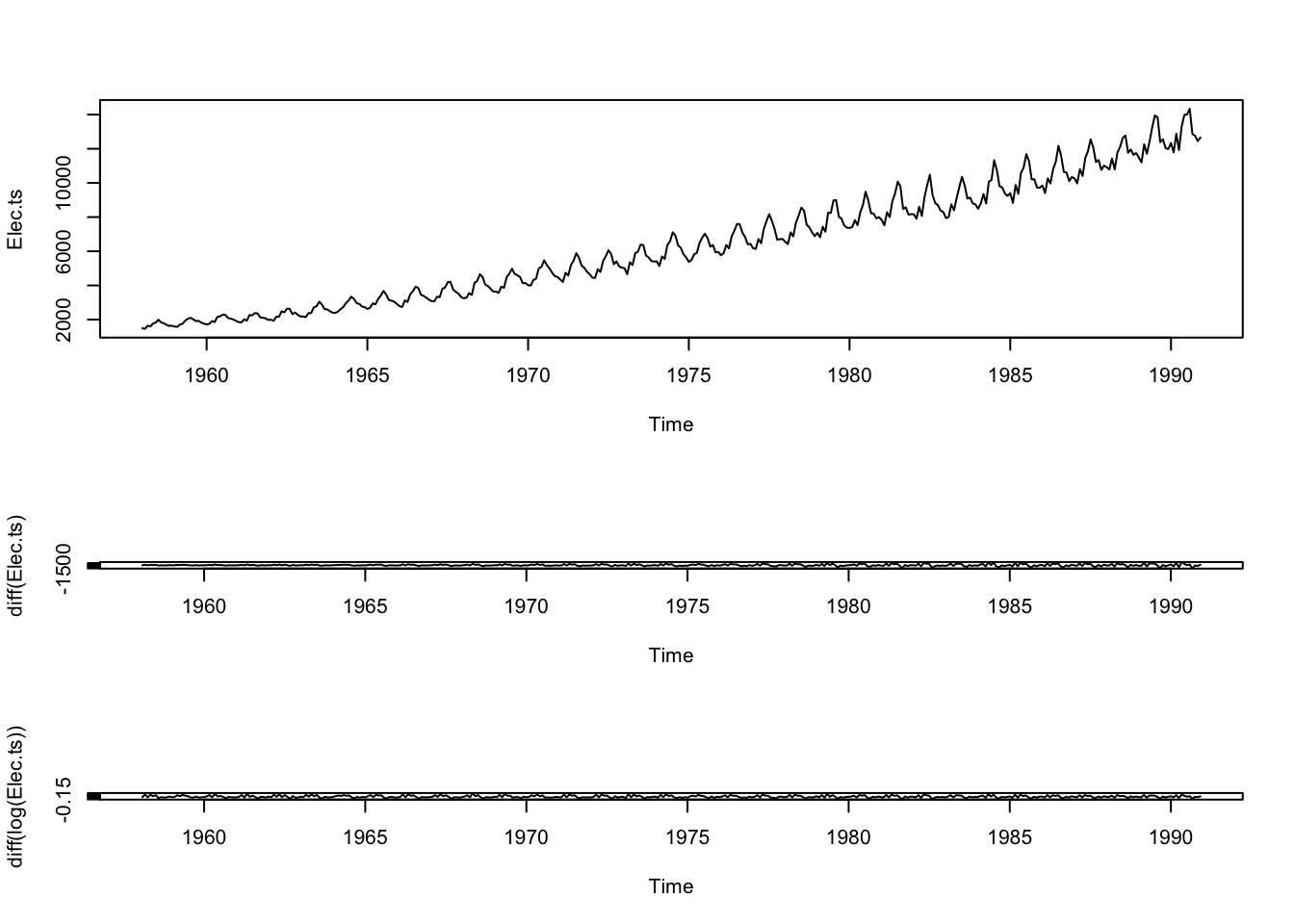

CBE <- read.table("data/cbe.dat", header = T)

Elec.ts <- ts(CBE[, 3], start = 1958, freq = 12)

layout(c(1, 1, 2, 3))

plot(Elec.ts)

plot(diff(Elec.ts))

plot(diff(log(Elec.ts)))

In this chapter, we extend the random walk model to include autoregressive and moving average terms. As the differenced series needs to be ‘integrated’ to recover the original series, the underlying stochastic process is called autoregressive integrated moving average, abbreviated to ARIMA.

We would like to note that the use of the R package tseries for GARCH models appears to be inferior with the addition of the rugarch package (see paper). Currently, no tidyverse developed package supports GARCH.

A short introduction to the rugarch package is helpful to discover more uses of the package.

Book code

CBE <- read.table("data/cbe.dat", header = T)

Elec.ts <- ts(CBE[, 3], start = 1958, freq = 12)

layout(c(1, 1, 2, 3))

plot(Elec.ts)

plot(diff(Elec.ts))

plot(diff(log(Elec.ts)))

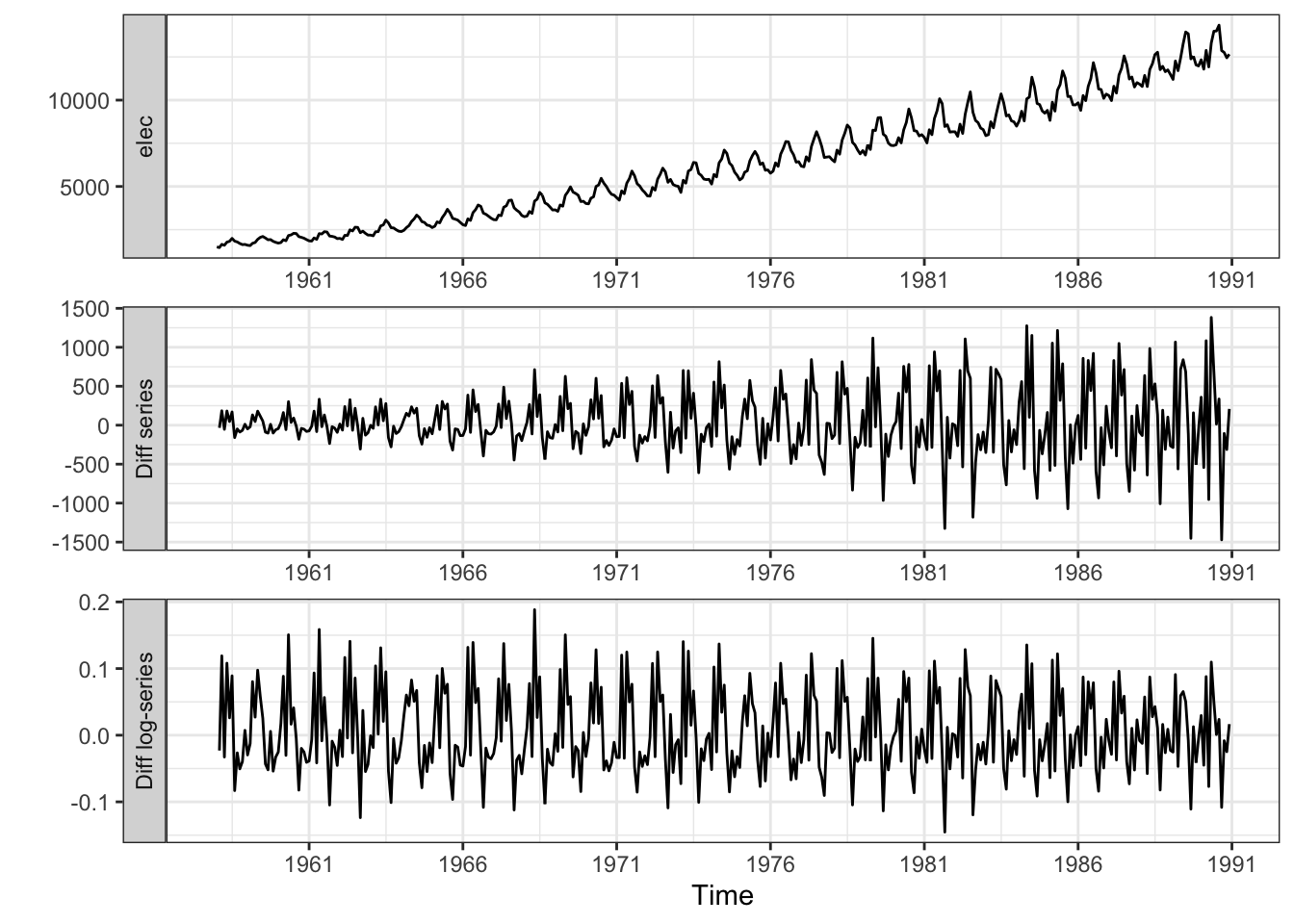

Tidyverts code

pacman::p_load("tsibble", "fable", "feasts",

"tsibbledata", "fable.prophet",

"tidyverse", "patchwork")

cbe <- read_table("data/cbe.dat")

elec_ts <- cbe |>

select(elec) |>

mutate(

date = seq(

ymd("1958-01-01"),

by = "1 months",

length.out = n()),

year_month = tsibble::yearmonth(date)) |>

as_tsibble(index = year_month)

elec_ts |>

mutate(

`Diff series` = elec - lag(elec),

`Diff log-series` = log(elec) - lag(log(elec))) |>

pivot_longer(

cols = all_of(c("elec", "Diff series", "Diff log-series"))) |>

mutate(name = factor(name, levels =c("elec","Diff series", "Diff log-series"))) |>

ggplot(aes(x = date, y = value)) +

geom_line() +

facet_wrap(~name, ncol = 1, scales = "free", strip.position = "left") +

labs(x = "Time", y = "") +

scale_x_date(breaks = "5 years", date_labels = "%Y") +

theme_bw()

pacman::p_load("tsibble", "fable", "feasts",

"tsibbledata", "fable.prophet",

"tidyverse", "patchwork")

cbe <- read_table("data/cbe.dat")

elec_ts <- cbe |>

select(elec) |>

mutate(

date = seq(

ymd("1958-01-01"),

by = "1 months",

length.out = n()),

year_month = tsibble::yearmonth(date)) |>

as_tsibble(index = year_month)

elec_ts |>

mutate(

`Diff series` = elec - lag(elec),

`Diff log-series` = log(elec) - lag(log(elec))) |>

pivot_longer(

cols = all_of(c("elec", "Diff series", "Diff log-series"))) |>

mutate(name = factor(name, levels =c("elec","Diff series", "Diff log-series"))) |>

ggplot(aes(x = date, y = value)) +

geom_line() +

facet_wrap(~name, ncol = 1, scales = "free", strip.position = "left") +

labs(x = "Time", y = "") +

scale_x_date(breaks = "5 years", date_labels = "%Y") +

theme_bw()Book code

set.seed(1)

x <- w <- rnorm(1000)

for (i in 3:1000) x[i] <- 0.5 * x[i - 1] + x[i - 1] -

0.5 * x[i - 2] + w[i] + 0.3 * w[i - 1]

arima(x, order = c(1, 1, 1))

Call:

arima(x = x, order = c(1, 1, 1))

Coefficients:

ar1 ma1

0.4235 0.3308

s.e. 0.0433 0.0450

sigma^2 estimated as 1.067: log likelihood = -1450.13, aic = 2906.26Tidyverts code

set.seed(1)

x <- w <- rnorm(1000)

for (i in 3:1000) x[i] <- 0.5 * x[i - 1] + x[i - 1] -

0.5 * x[i - 2] + w[i] + 0.3 * w[i - 1]

tibble(x = x) |>

mutate(time = 1:n()) |>

as_tsibble(index = time) |>

model(arima = ARIMA(x ~ pdq(1, 1, 1) + PDQ(0, 0, 0))) |>

tidy()# A tibble: 2 × 6

.model term estimate std.error statistic p.value

<chr> <chr> <dbl> <dbl> <dbl> <dbl>

1 arima ar1 0.423 0.0433 9.79 1.11e-21

2 arima ma1 0.331 0.0450 7.35 4.02e-13x <- arima.sim(model = list(

order = c(1, 1, 1),

ar = 0.5,

ma = 0.3),

n = 1000)

arima(x, order = c(1, 1, 1))

Call:

arima(x = x, order = c(1, 1, 1))

Coefficients:

ar1 ma1

0.5567 0.2502

s.e. 0.0372 0.0437

sigma^2 estimated as 1.079: log likelihood = -1457.45, aic = 2920.91tibble(x = arima.sim(model = list(

order = c(1, 1, 1),

ar = 0.5,

ma = 0.3),

n = 1000)) |>

mutate(time = 1:n()) |>

as_tsibble(index = time) |>

model(arima = ARIMA(x ~ pdq(1, 1, 1) + PDQ(0, 0, 0))) |>

tidy()# A tibble: 2 × 6

.model term estimate std.error statistic p.value

<chr> <chr> <dbl> <dbl> <dbl> <dbl>

1 arima ar1 0.475 0.0380 12.5 2.42e-33

2 arima ma1 0.376 0.0395 9.53 1.19e-20set.seed(1)

x <- w <- rnorm(1000)

for (i in 3:1000) x[i] <- 0.5 * x[i - 1] + x[i - 1] -

0.5 * x[i - 2] + w[i] + 0.3 * w[i - 1]

tibble(x = x) |>

mutate(time = 1:n()) |>

as_tsibble(index = time) |>

model(arima = ARIMA(x ~ pdq(1, 1, 1) + PDQ(0, 0, 0))) |>

tidy()

tibble(x = arima.sim(model = list(

order = c(1, 1, 1),

ar = 0.5,

ma = 0.3),

n = 1000)) |>

mutate(time = 1:n()) |>

as_tsibble(index = time) |>

model(arima = ARIMA(x ~ pdq(1, 1, 1) + PDQ(0, 0, 0))) |>

tidy()Book code

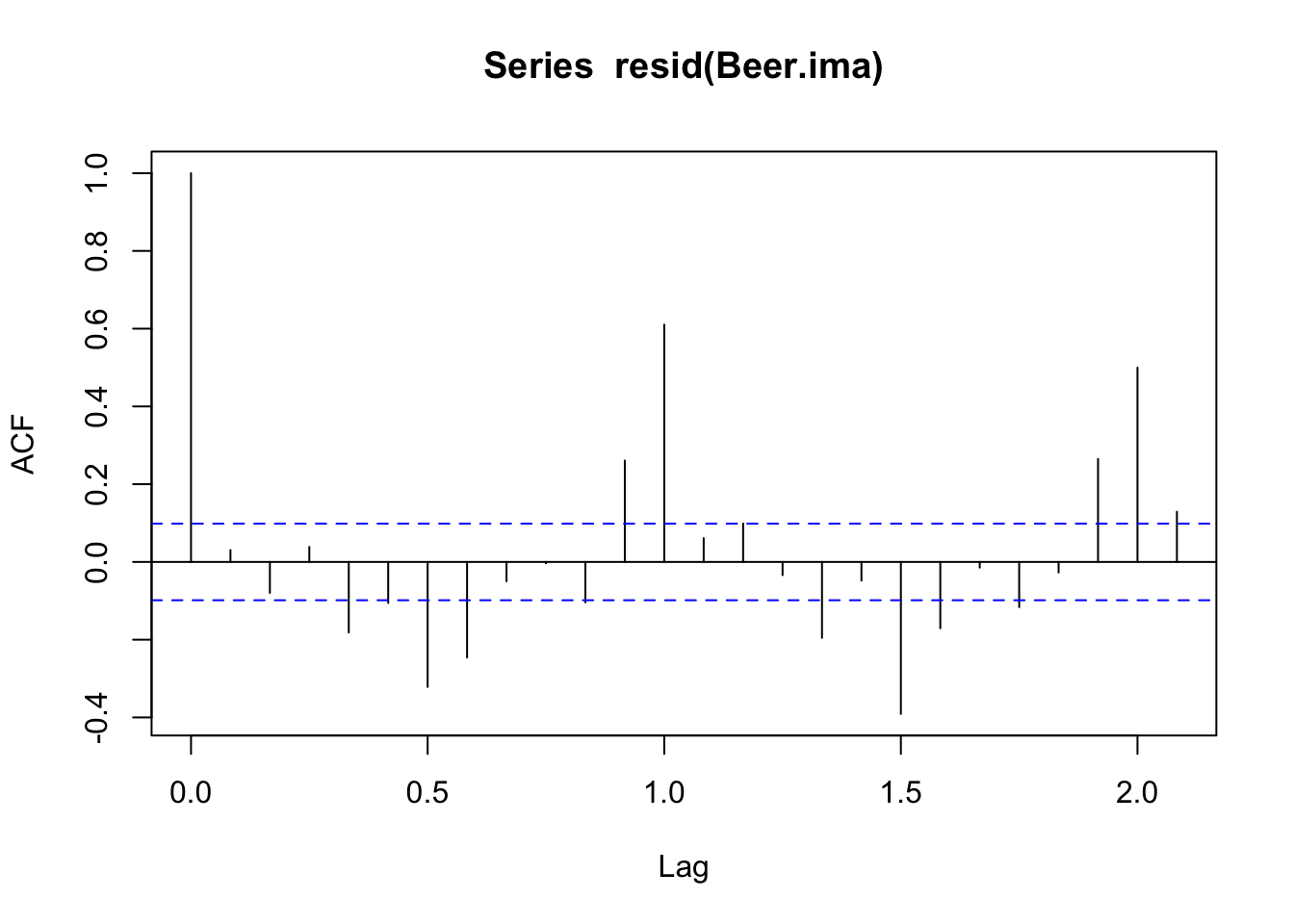

Beer.ts <- ts(CBE[, 2], start = 1958, freq = 12)

Beer.ima <- arima(Beer.ts, order = c(0, 1, 1))

Beer.ima

Call:

arima(x = Beer.ts, order = c(0, 1, 1))

Coefficients:

ma1

-0.3334

s.e. 0.0558

sigma^2 estimated as 360.4: log likelihood = -1723.27, aic = 3450.53Tidyverts code

cbe <- read_table("data/cbe.dat")

beer_ts <- cbe |>

select(beer) |>

mutate(

date = seq(

ymd("1958-01-01"),

by = "1 months",

length.out = n()),

year_month = tsibble::yearmonth(date)) |>

as_tsibble(index = year_month)

beer_arima <- beer_ts |>

model(arima = ARIMA(beer ~ pdq(0, 1, 1) + PDQ(0, 0, 0)))

tidy(beer_arima)# A tibble: 1 × 6

.model term estimate std.error statistic p.value

<chr> <chr> <dbl> <dbl> <dbl> <dbl>

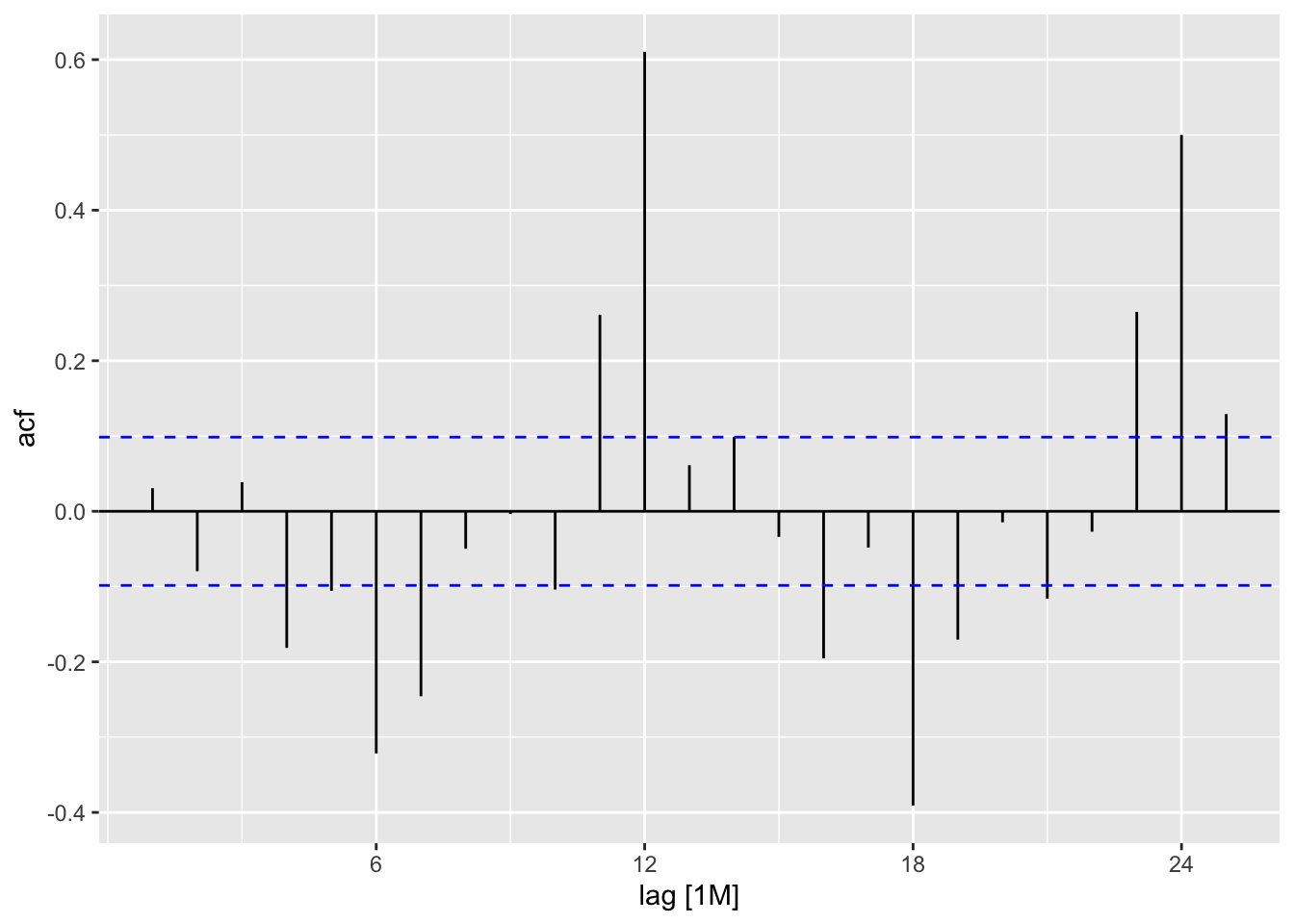

1 arima ma1 -0.333 0.0558 -5.97 0.00000000515acf(resid(Beer.ima))

beer_arima |>

residuals() |>

ACF() |>

autoplot()

Beer.1991 <- predict(Beer.ima, n.ahead = 12)

sum(Beer.1991$pred)[1] 2365.412beer_1991 <- beer_arima |>

forecast(h = "12 months")

pull(beer_1991, .mean) |> sum()[1] 2365.412cbe <- read_table("data/cbe.dat")

beer_ts <- cbe |>

select(beer) |>

mutate(

date = seq(

ymd("1958-01-01"),

by = "1 months",

length.out = n()),

year_month = tsibble::yearmonth(date)) |>

as_tsibble(index = year_month)

beer_arima <- beer_ts |>

model(arima = ARIMA(beer ~ pdq(0, 1, 1) + PDQ(0, 0, 0)))

tidy(beer_arima)

beer_arima |>

residuals() |>

ACF() |>

autoplot()

beer_1991 <- beer_arima |>

forecast(h = "12 months")

pull(beer_1991, .mean) |> sum()Book code

aic1 <- AIC(arima(log(Elec.ts),

order = c(1,1,0),

seas = list(order = c(1,0,0), 12)))

aic2 <- AIC(arima(log(Elec.ts),

order = c(0,1,1),

seas = list(order = c(0,0,1), 12)))

c("aic1" = aic1, "aic2" = aic2) aic1 aic2

-1764.741 -1361.586 Tidyverts code

elec_ts |>

model(

ar_model = ARIMA(log(elec) ~ 1 +

pdq(1, 1, 0) +

PDQ(1, 0, 0)),

ma_model = ARIMA(log(elec) ~ 1 +

pdq(0, 1, 1) +

PDQ(0, 0, 1))) |>

glance() |>

pull(AIC)[1] -1763.076 -1362.217get.best.arima <- function(x.ts, maxord = c(1,1,1,1,1,1)) {

best.aic <- 1e8

n <- length(x.ts)

for (p in 0:maxord[1]) for(d in 0:maxord[2]) for(q in 0:maxord[3])

for (P in 0:maxord[4]) for(D in 0:maxord[5]) for(Q in 0:maxord[6])

{

fit <- arima(x.ts, order = c(p,d,q),

seas = list(order = c(P,D,Q),

frequency(x.ts)), method = "CSS")

fit.aic <- -2 * fit$loglik + (log(n) + 1) * length(fit$coef)

if (fit.aic < best.aic)

{

best.aic <- fit.aic

best.fit <- fit

best.model <- c(p,d,q,P,D,Q)

}

}

list(best.aic, best.fit, best.model)

}

best.arima.elec <- get.best.arima(

log(Elec.ts),

maxord = c(2,2,2,2,2,2))

best.fit.elec <- best.arima.elec[[2]]

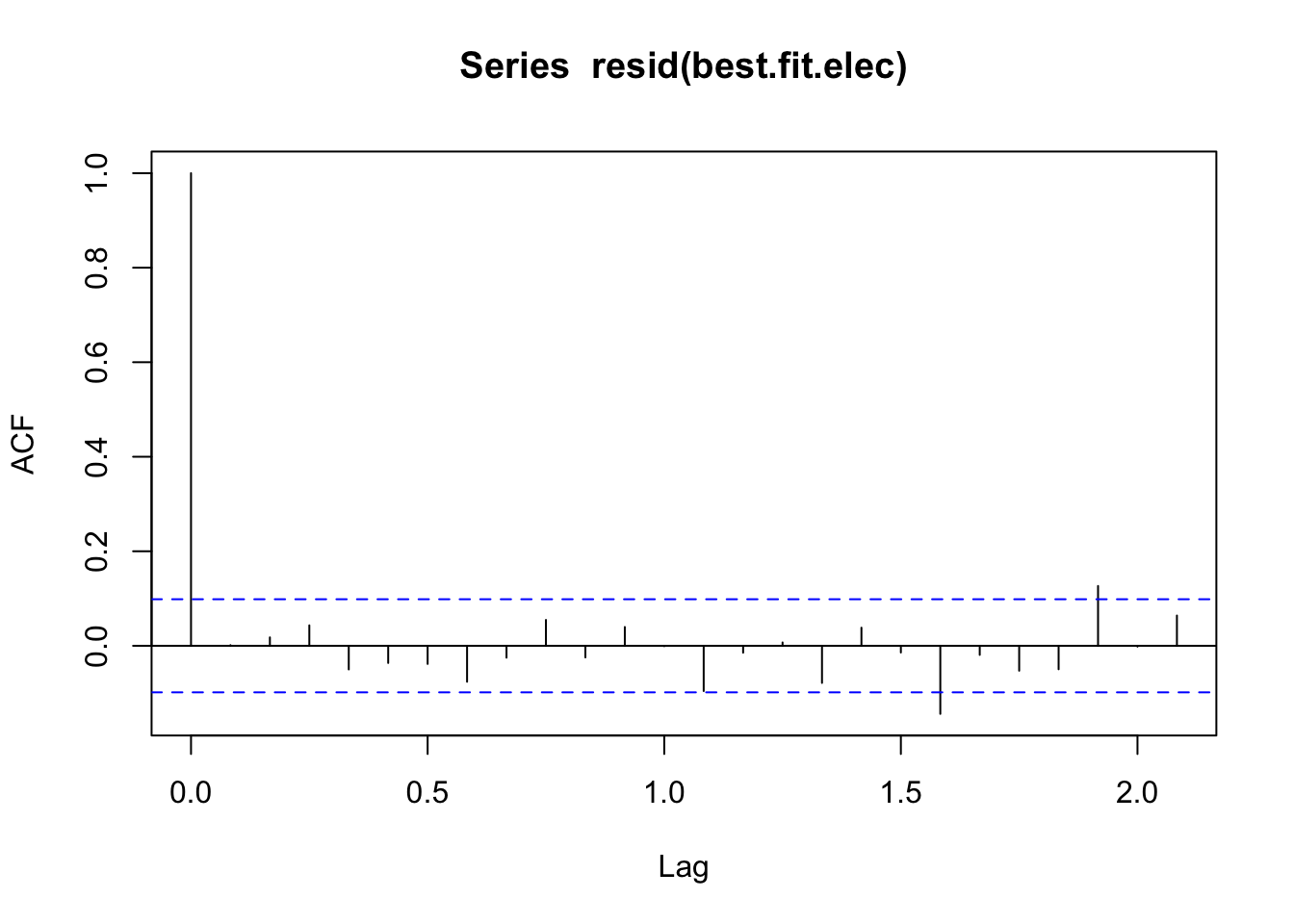

acf(resid(best.fit.elec))

best_fit_elec <- elec_ts |>

model(

ar_model = ARIMA(log(elec) ~ 1 +

pdq(0:2, 0:2, 0:2) +

PDQ(0:2, 0:2, 0:2), approximation = TRUE))

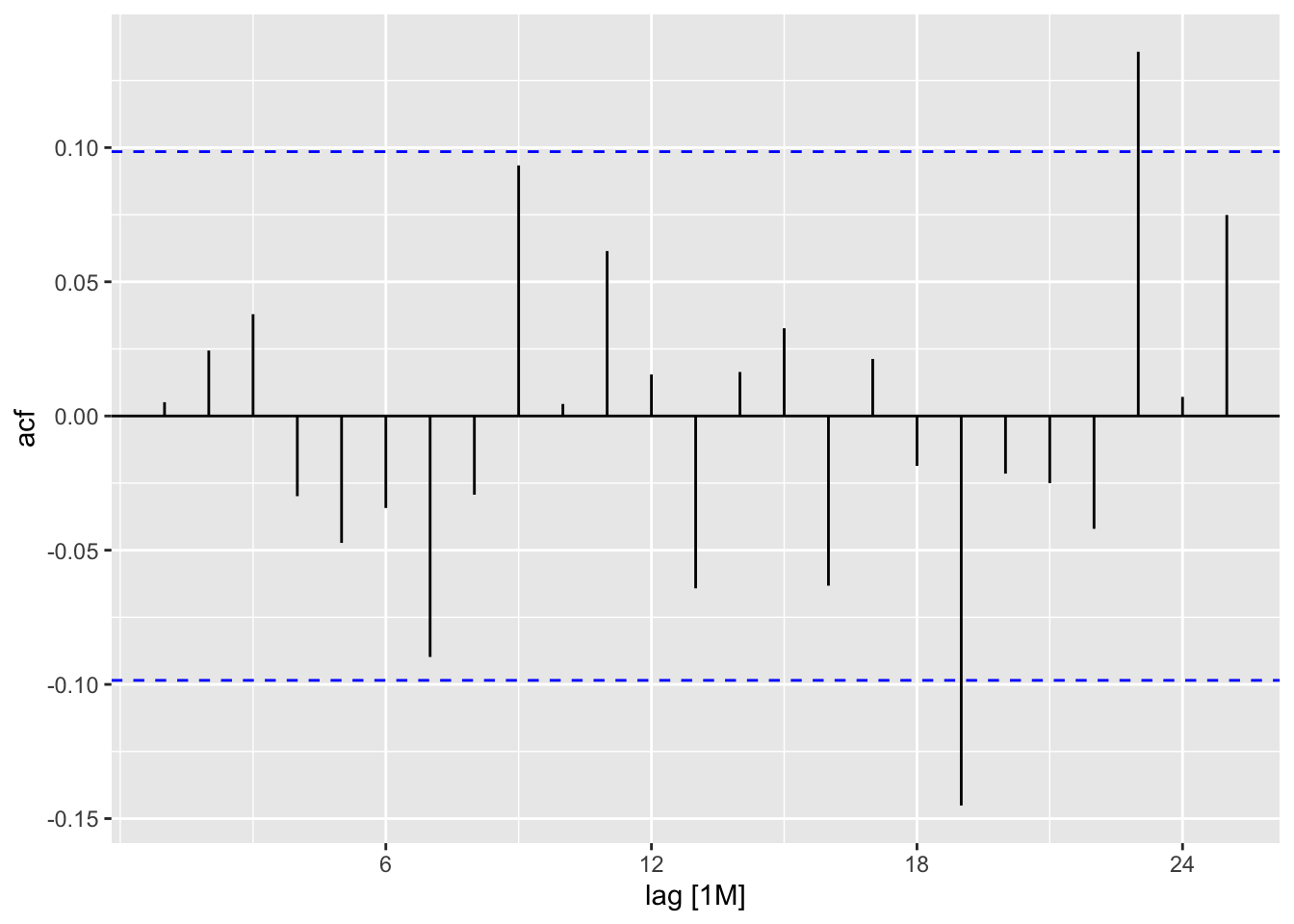

best_fit_elec |>

residuals() |>

ACF() |>

autoplot()

best.arima.elec[[3]][1] 0 1 1 2 0 2best_fit_elec# A mable: 1 x 1

ar_model

<model>

1 <ARIMA(2,0,1)(1,1,2)[12] w/ drift>ts.plot(cbind(window(Elec.ts,start = 1981),

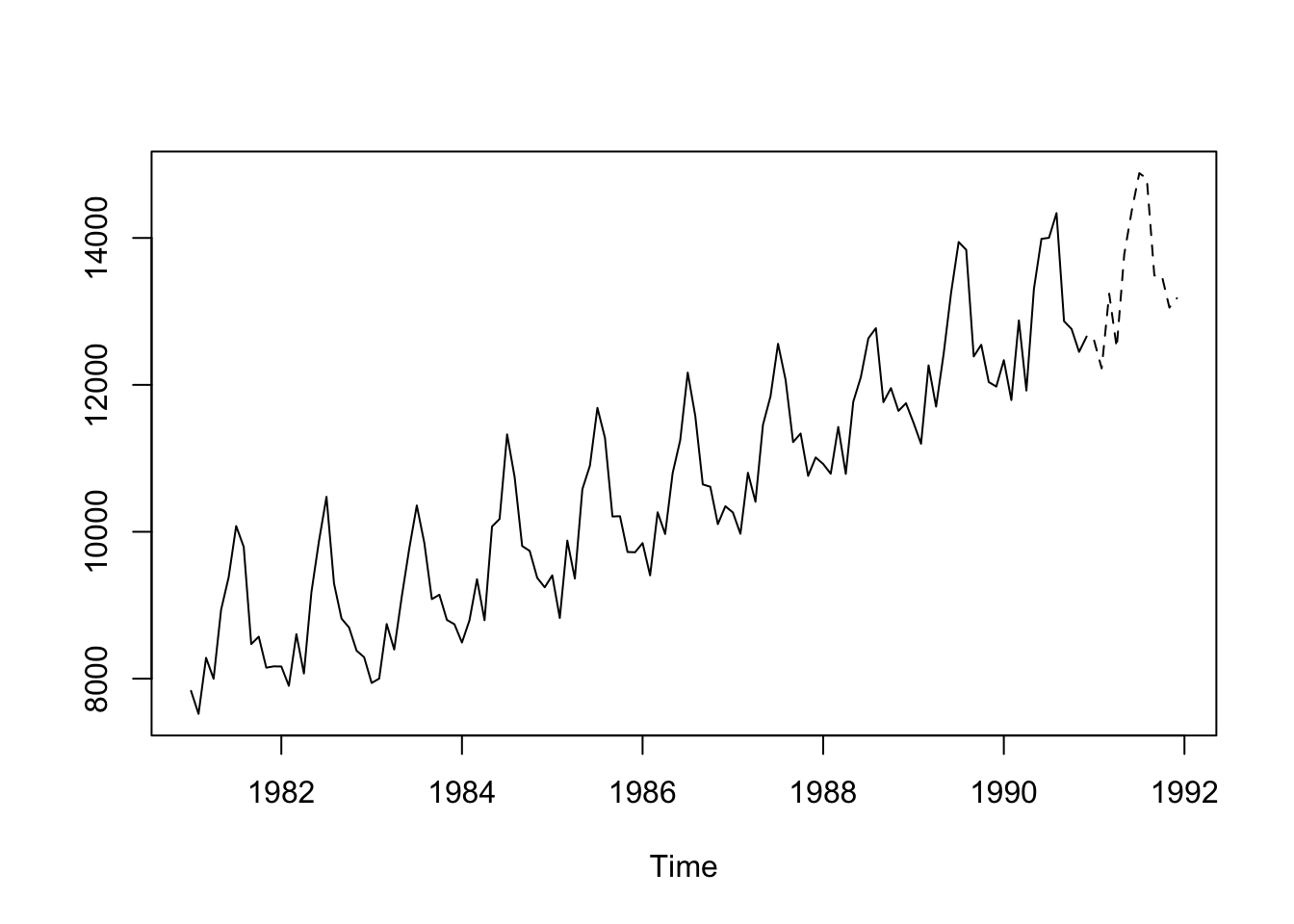

exp(predict(best.fit.elec,12)$pred) ), lty = 1:2)

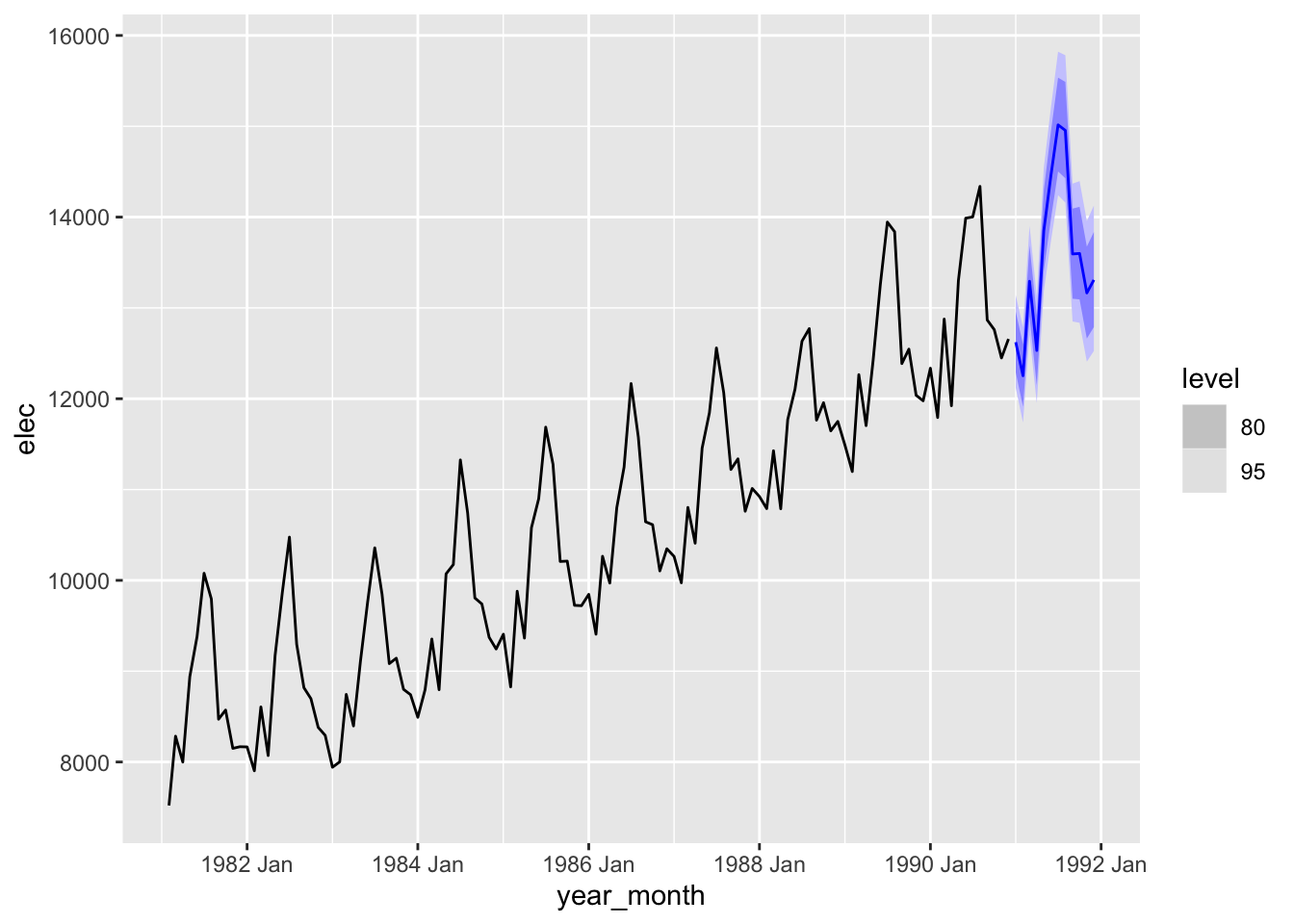

best_fit_elec |>

forecast(h = "12 months") |>

autoplot(filter(elec_ts, date > ymd("1981-01-01")))

aic1 <- AIC(arima(log(Elec.ts),

order = c(1,1,0),

seas = list(order = c(1,0,0), 12)))

aic2 <- AIC(arima(log(Elec.ts),

order = c(0,1,1),

seas = list(order = c(0,0,1), 12)))

c("aic1" = aic1, "aic2" = aic2)

get.best.arima <- function(x.ts, maxord = c(1,1,1,1,1,1)) {

best.aic <- 1e8

n <- length(x.ts)

for (p in 0:maxord[1]) for(d in 0:maxord[2]) for(q in 0:maxord[3])

for (P in 0:maxord[4]) for(D in 0:maxord[5]) for(Q in 0:maxord[6])

{

fit <- arima(x.ts, order = c(p,d,q),

seas = list(order = c(P,D,Q),

frequency(x.ts)), method = "CSS")

fit.aic <- -2 * fit$loglik + (log(n) + 1) * length(fit$coef)

print(paste(paste(c(p,d,q,P,D,Q), collapse = "-"), "AIC:", fit.aic))

if (fit.aic < best.aic)

{

best.aic <- fit.aic

best.fit <- fit

best.model <- c(p,d,q,P,D,Q)

}

}

list(best.aic, best.fit, best.model)

}

best.arima.elec <- get.best.arima(

log(Elec.ts),

maxord = c(2,2,2,2,2,2))

best.fit.elec <- best.arima.elec[[2]]

acf(resid(best.fit.elec))

best.arima.elec[[3]]

ts.plot(cbind(window(Elec.ts,start = 1981),

exp(predict(best.fit.elec,12)$pred) ), lty = 1:2)elec_ts |>

model(

ar_model = ARIMA(log(elec) ~ 1 +

pdq(1, 1, 0) +

PDQ(1, 0, 0)),

ma_model = ARIMA(log(elec) ~ 1 +

pdq(0, 1, 1) +

PDQ(0, 0, 1))) |>

glance() |>

pull(AIC)

best_fit_elec <- elec_ts |>

model(

ar_model = ARIMA(log(elec) ~ 1 +

pdq(0:2, 0:2, 0:2) +

PDQ(0:2, 0:2, 0:2), approximation = TRUE))

best_fit_elec |>

residuals() |>

ACF() |>

autoplot()

glance(best_fit_elec) |> pull(AIC)

best_fit_elec |>

forecast(h = "12 months") |>

autoplot(filter(elec_ts, date > ymd("1981-01-01")))

# Very Slow, but you can see all fits.

# get_arima <- function(p, d, q, P, D, Q, data = elec_ts) {

# model(data, arima = ARIMA(log(elec) ~ 1 +

# pdq(p, d, q) + PDQ(P, D, Q), approximation = TRUE))

# }

# get_aic <- function(fit) {

# gfit <- glance(fit)

# if (nrow(gfit) != 0) {

# pull(gfit, AIC)

# } else {

# NA

# }

# }

# all_possible <- expand_grid(

# p = 0:2, d = 0:2, q = 0:2,

# P = 0:2, D = 0:2, Q = 0:2)

# all_possible <- all_possible |>

# mutate(

# fit = purrr::pmap(all_possible, get_arima),

# aic = purrr::map_dbl(fit, ~get_aic(.x))

# )

# filter(all_possible, aic == min(aic, na.rm = TRUE))Book code

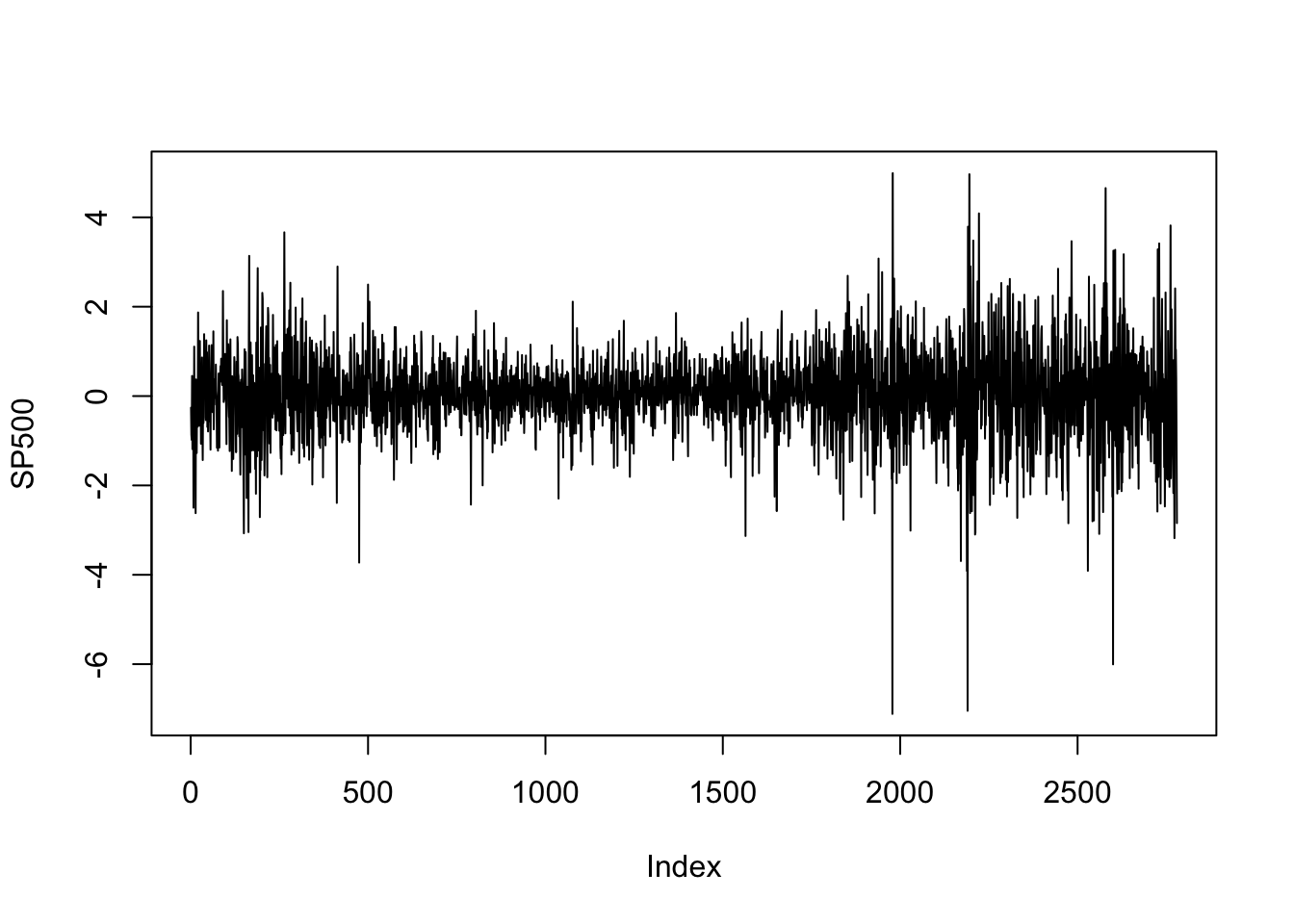

library(MASS)

data(SP500)

plot(SP500, type = 'l')

Tidyverts code

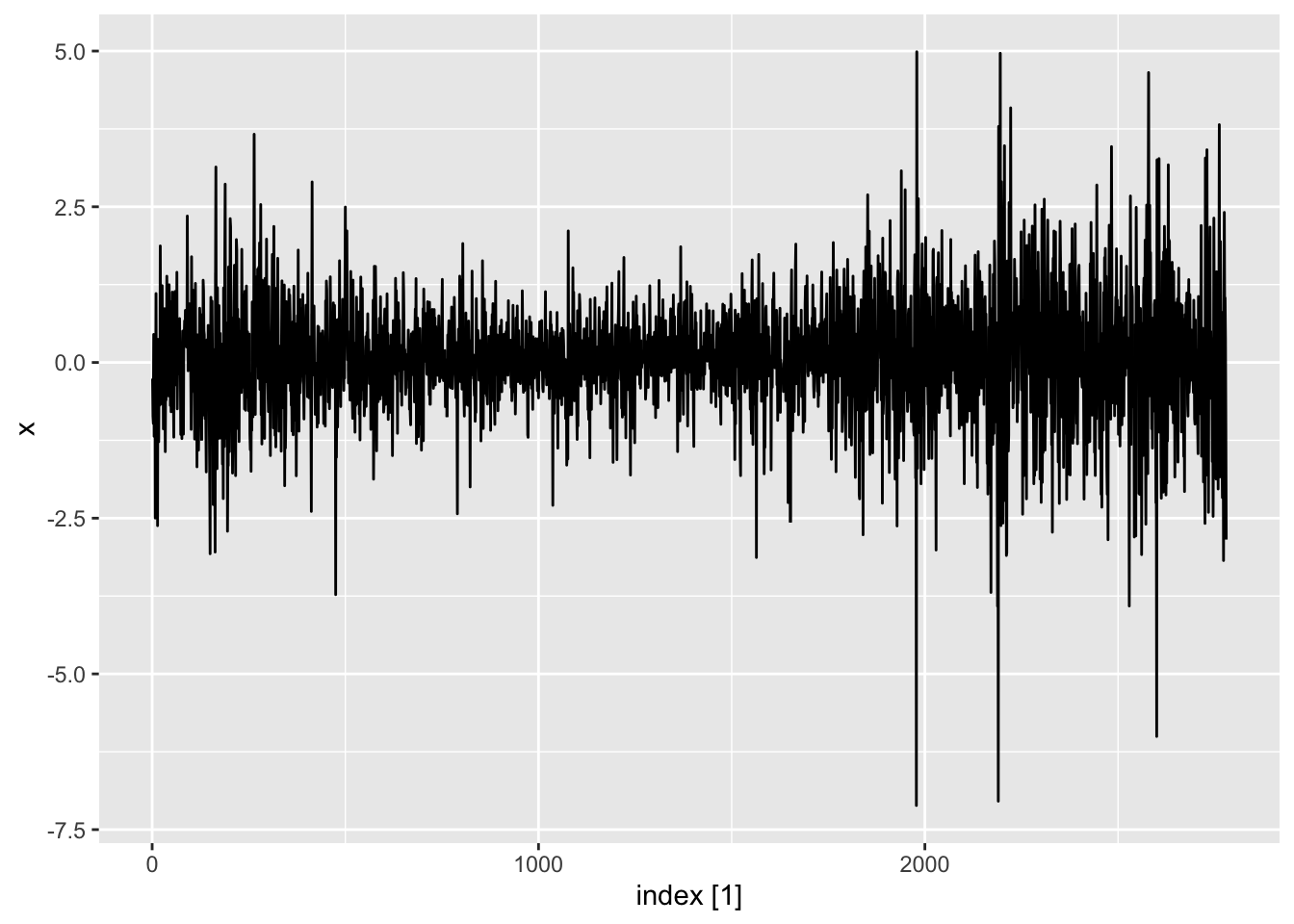

library(MASS)

data(SP500)

dat <- tibble(x = SP500) |>

mutate(

sq_mean_diff = (x - mean(x))^2,

index = 1:n()) |>

as_tsibble(index = index)

autoplot(dat)

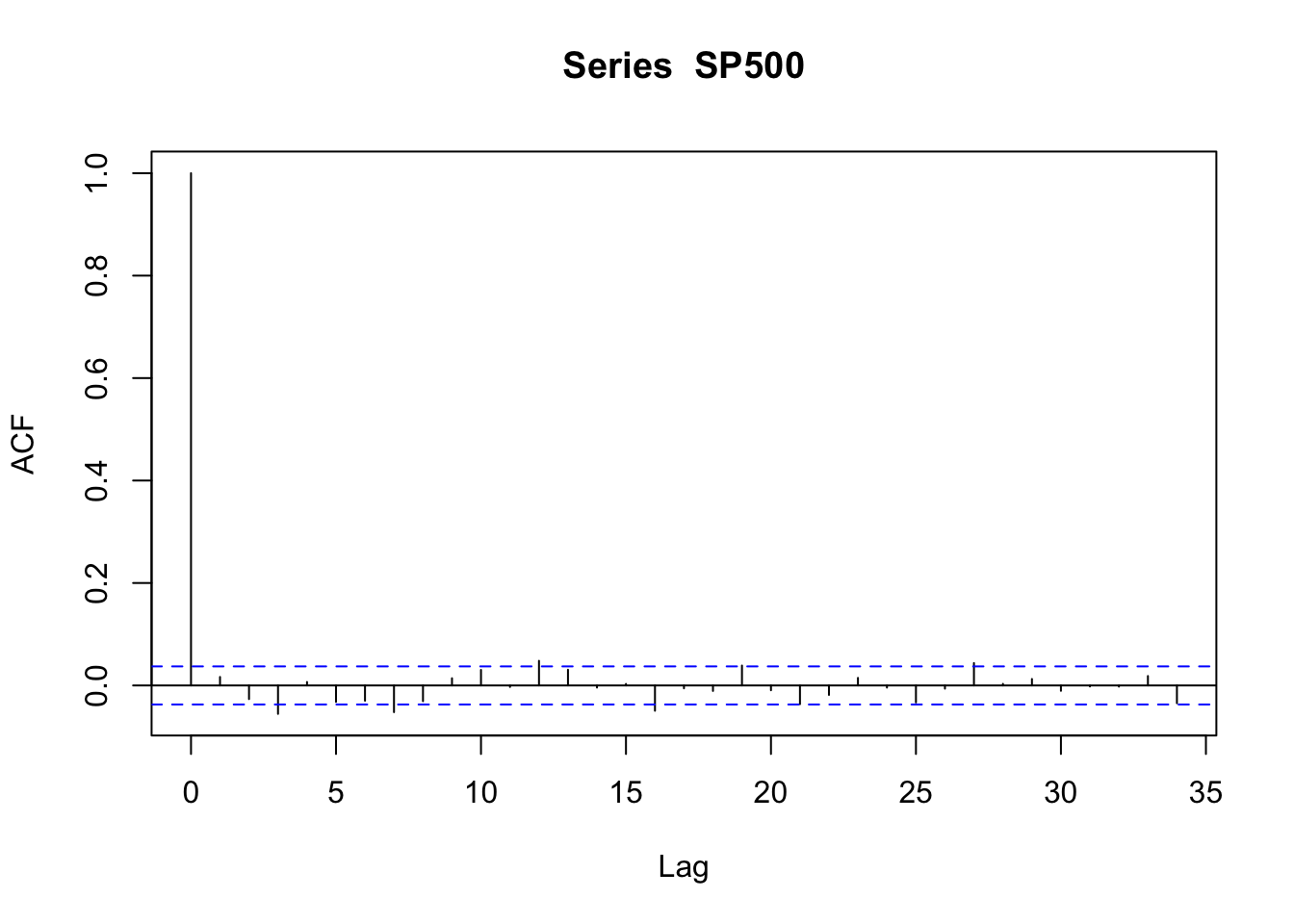

acf(SP500)

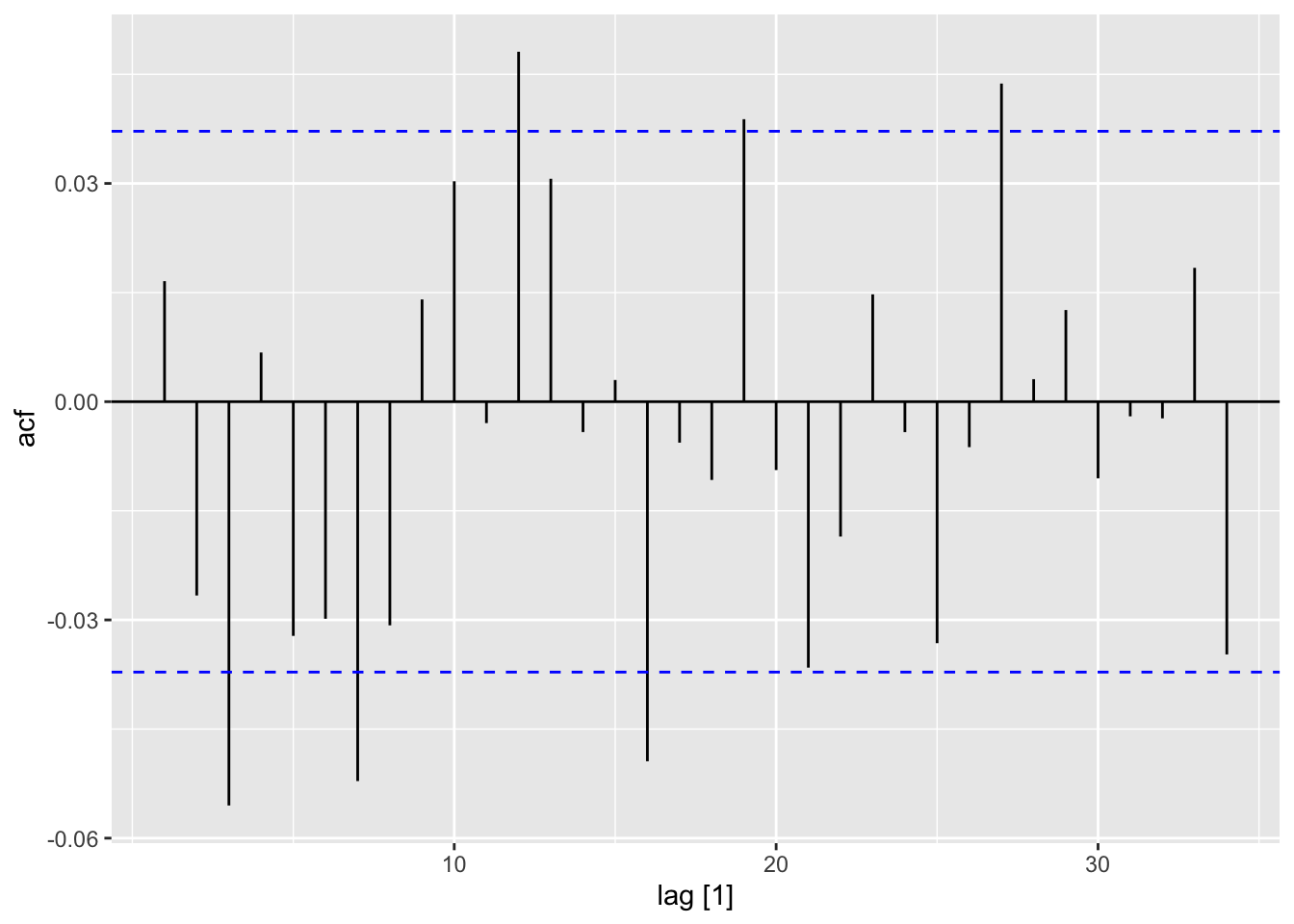

ACF(dat) |> autoplot()

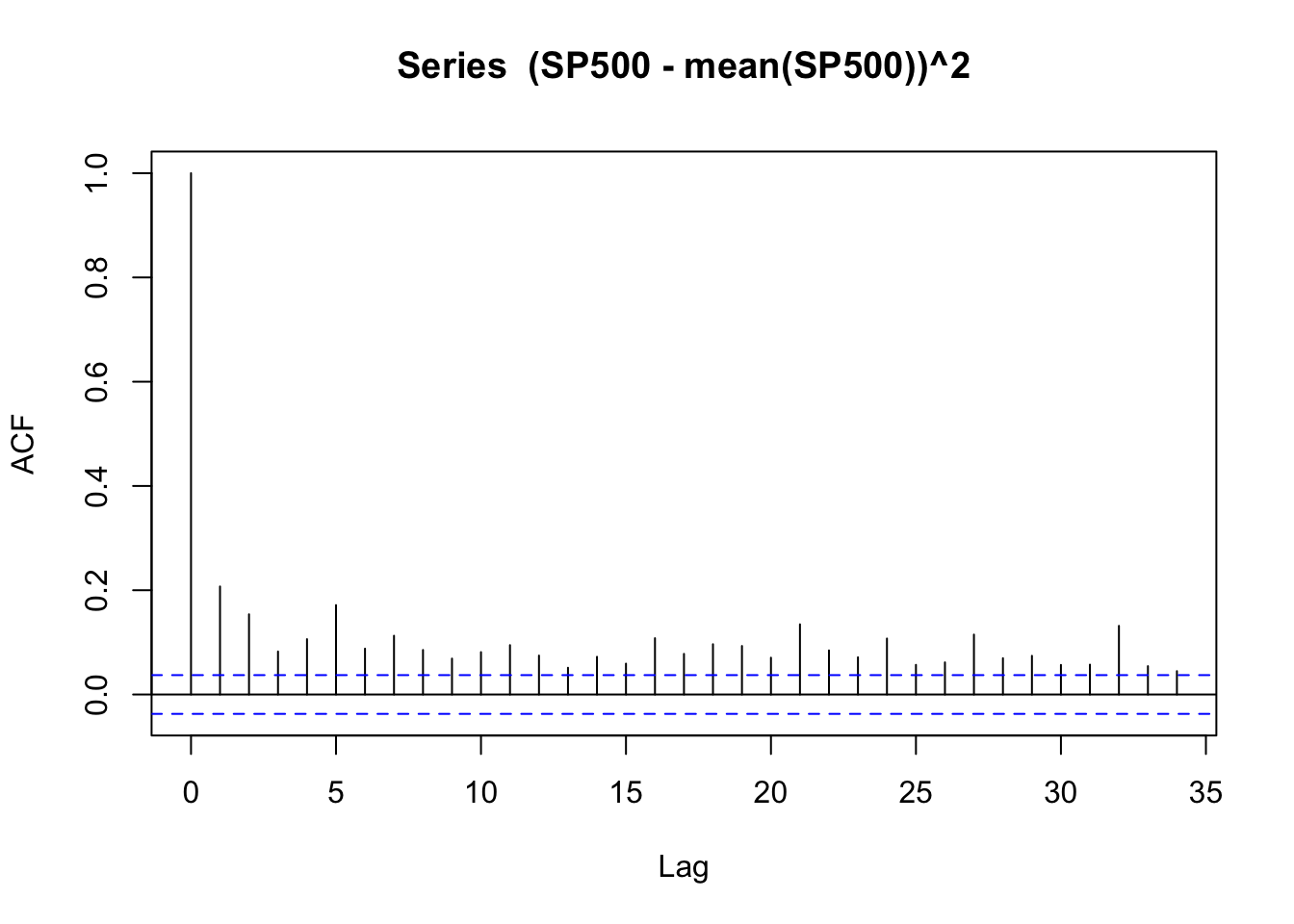

acf((SP500 - mean(SP500))^2)

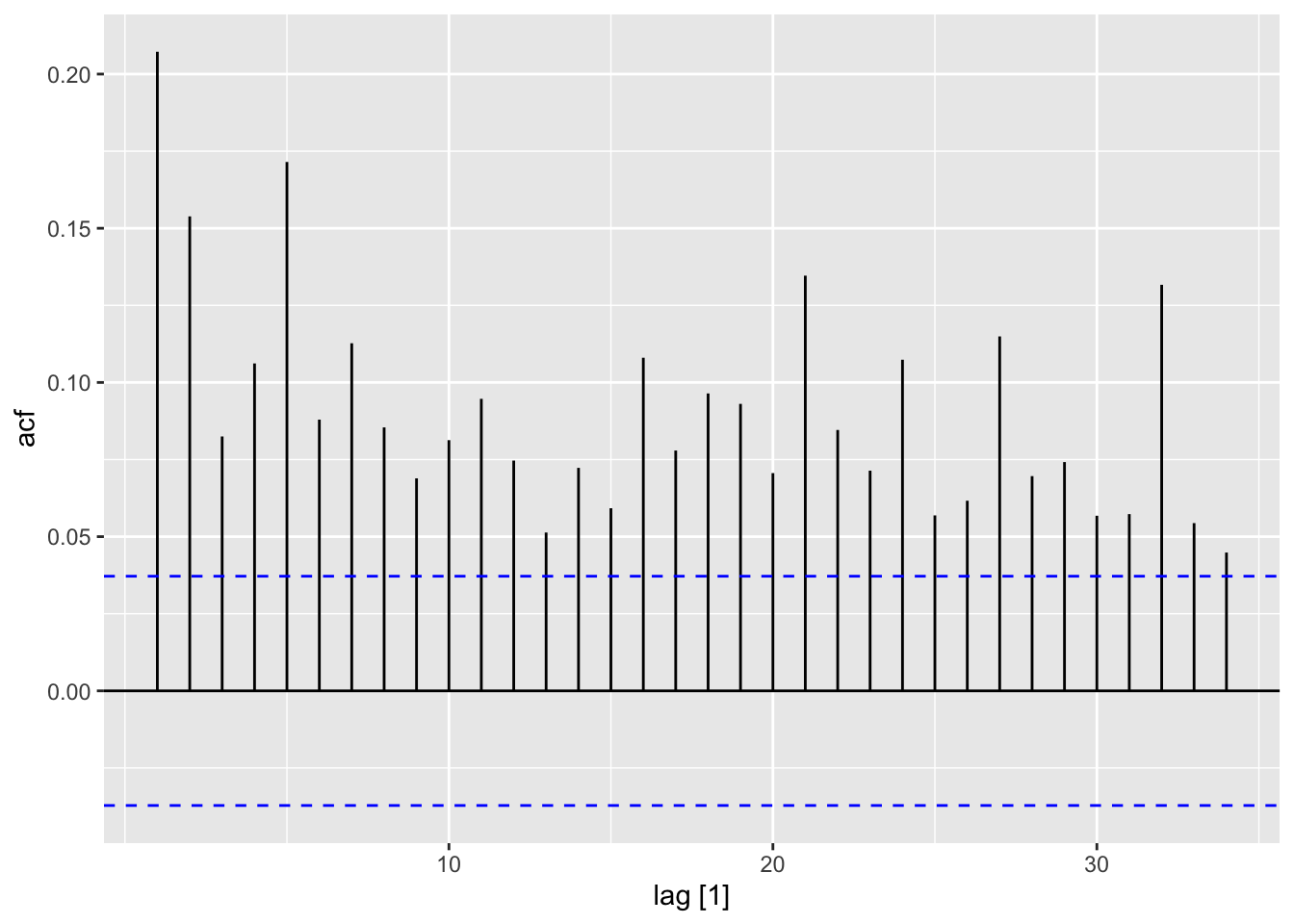

ACF(dat, y = sq_mean_diff) |> autoplot()

Book code

library(tseries)

set.seed(1)

alpha0 <- 0.1

alpha1 <- 0.4

beta1 <- 0.2

w <- rnorm(10000)

a <- rep(0, 10000)

h <- rep(0, 10000)

for (i in 2:10000) {

h[i] <- alpha0 + alpha1 * (a[i - 1]^2) + beta1 * h[i - 1]

a[i] <- w[i] * sqrt(h[i])

}

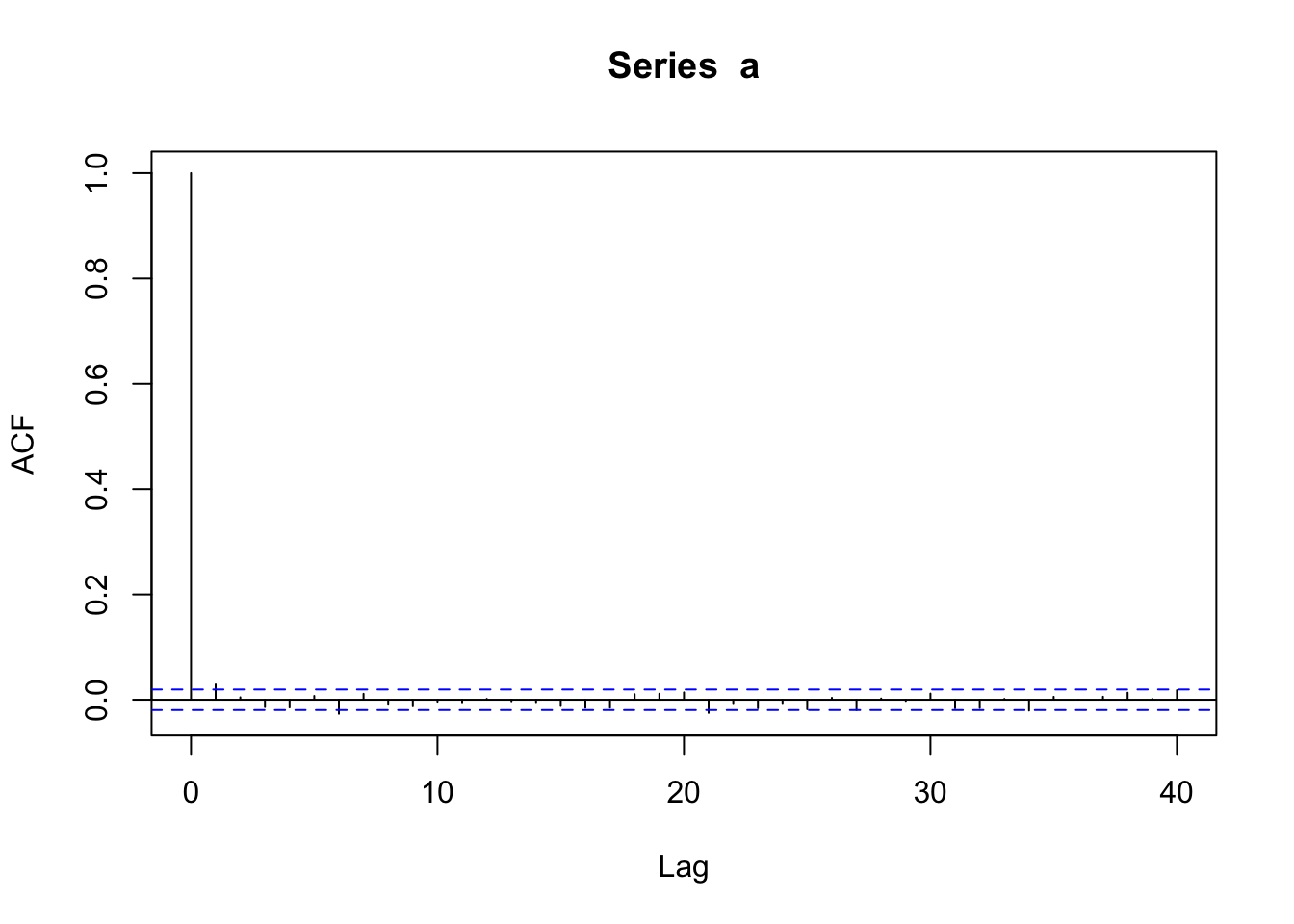

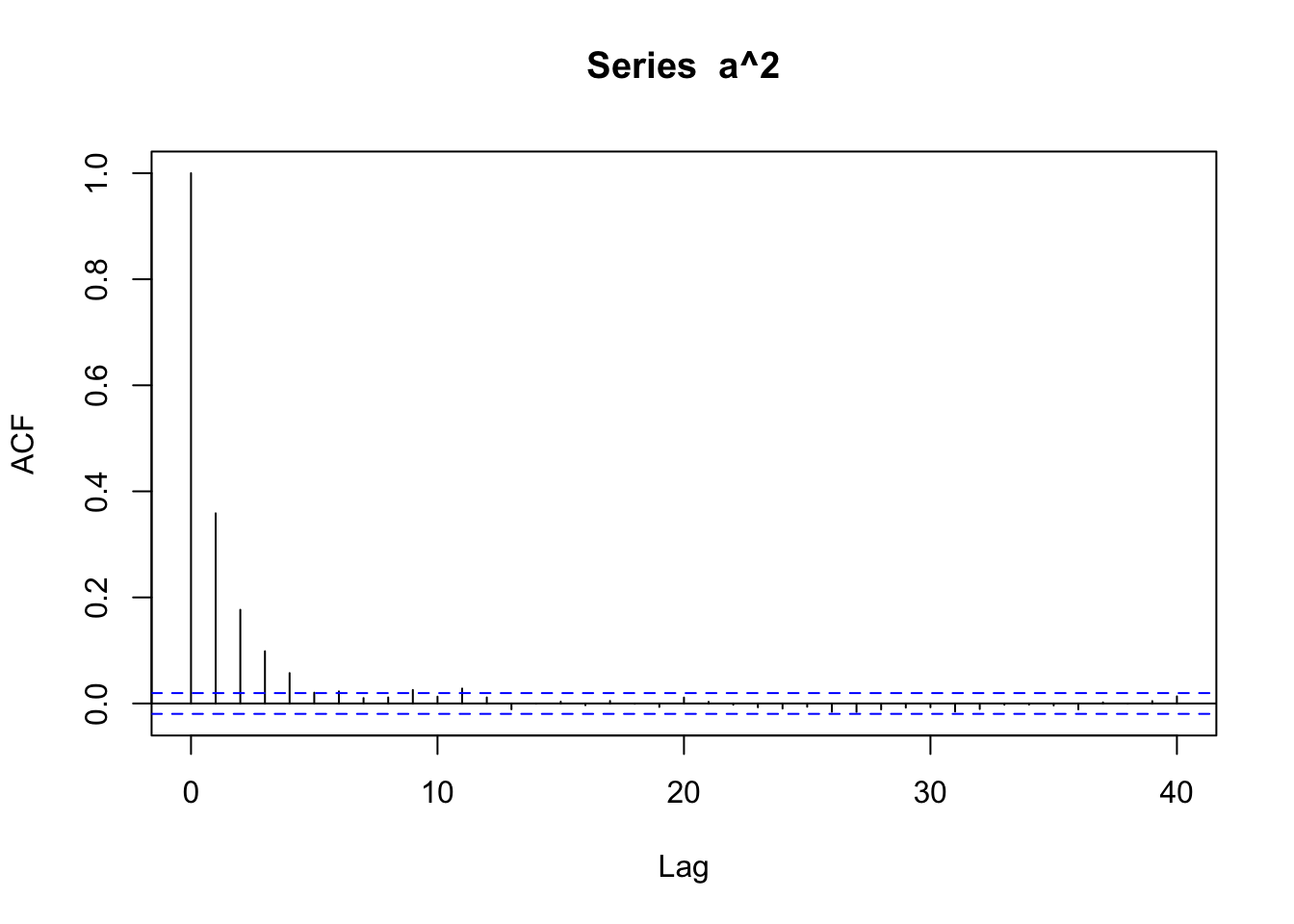

acf(a)

Tidyverts code

pacman::p_load("rugarch")

set.seed(1)

sim <- tibble(

alpha0 = 0.1,

alpha1 = 0.4,

beta1 = 0.2,

w = rnorm(10000),

a = rep(0, 10000),

h = rep(0, 10000)) |>

mutate(index = 1:n()) |>

as_tsibble(index = index)

for (i in 2:10000) {

sim$h[i] <- sim$alpha0[1] + sim$alpha1[1] * (sim$a[i - 1]^2) + sim$beta1[1] * sim$h[i - 1]

sim$a[i] <- sim$w[i] * sqrt(sim$h[i])

}

sim <- mutate(sim, a2 = a^2)

ACF(sim, y = a) |>

autoplot()

acf(a^2)

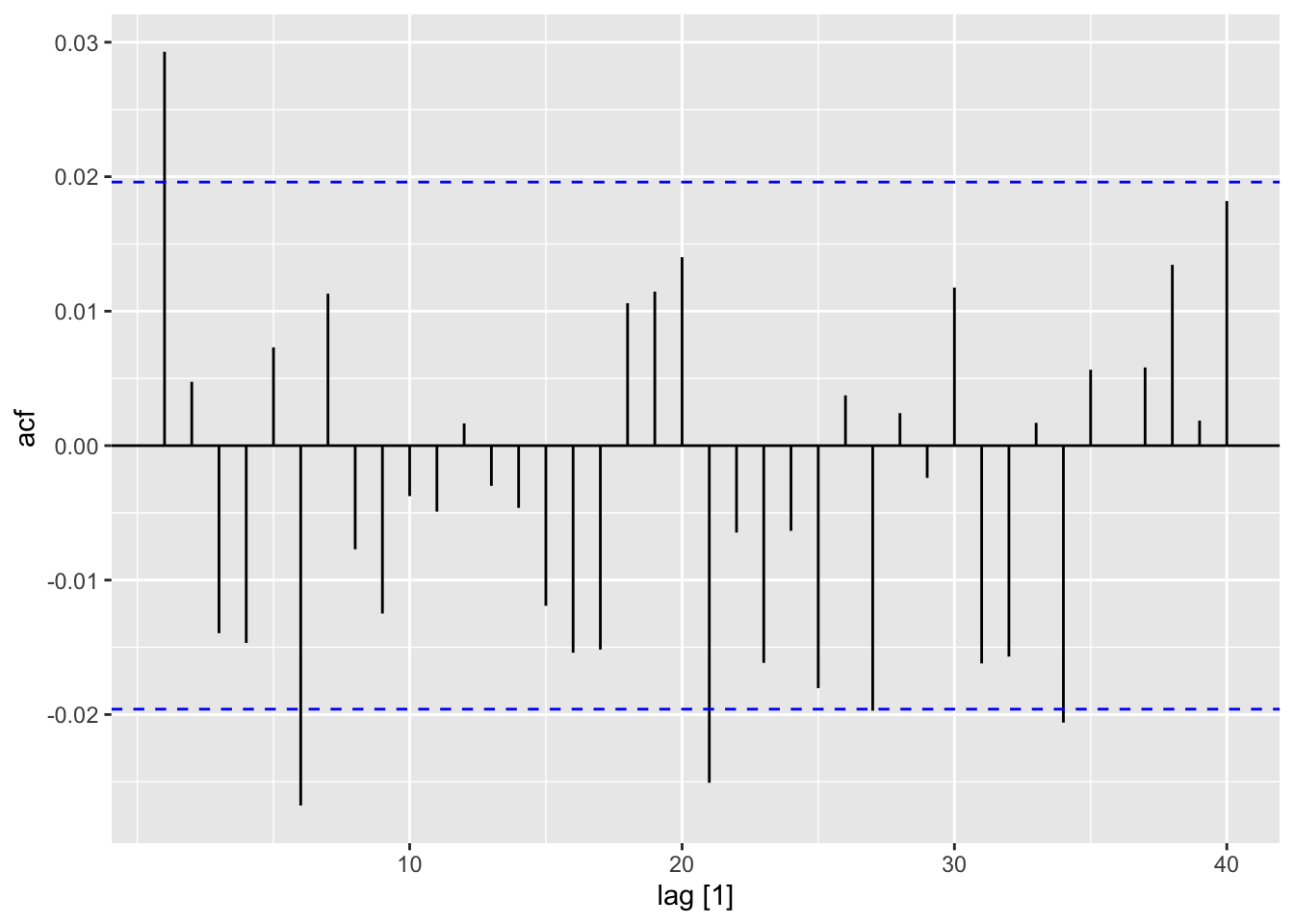

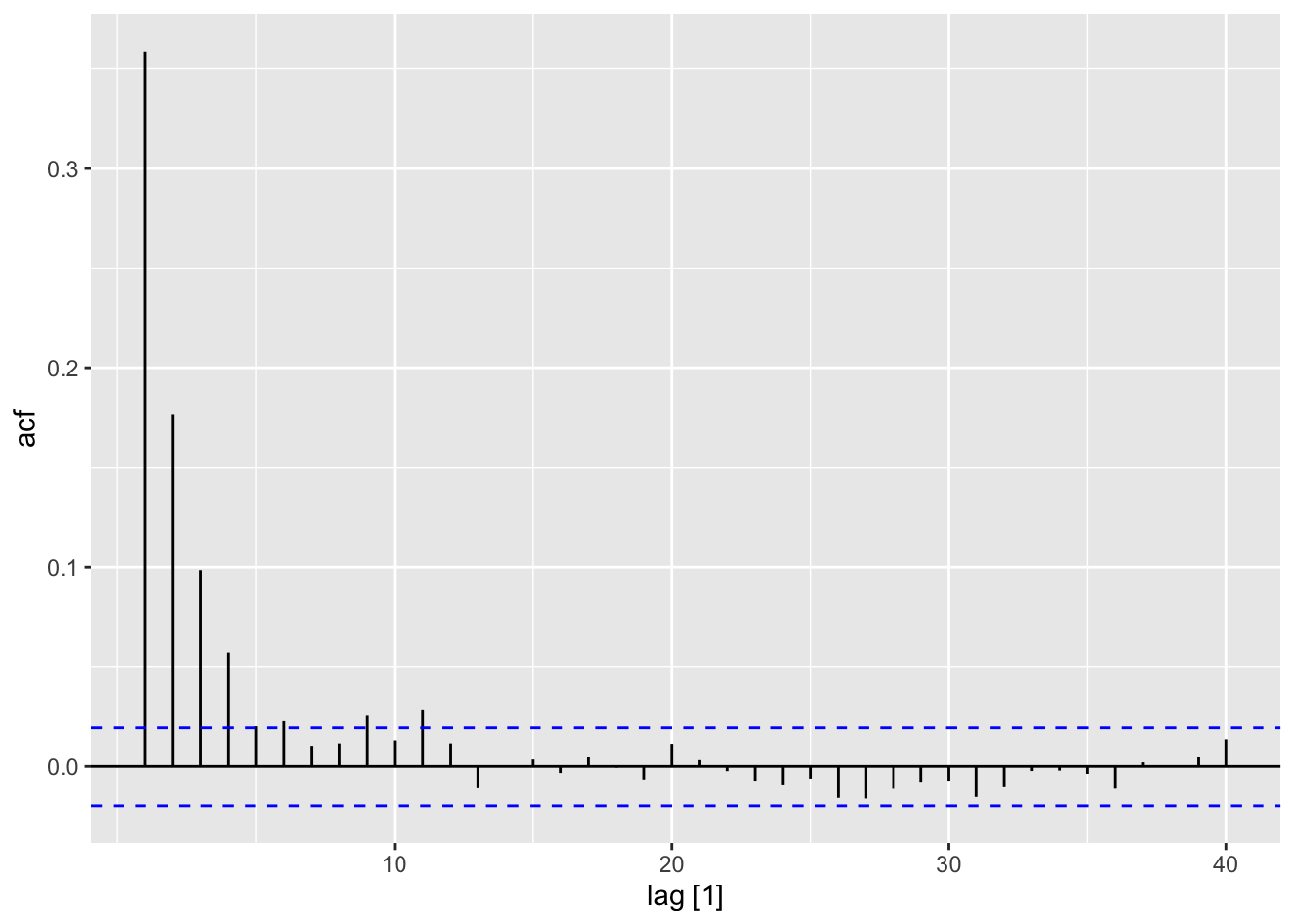

ACF(sim, y = a2) |>

autoplot()

a.garch <- garch(a, grad = "numerical", trace = FALSE)

confint(a.garch) 2.5 % 97.5 %

a0 0.0882393 0.1092903

a1 0.3307897 0.4023932

b1 0.1928344 0.2954660spec <- ugarchspec(

mean.model = list(armaOrder = c(0,0)),

variance.model = list(model = "sGARCH"),

distribution.model = "norm")

sim_garch <- ugarchfit(data = pull(sim,a), spec = spec)

confint(sim_garch) 2.5 % 97.5 %

mu -0.008260573 0.008253128

omega 0.088325823 0.109204574

alpha1 0.331527684 0.401653876

beta1 0.192934674 0.295362333library(tseries)

set.seed(1)

alpha0 <- 0.1

alpha1 <- 0.4

beta1 <- 0.2

w <- rnorm(10000)

a <- rep(0, 10000)

h <- rep(0, 10000)

for (i in 2:10000) {

h[i] <- alpha0 + alpha1 * (a[i - 1]^2) + beta1 * h[i - 1]

a[i] <- w[i] * sqrt(h[i])

}

acf(a)

acf(a^2)

a.garch <- garch(a, grad = "numerical", trace = FALSE)

confint(a.garch)pacman::p_load("rugarch")

set.seed(1)

sim <- tibble(

alpha0 = 0.1,

alpha1 = 0.4,

beta1 = 0.2,

w = rnorm(10000),

a = rep(0, 10000),

h = rep(0, 10000)) |>

mutate(index = 1:n()) |>

as_tsibble(index = index)

for (i in 2:10000) {

sim$h[i] <- sim$alpha0[1] + sim$alpha1[1] * (sim$a[i - 1]^2) + sim$beta1[1] * sim$h[i - 1]

sim$a[i] <- sim$w[i] * sqrt(sim$h[i])

}

sim <- mutate(sim, a2 = a^2)

ACF(sim, y = a) |>

autoplot()

ACF(sim, y = a2) |>

autoplot()

spec <- rurgarch::ugarchspec(

mean.model = list(armaOrder = c(0,0)),

variance.model = list(model = "sGARCH"),

distribution.model = "norm")

sim_garch <- ugarchfit(data = pull(sim,a), spec = spec)

confint(sim_garch)

# gd <- ugarchdistribution(garchfit, n.sim = 500, recursive = TRUE,

# recursive.length = 6000, recursive.window = 500, m.sim = 100,

# solver = 'hybrid')

#garchforecast <- ugarchforecast(fitORspec = garchfit, n.ahead = 5)Book code

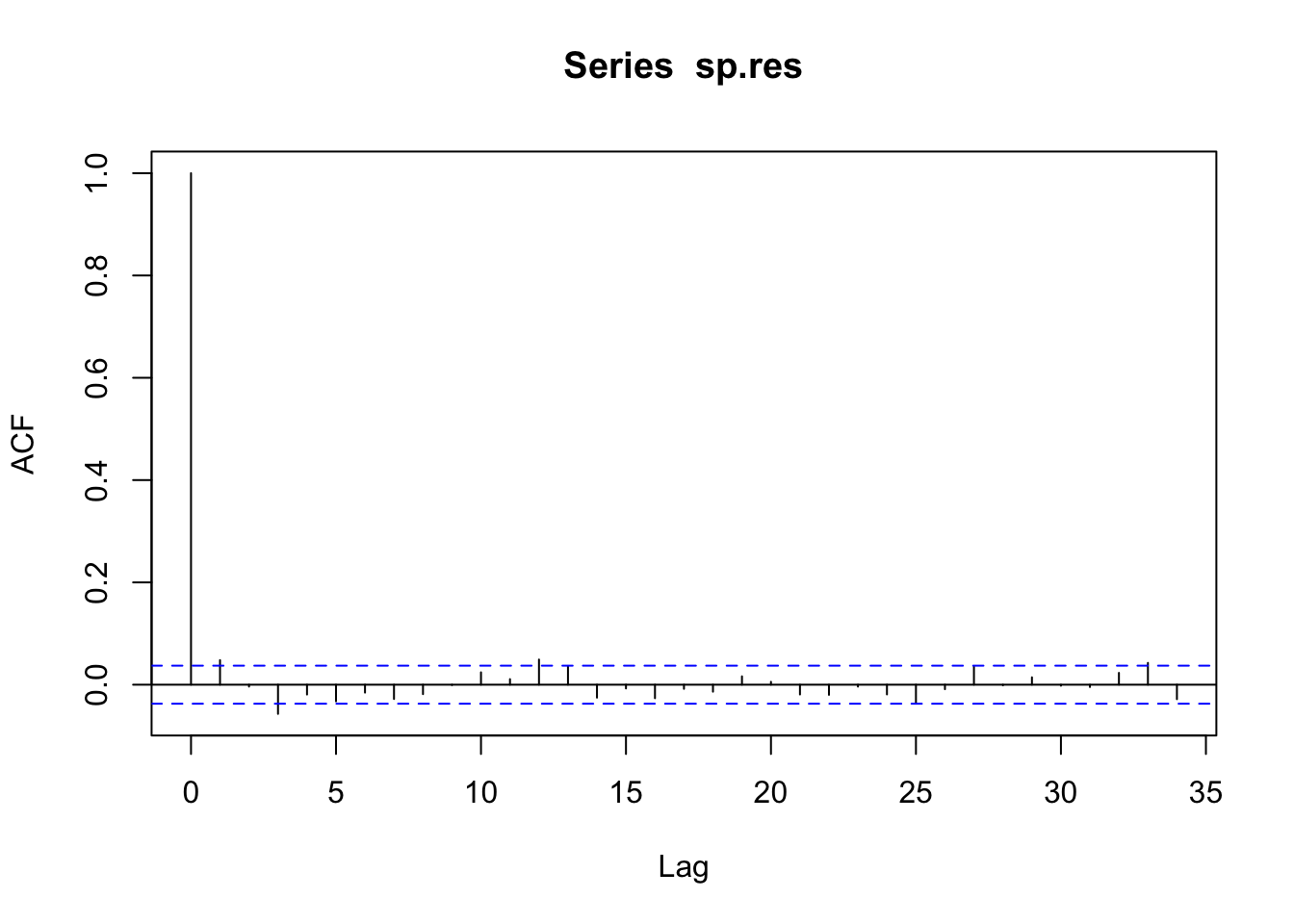

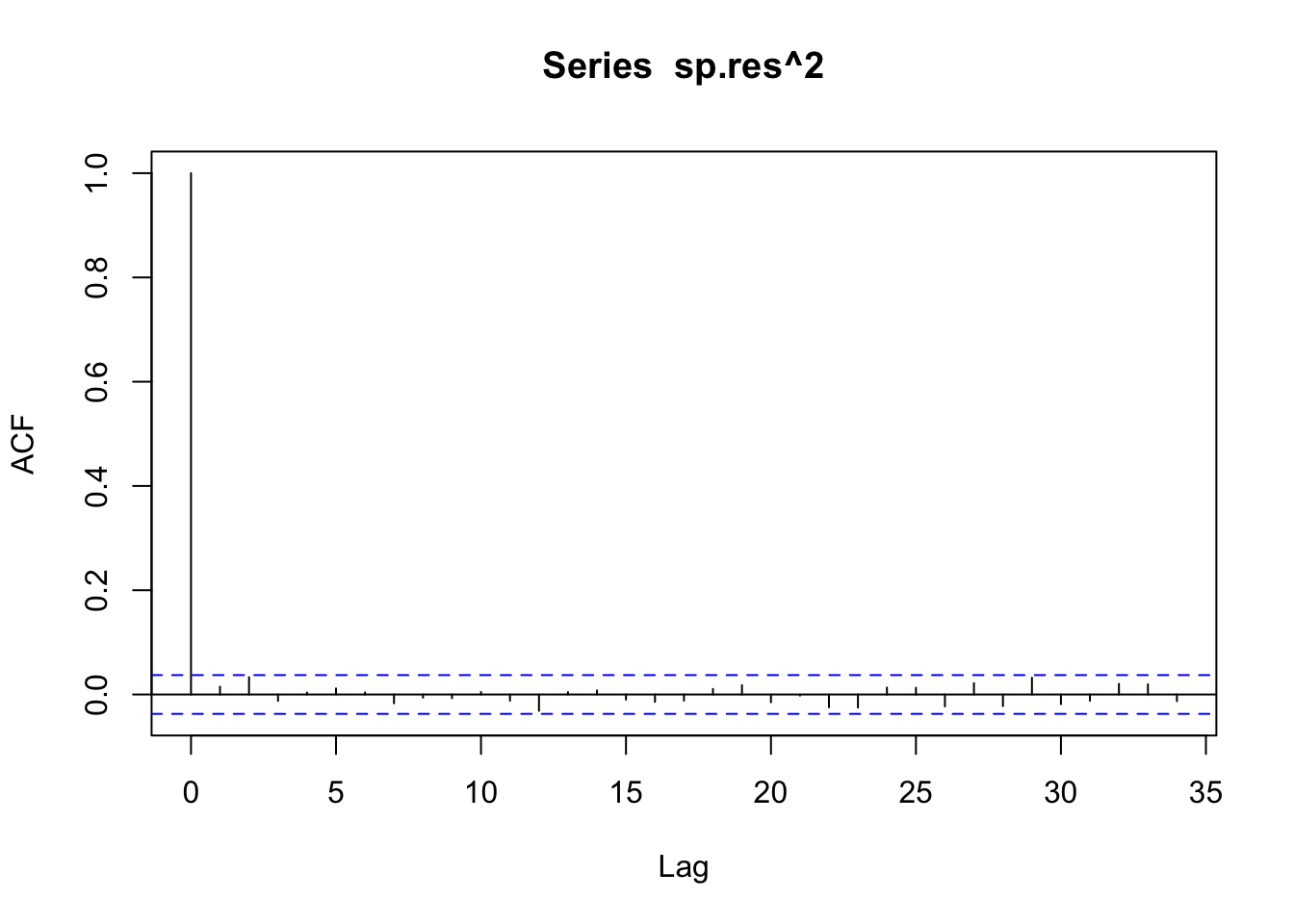

sp.garch <- garch(SP500, trace = F)

sp.res <- sp.garch$res[-1]

acf(sp.res)

Tidyverts code

dat <- tibble::tibble(sp500 = SP500) |>

mutate(index = 1:n()) |>

as_tsibble(index = index)

spec <- ugarchspec(

mean.model = list(armaOrder = c(0,0)),

variance.model = list(model = "sGARCH"),

distribution.model = "norm")

sp_garch <- ugarchfit(data = pull(dat, sp500), spec = spec)

dat <- dat |>

mutate(

.resid = residuals(sp_garch),

.resid2 = .resid^2)

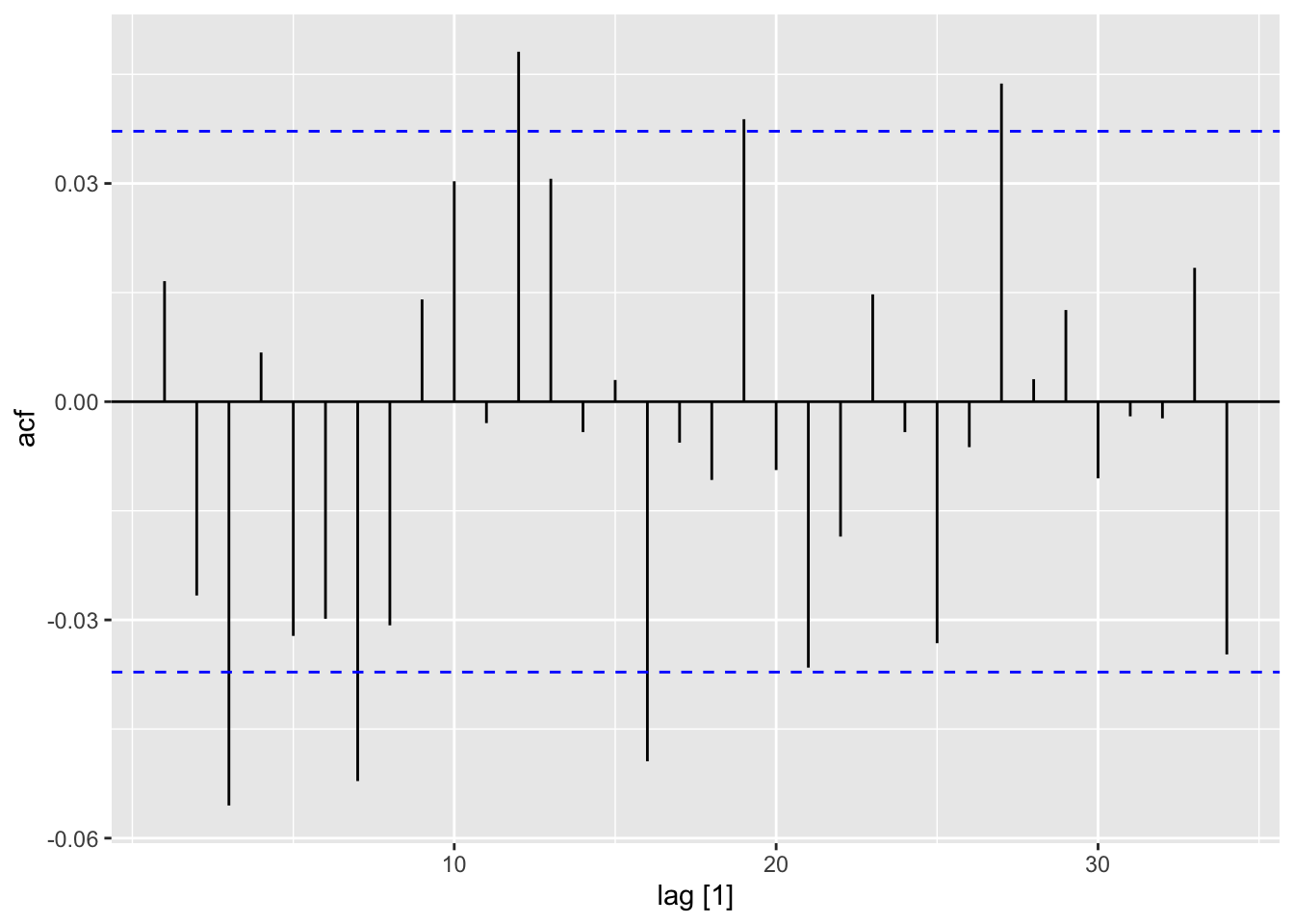

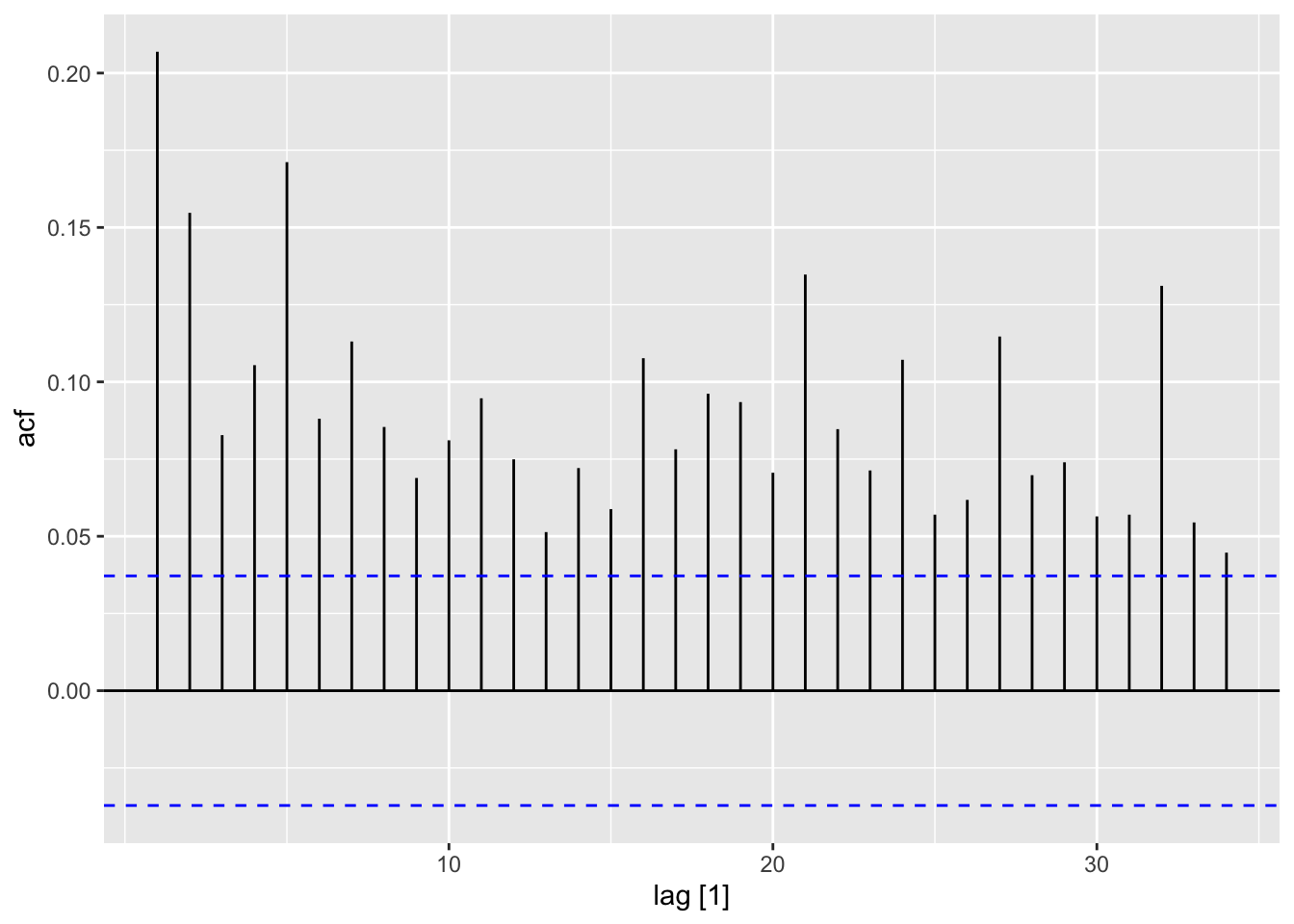

dat |>

ACF(y = .resid) |>

autoplot()

acf(sp.res^2)

dat |>

ACF(y = .resid2) |>

autoplot()

dat <- tibble::tibble(sp500 = SP500) |>

mutate(index = 1:n()) |>

as_tsibble(index = index)

spec <- ugarchspec(

mean.model = list(armaOrder = c(0,0)),

variance.model = list(model = "sGARCH"),

distribution.model = "norm")

sp_garch <- ugarchfit(data = pull(dat, sp500), spec = spec)

dat <- dat |>

mutate(

.resid = residuals(sp_garch),

.resid2 = .resid^2)

dat |>

ACF(y = .resid) |>

autoplot()

dat |>

ACF(y = .resid2) |>

autoplot()Book code

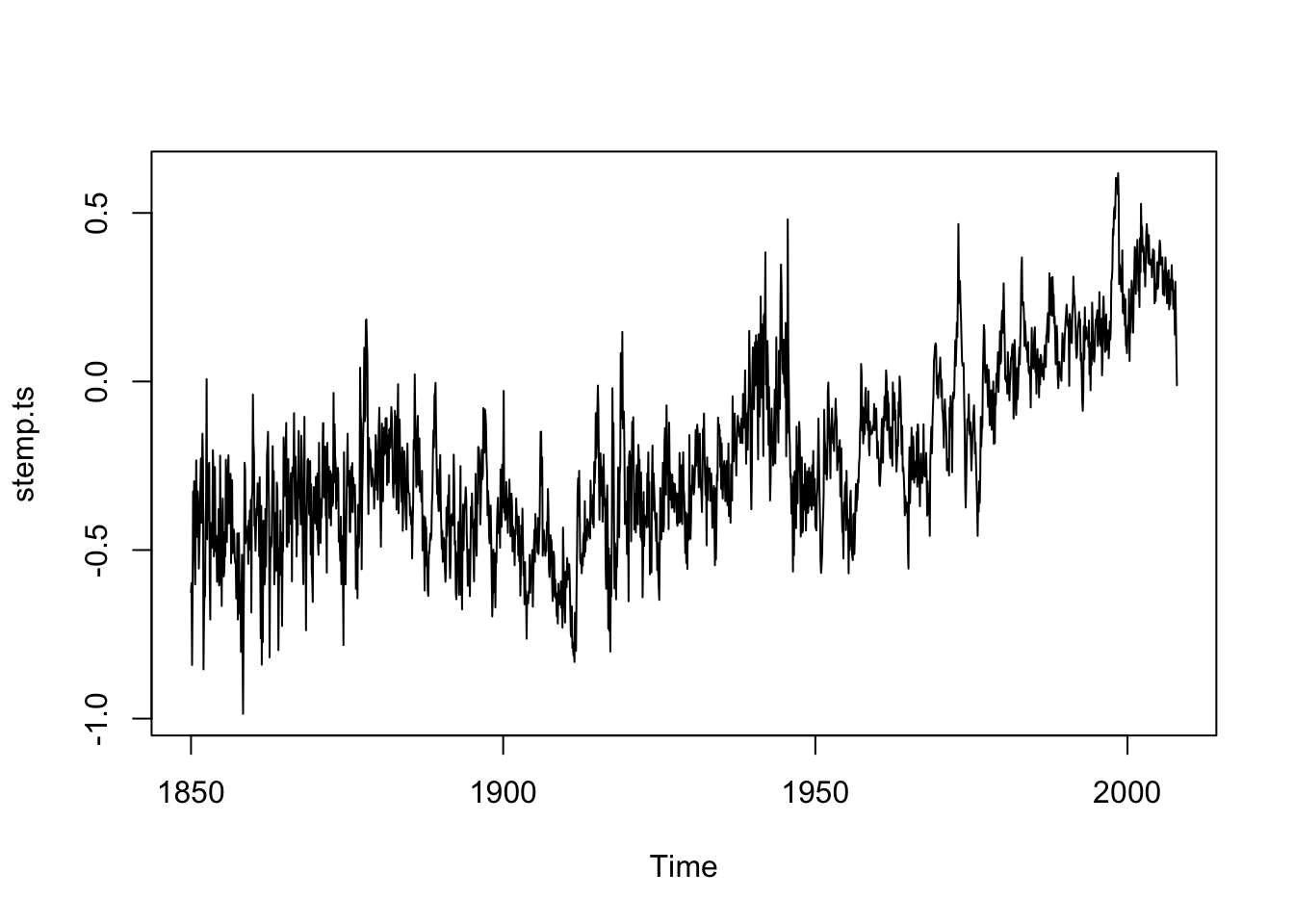

stemp <- scan("data/stemp.dat")

stemp.ts <- ts(stemp, start = 1850, freq = 12)

plot(stemp.ts)

stemp.best <- get.best.arima(stemp.ts, maxord = rep(2,6))

stemp.best[[3]][1] 1 1 2 2 0 1stemp.arima <- arima(stemp.ts, order = c(1,1,2),

seas = list(order = c(2,0,1), 12))

t(confint(stemp.arima)) ar1 ma1 ma2 sar1 sar2 sma1

2.5 % 0.8317390 -1.447400 0.3256700 0.8576802 -0.02501883 -0.9690534

97.5 % 0.9127946 -1.312553 0.4530475 1.0041396 0.07413424 -0.8507034Tidyverts code

stemp_ts <- tibble::tibble(stemp = scan("data/stemp.dat")) |>

mutate(

date = seq(

ymd("1850-01-01"),

by = "1 months",

length.out = n()),

year_month = tsibble::yearmonth(date)) |>

as_tsibble(index = year_month)

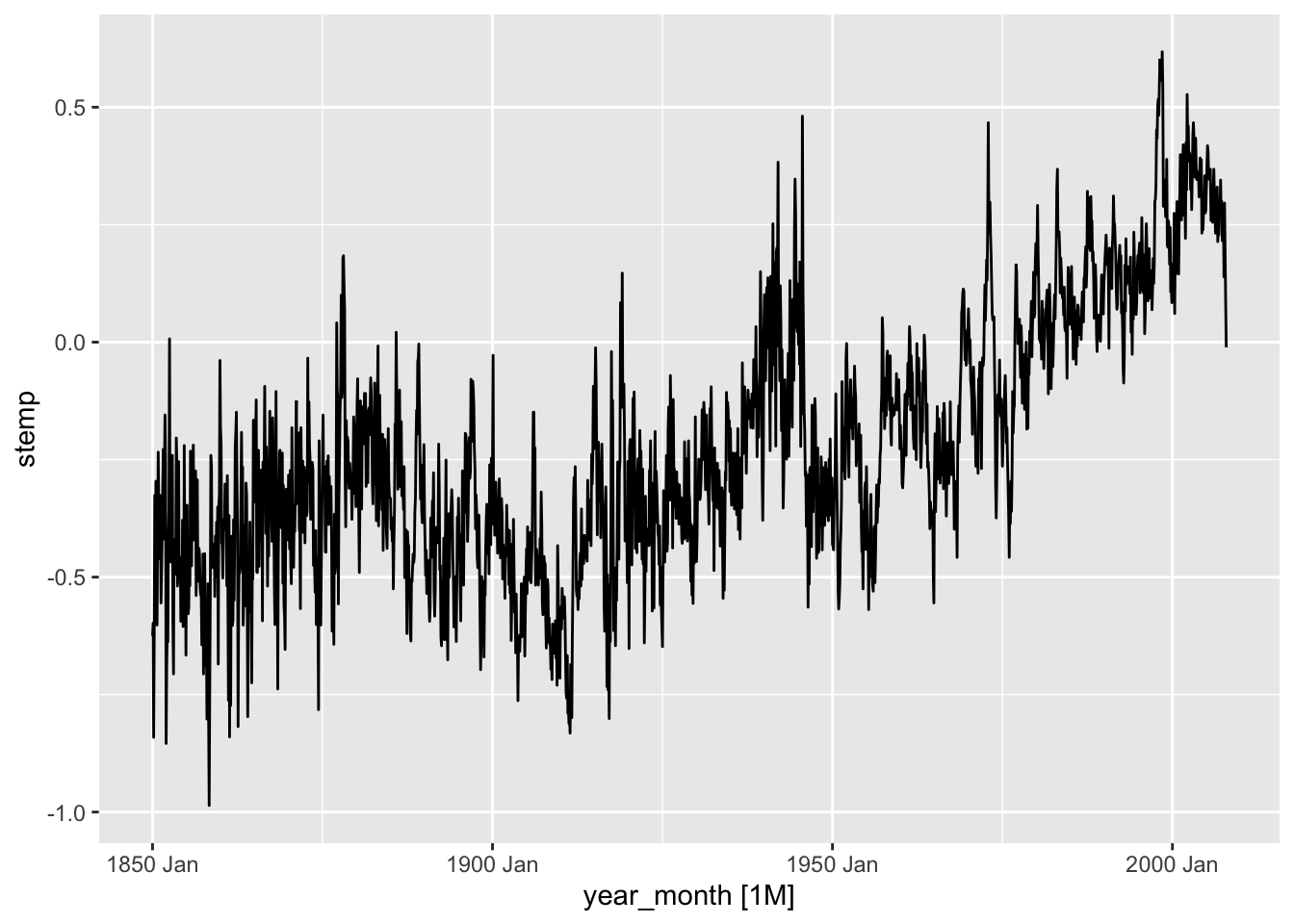

autoplot(stemp_ts)

stemp_best <- stemp_ts |>

model(

ar_model = ARIMA(stemp ~ 1 +

pdq(0:2, 0:2, 0:2) +

PDQ(0:2, 0:2, 0:2), approximation = TRUE),

book_arima = ARIMA(stemp ~ 1 +

pdq(1, 1, 2) +

PDQ(2, 0, 1), approximation = TRUE),

book_arima_reduced = ARIMA(stemp ~ 1 +

pdq(1, 1, 2) +

PDQ(1, 0, 1), approximation = TRUE),

)

tidy(stemp_best) |>

dplyr::filter(term != "constant") |>

mutate(

lb = round(estimate + qnorm(.025) * std.error, 3),

ub = round(estimate + qnorm(.975) * std.error, 3),

interval = paste0(lb, " , ", ub)

) |>

dplyr::select(.model, term, interval) |>

pivot_wider(names_from = .model, values_from = interval, values_fill = "-") |>

knitr::kable()| term | ar_model | book_arima | book_arima_reduced |

|---|---|---|---|

| ar1 | 0.449 , 0.546 | 0.838 , 0.917 | 0.835 , 0.913 |

| ar2 | 0.161 , 0.257 | - | - |

| ma1 | -0.99 , -0.954 | -1.452 , -1.319 | -1.45 , -1.317 |

| sar1 | -0.01 , 0.083 | 0.845 , 0.997 | 0.917 , 0.995 |

| sar2 | -0.028 , 0.065 | -0.023 , 0.077 | - |

| ma2 | - | 0.33 , 0.456 | 0.328 , 0.454 |

| sma1 | - | -0.964 , -0.837 | -0.968 , -0.859 |

stemp.arima <- arima(stemp.ts, order = c(1,1,2),

seas = list(order = c(1,0,1), 12))

t(confint(stemp.arima)) ar1 ma1 ma2 sar1 sma1

2.5 % 0.8303969 -1.445048 0.3242572 0.9243526 -0.9694910

97.5 % 0.9108148 -1.311229 0.4508903 0.9956640 -0.8679276tidy(stemp_best) |>

dplyr::filter(term != "constant") |>

mutate(

lb = round(estimate + qnorm(.025) * std.error, 3),

ub = round(estimate + qnorm(.975) * std.error, 3),

interval = paste0(lb, " , ", ub)

) |>

dplyr::select(.model, term, interval) |>

pivot_wider(names_from = .model, values_from = interval, values_fill = "-") |>

knitr::kable()| term | ar_model | book_arima | book_arima_reduced |

|---|---|---|---|

| ar1 | 0.449 , 0.546 | 0.838 , 0.917 | 0.835 , 0.913 |

| ar2 | 0.161 , 0.257 | - | - |

| ma1 | -0.99 , -0.954 | -1.452 , -1.319 | -1.45 , -1.317 |

| sar1 | -0.01 , 0.083 | 0.845 , 0.997 | 0.917 , 0.995 |

| sar2 | -0.028 , 0.065 | -0.023 , 0.077 | - |

| ma2 | - | 0.33 , 0.456 | 0.328 , 0.454 |

| sma1 | - | -0.964 , -0.837 | -0.968 , -0.859 |

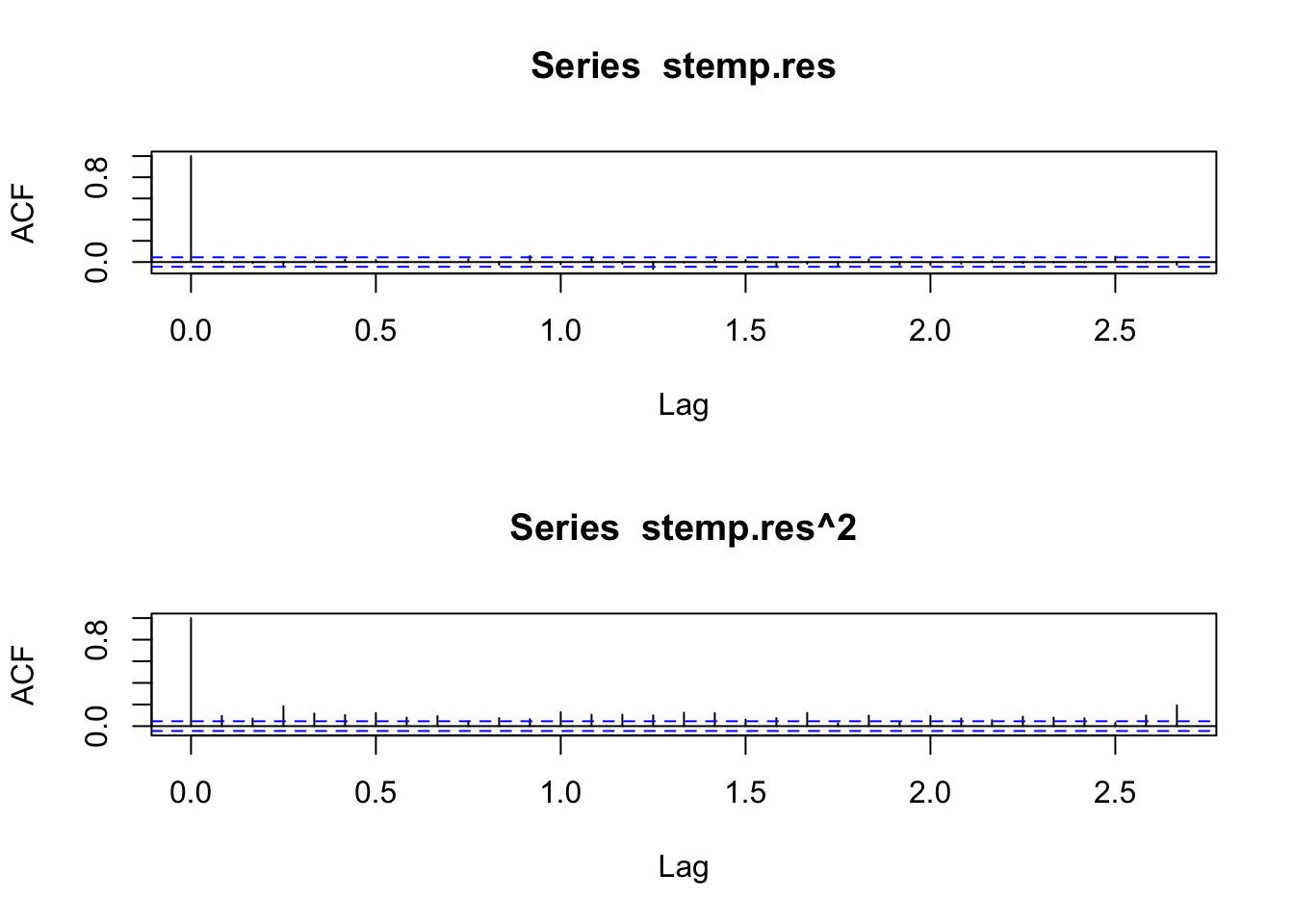

stemp.res <- resid(stemp.arima)

layout(1:2)

acf(stemp.res)

acf(stemp.res^2)

stemp_res <- stemp_best |>

dplyr::select(book_arima_reduced) |>

residuals() |>

mutate(.resid2 = .resid^2)

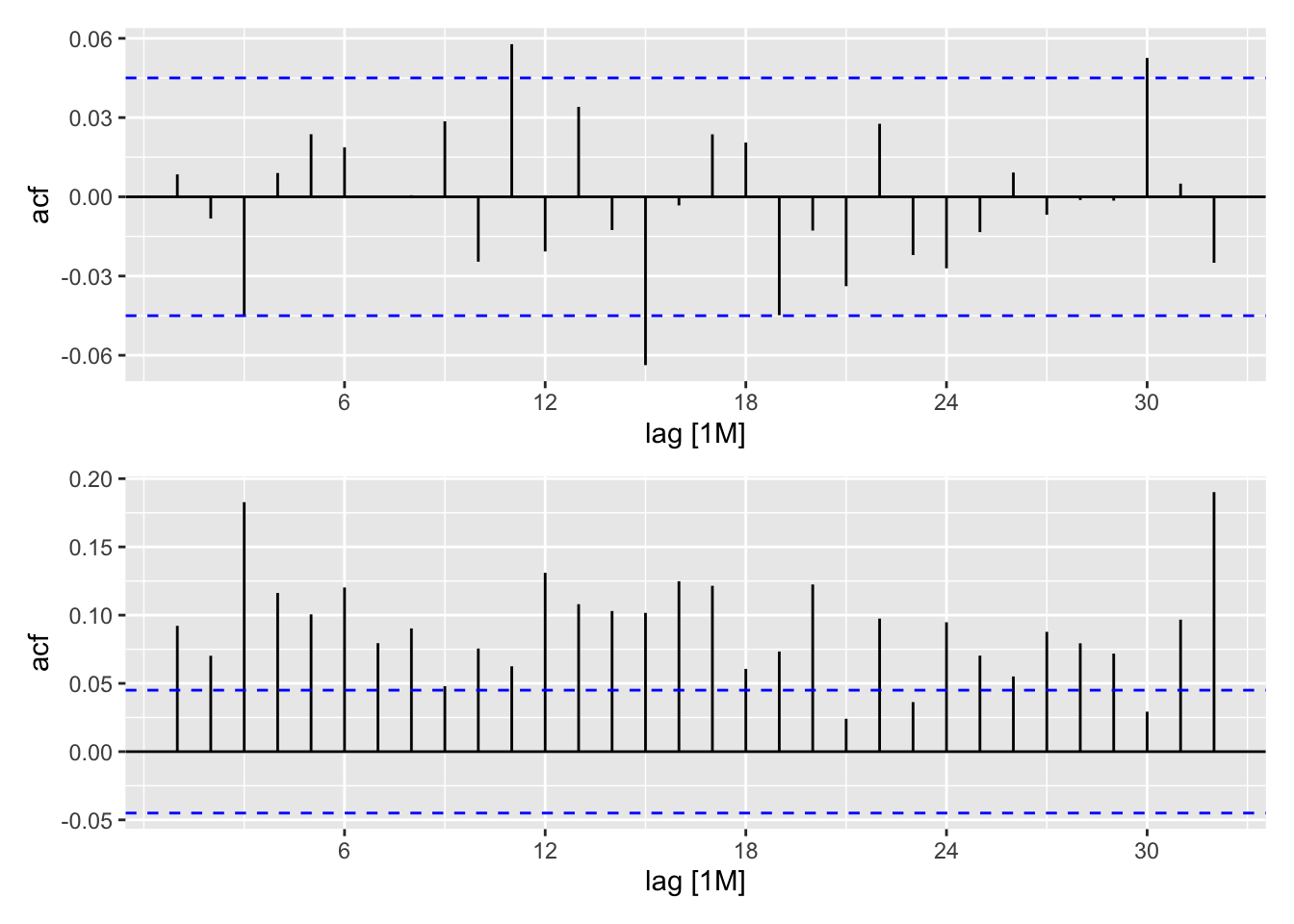

rp <- ACF(stemp_res, y = .resid) |> autoplot()

r2p <- ACF(stemp_res, y = .resid2) |> autoplot()

rp / r2p

stemp.garch <- garch(stemp.res, trace = F)

confint(stemp.garch) 2.5 % 97.5 %

a0 1.064246e-05 0.0001485812

a1 3.299179e-02 0.0652567733

b1 9.249316e-01 0.9630787389spec <- ugarchspec(

mean.model = list(armaOrder = c(0,0)),

variance.model = list(model = "sGARCH"),

distribution.model = "norm")

stemp_garch <- ugarchfit(data = pull(stemp_res, .resid), spec = spec)

confint(stemp_garch) 2.5 % 97.5 %

mu -3.974225e-03 0.0044798310

omega 2.246930e-06 0.0001533503

alpha1 2.884755e-02 0.0691398769

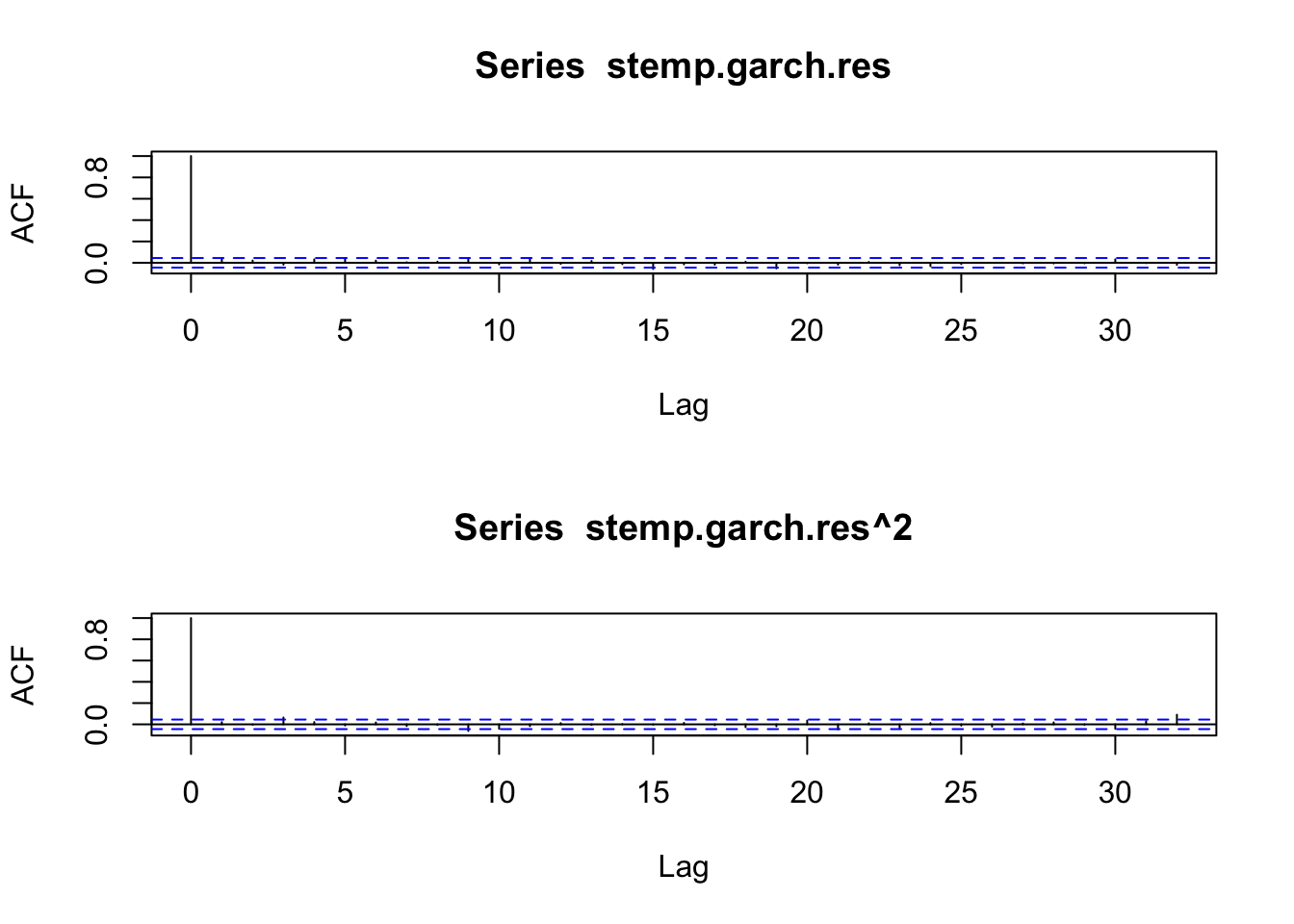

beta1 9.215237e-01 0.9670927847stemp.garch.res <- resid(stemp.garch)[-1]

layout(1:2)

acf(stemp.garch.res)

acf(stemp.garch.res^2)

stemp_res <- stemp_res |>

mutate(

.resid_garch = residuals(stemp_garch),

.resid2_garch = .resid_garch^2)

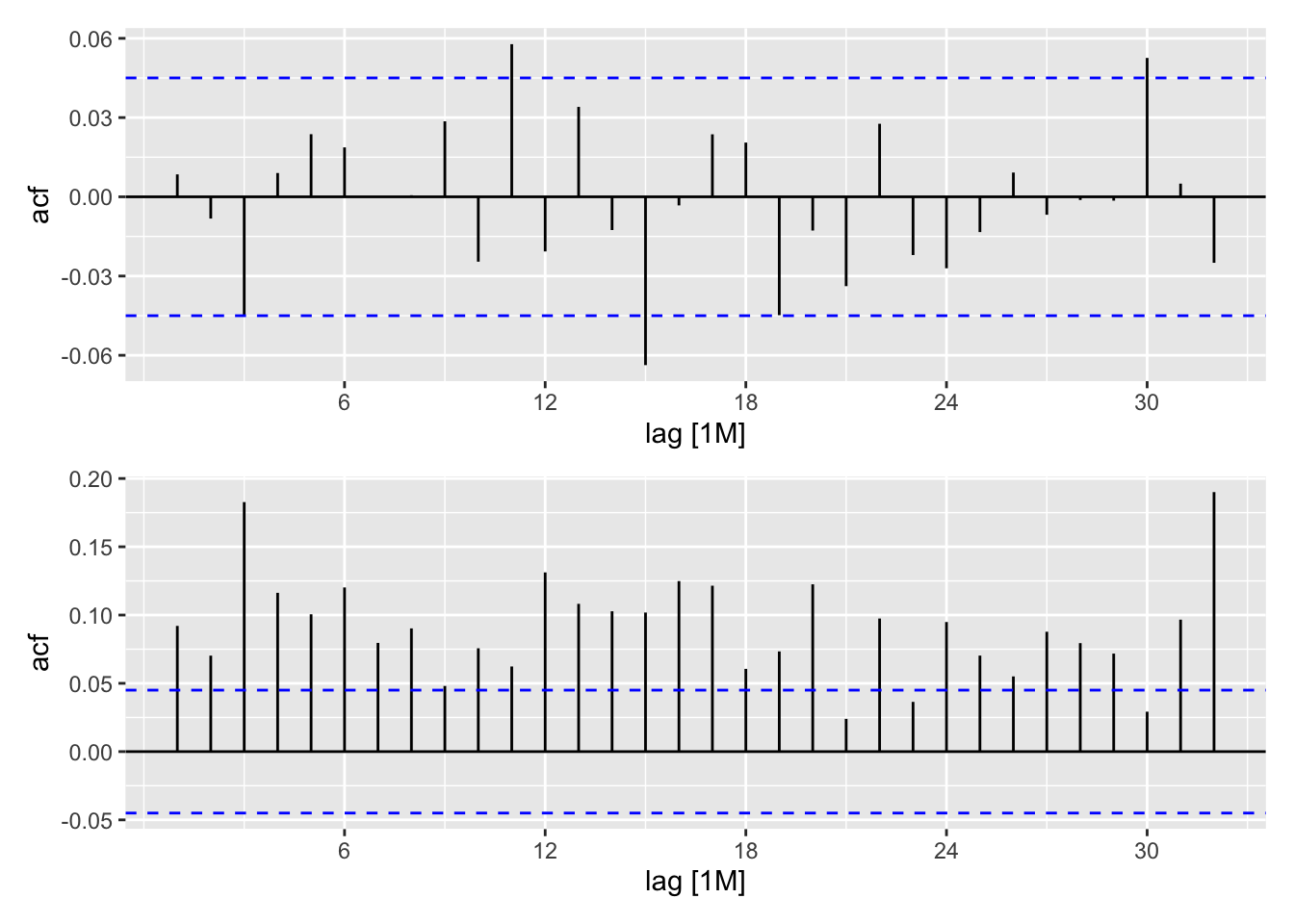

rgp <- ACF(stemp_res, y = .resid_garch) |> autoplot()

rg2p <- ACF(stemp_res, y = .resid2_garch) |> autoplot()

rgp / rg2p

stemp <- scan("data/stemp.dat")

stemp.ts <- ts(stemp, start = 1850, freq = 12)

plot(stemp.ts)

stemp.best <- get.best.arima(stemp.ts, maxord = rep(2,6))

stemp.best[[3]]

stemp.arima <- arima(stemp.ts, order = c(1,1,2),

seas = list(order = c(2,0,1), 12))

t(confint(stemp.arima))

stemp.arima <- arima(stemp.ts, order = c(1,1,2),

seas = list(order = c(1,0,1), 12))

t(confint(stemp.arima))

stemp.res <- resid(stemp.arima)

layout(1:2)

acf(stemp.res)

acf(stemp.res^2)

stemp.garch <- garch(stemp.res, trace = F)

confint(stemp.garch)

stemp.garch.res <- resid(stemp.garch)[-1]

acf(stemp.garch.res)

acf(stemp.garch.res^2)stemp_ts <- tibble::tibble(stemp = scan("data/stemp.dat")) |>

mutate(

date = seq(

ymd("1850-01-01"),

by = "1 months",

length.out = n()),

year_month = tsibble::yearmonth(date)) |>

as_tsibble(index = year_month)

autoplot(stemp_ts)

stemp_best <- stemp_ts |>

model(

ar_model = ARIMA(stemp ~ 1 +

pdq(0:2, 0:2, 0:2) +

PDQ(0:2, 0:2, 0:2), approximation = TRUE),

book_arima = ARIMA(stemp ~ 1 +

pdq(1, 1, 2) +

PDQ(2, 0, 1), approximation = TRUE),

book_arima_reduced = ARIMA(stemp ~ 1 +

pdq(1, 1, 2) +

PDQ(1, 0, 1), approximation = TRUE),

)

tidy(stemp_best) |>

dplyr::filter(term != "constant") |>

mutate(

lb = round(estimate + qnorm(.025) * std.error, 3),

ub = round(estimate + qnorm(.975) * std.error, 3),

interval = paste0(lb, " , ", ub)

) |>

dplyr::select(.model, term, interval) |>

pivot_wider(names_from = .model, values_from = interval, values_fill = "-") |>

knitr::kable()

stemp_res <- stemp_best |>

dplyr::select(book_fit_reduced) |>

residuals() |>

mutate(.resid2 = .resid^2)

rp <- ACF(stemp_res, y = .resid) |> autoplot()

r2p <- ACF(stemp_res, y = .resid2) |> autoplot()

rp / r2p

spec <- ugarchspec(

mean.model = list(armaOrder = c(0,0)),

variance.model = list(model = "sGARCH"),

distribution.model = "norm")

stemp_garch <- ugarchfit(data = pull(stemp_res, .resid), spec = spec)

confint(stemp_garch)

stemp.garch <- garch(stemp.res, trace = F)

t(confint(stemp.garch)

stemp_res <- stemp_res |>

mutate(

.resid_garch = residuals(stemp_garch),

.resid2_garch = .resid_garch^2)

rgp <- ACF(stemp_res, y = .resid_garch) |> autoplot()

rg2p <- ACF(stemp_res, y = .resid2_garch) |> autoplot()

rgp / rg2pR commands used in examplesrugarch::ugarchspec(): Univariate GARCH Specificationrugarch::ugarchfit(): Univariate GARCH Fittingstats::confint(): Confidence Intervals for Model Parameters