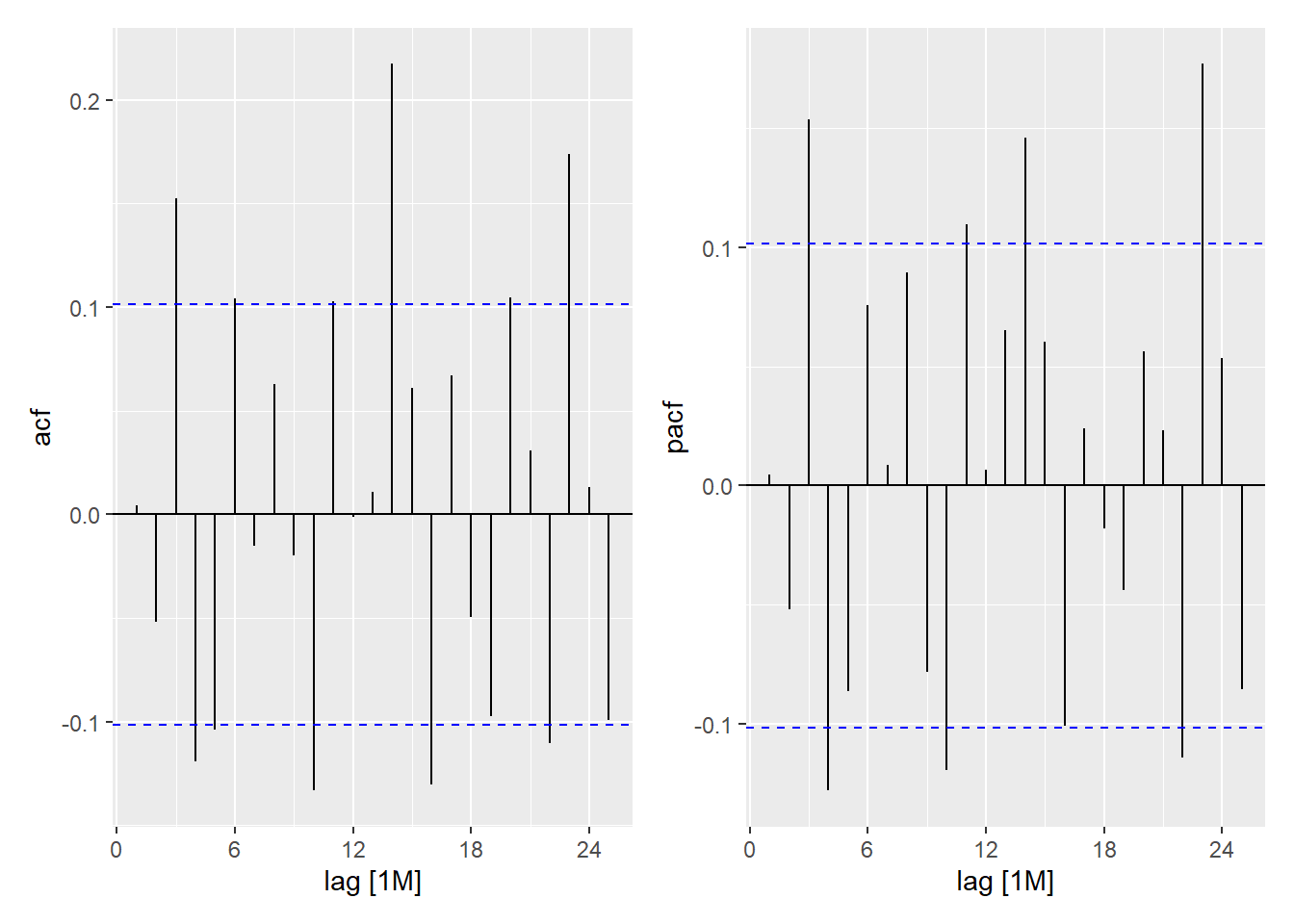

1 <ARIMA(1,0,2)(0,1,2)[12] w/ drift>This is the acf and pacf of the residuals from the automatically selected model.

Show the code

acf_plot <- best_fit_retail |>

residuals() |>

feasts::ACF() |>

autoplot()

pacf_plot <- best_fit_retail |>

residuals() |>

feasts::PACF() |>

autoplot()

acf_plot | pacf_plot

Here are the coefficients from the automatically-selected model.

Show the code

coefficients(best_fit_retail)| .model | term | estimate | std.error | statistic | p.value |

|---|---|---|---|---|---|

| ar_model | ar1 | 0.9783222 | 0.0159630 | 61.286943 | 0.0000000 |

| ar_model | ma1 | -0.8326530 | 0.0542793 | -15.340162 | 0.0000000 |

| ar_model | ma2 | 0.1720797 | 0.0561780 | 3.063114 | 0.0023554 |

| ar_model | sma1 | -0.4200558 | 0.0535544 | -7.843535 | 0.0000000 |

| ar_model | sma2 | -0.0980853 | 0.0515993 | -1.900905 | 0.0581128 |

| ar_model | constant | 39.3324830 | 9.4754966 | 4.150968 | 0.0000414 |

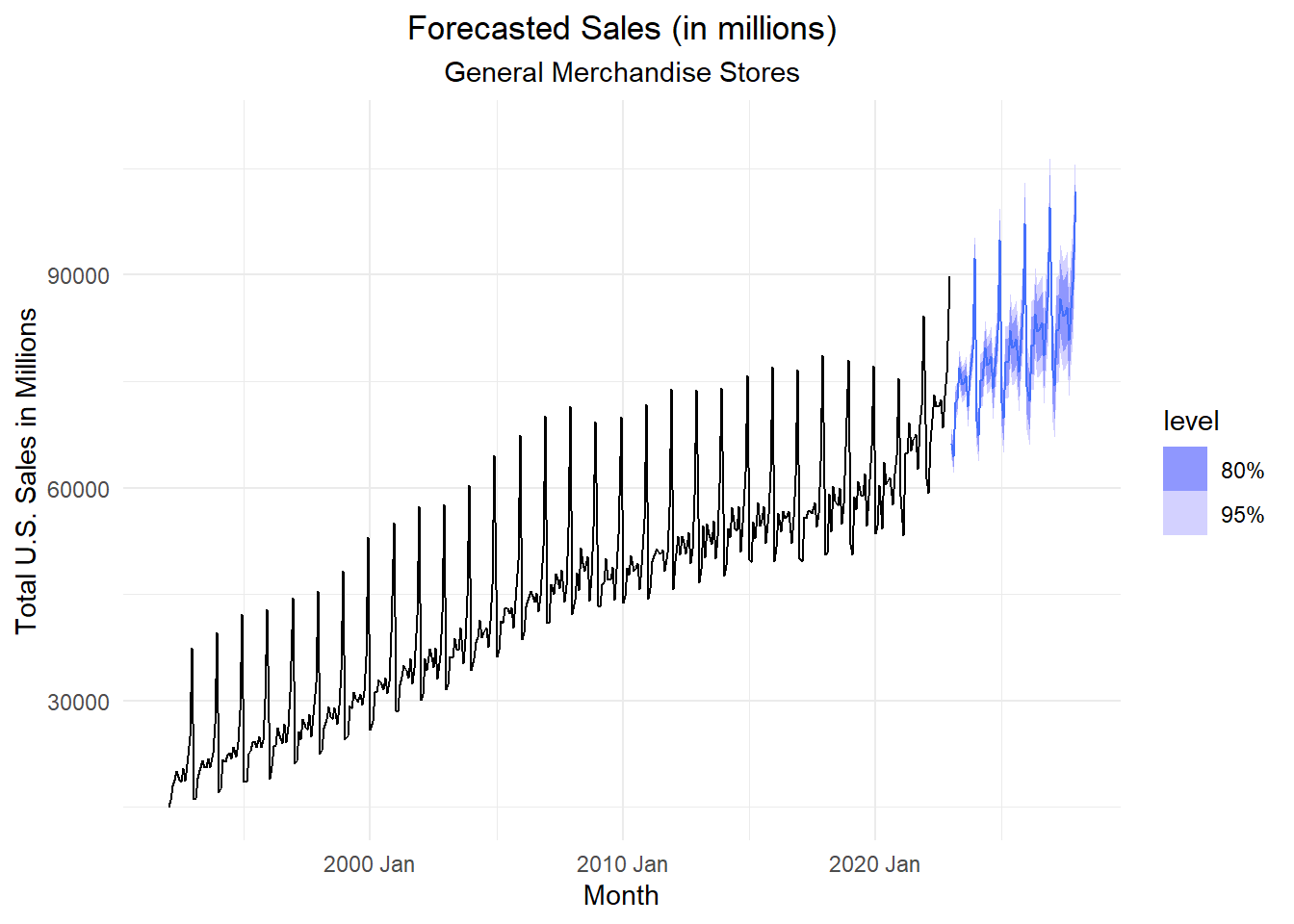

We can forecast future values of this time series using our model.

Show the code

best_fit_retail |>

forecast(h = "60 months") |>

autoplot(retail_ts) +

labs(

x = "Month",

y = "Total U.S. Sales in Millions",

title = "Forecasted Sales (in millions)",

subtitle = "General Merchandise Stores"

) +

theme_minimal() +

theme(

plot.title = element_text(hjust = 0.5),

plot.subtitle = element_text(hjust = 0.5)

)

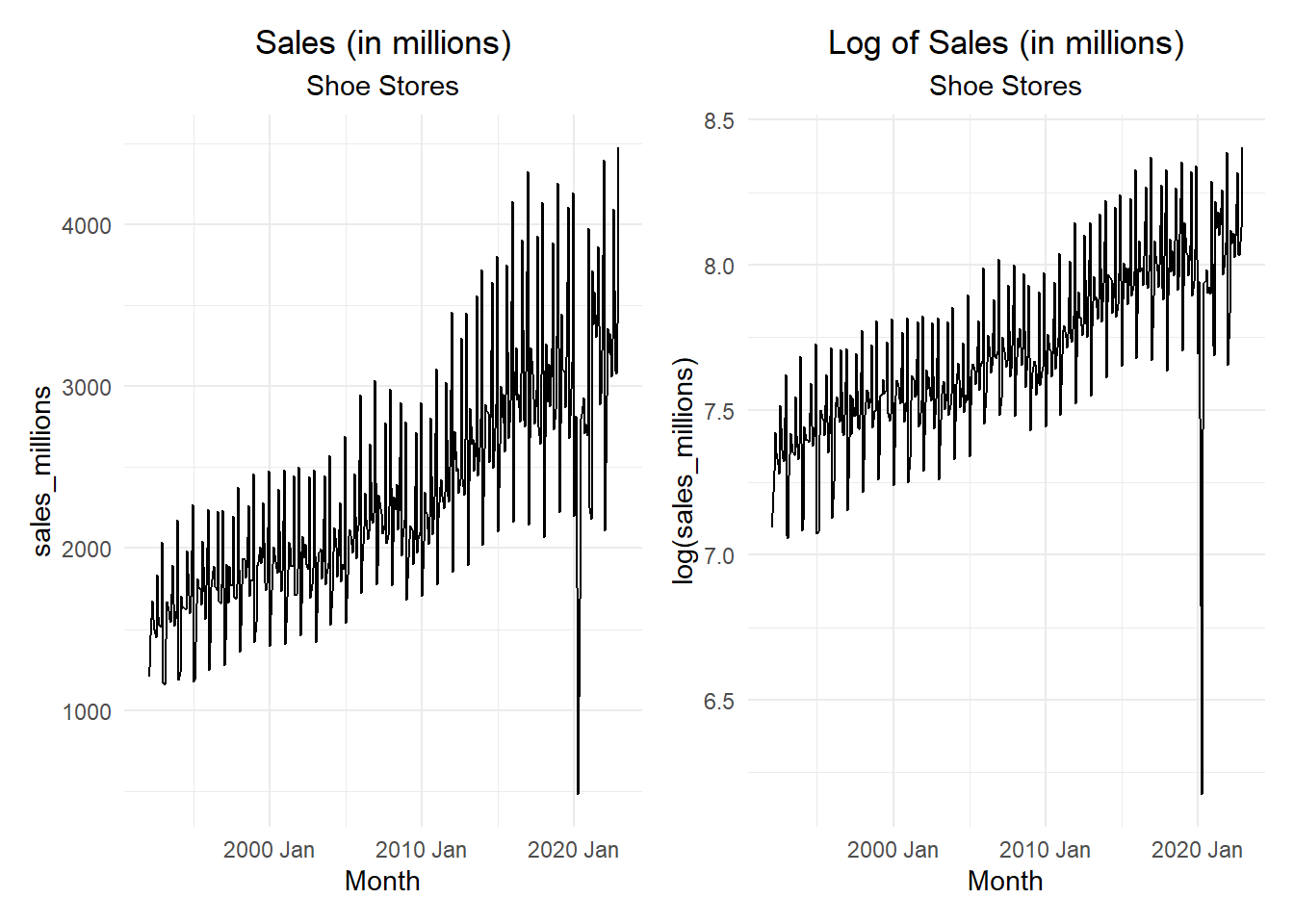

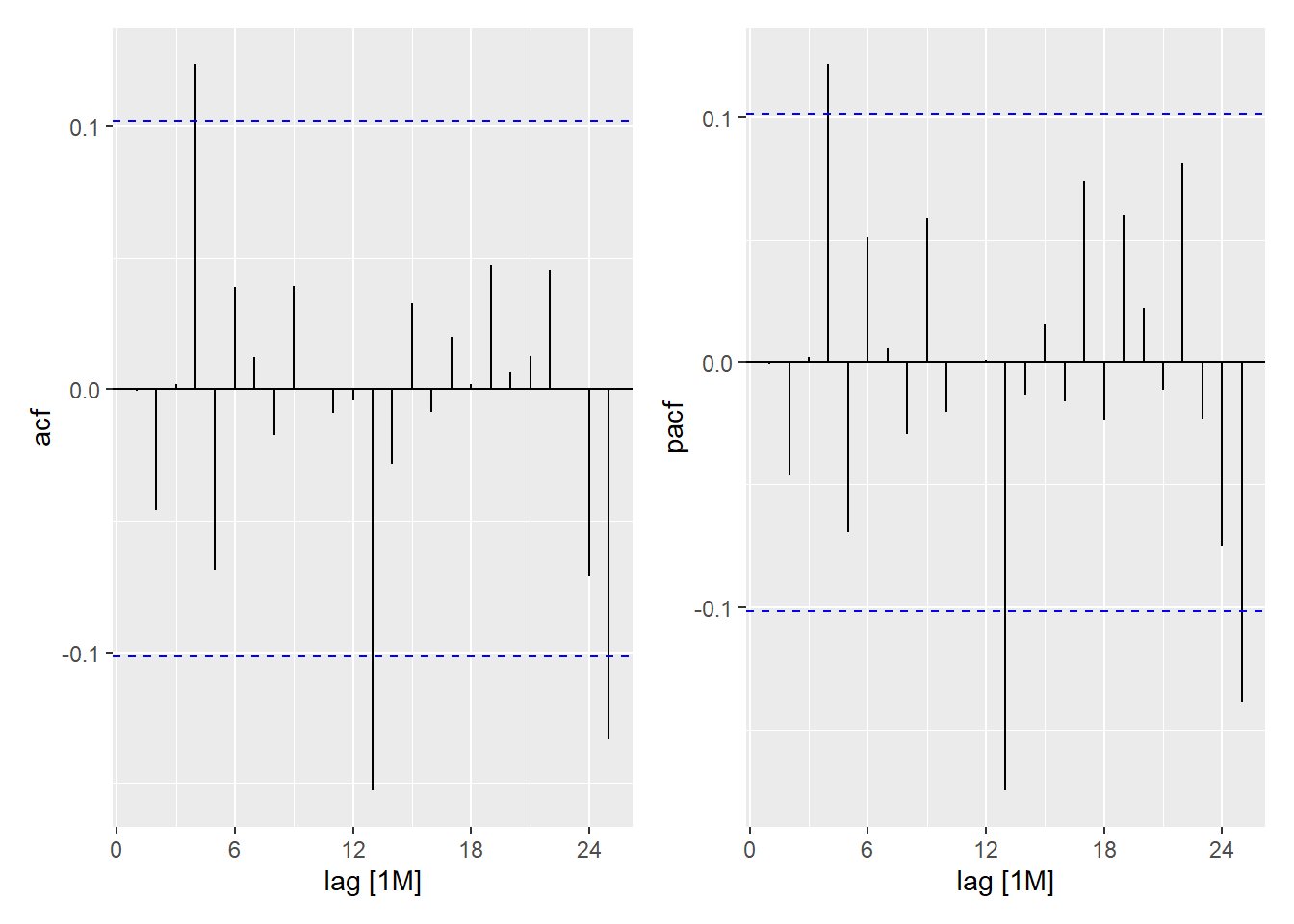

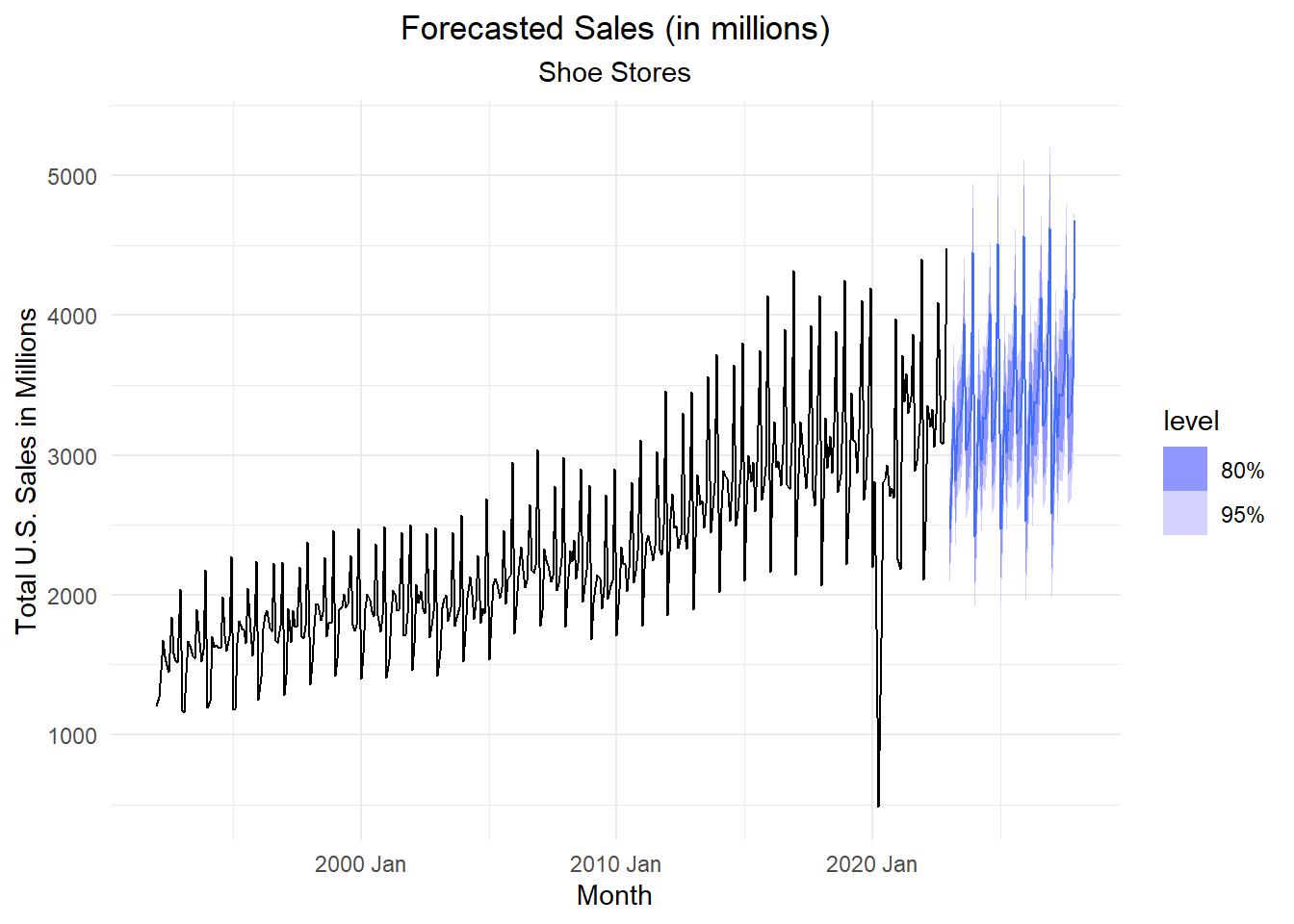

Small-Group Activity: Seasonal ARIMA Models - Retail: Shoe Stores (20 min)

Homework Preview (5 min)

- Review upcoming homework assignment

- Clarify questions

Small-Group Activity: Seasonal ARIMA Models - Retail: Shoe Stores