set.seed(1)

w <- rnorm(100)

plot(w, type = "l")

Throughout this book, we will often fit models to data that we have simulated and attempt to recover the underlying model parameters. At first sight, this might seem odd, given that the parameters are used to simulate the data so that we already know at the outset the values the parameters should take. However, the procedure is useful for a number of reasons. In particular, to be able to simulate data using a model requires that the model formulation be correctly understood. If the model is understood but incorrectly implemented, then the parameter estimates from the fitted model may deviate significantly from the underlying model values used in the simulation. Simulation can therefore help ensure that the model is both correctly understood and correctly implemented.

R” Modern LookBook code

set.seed(1)

w <- rnorm(100)

plot(w, type = "l")

Tidyverts code

pacman::p_load("tsibble", "fable", "feasts",

"tsibbledata", "fable.prophet", "tidyverse", "patchwork")

set.seed(1)

wd <- tibble(

x = 1:100,

y = rnorm(100))

wd |> ggplot(aes(x = x, y = y)) + geom_line()

x <- seq(-3, 3, length = 1000)

hist(rnorm(100), prob = T)

points(x, dnorm(x), type = "l")

xd <- tibble(

x = seq(-3, 3, length = 1000),

norm = rnorm(1000),

density = dnorm(x)

)

xd |>

ggplot(aes(x = norm)) +

geom_histogram(aes(y = after_stat(density)),

color = "white", fill = "darkgrey") +

geom_line(aes(x = x, y = density)) +

theme_bw()

set.seed(1)

wd <- tibble(

x = 1:100,

y = rnorm(100))

wd |> ggplot(aes(x = x, y = y)) + geom_line()

xd <- tibble(

x = seq(-3, 3, length = 1000),

norm = rnorm(1000),

density = dnorm(x)

)

xd |>

ggplot(aes(x = norm)) +

geom_histogram(aes(y = after_stat(density)),

color = "white", fill = "darkgrey") +

geom_line(aes(x = x, y = density)) +

theme_bw()Book code

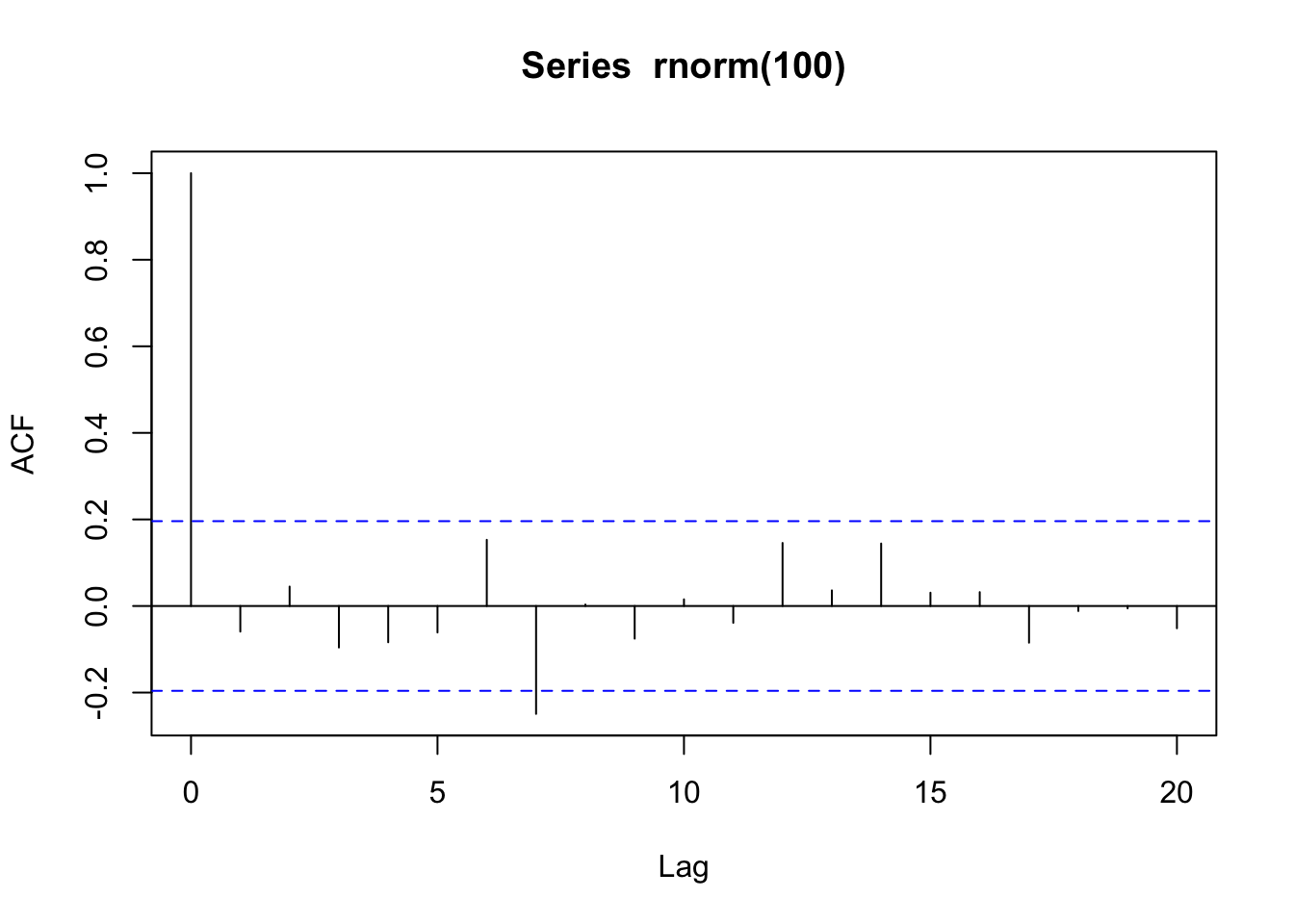

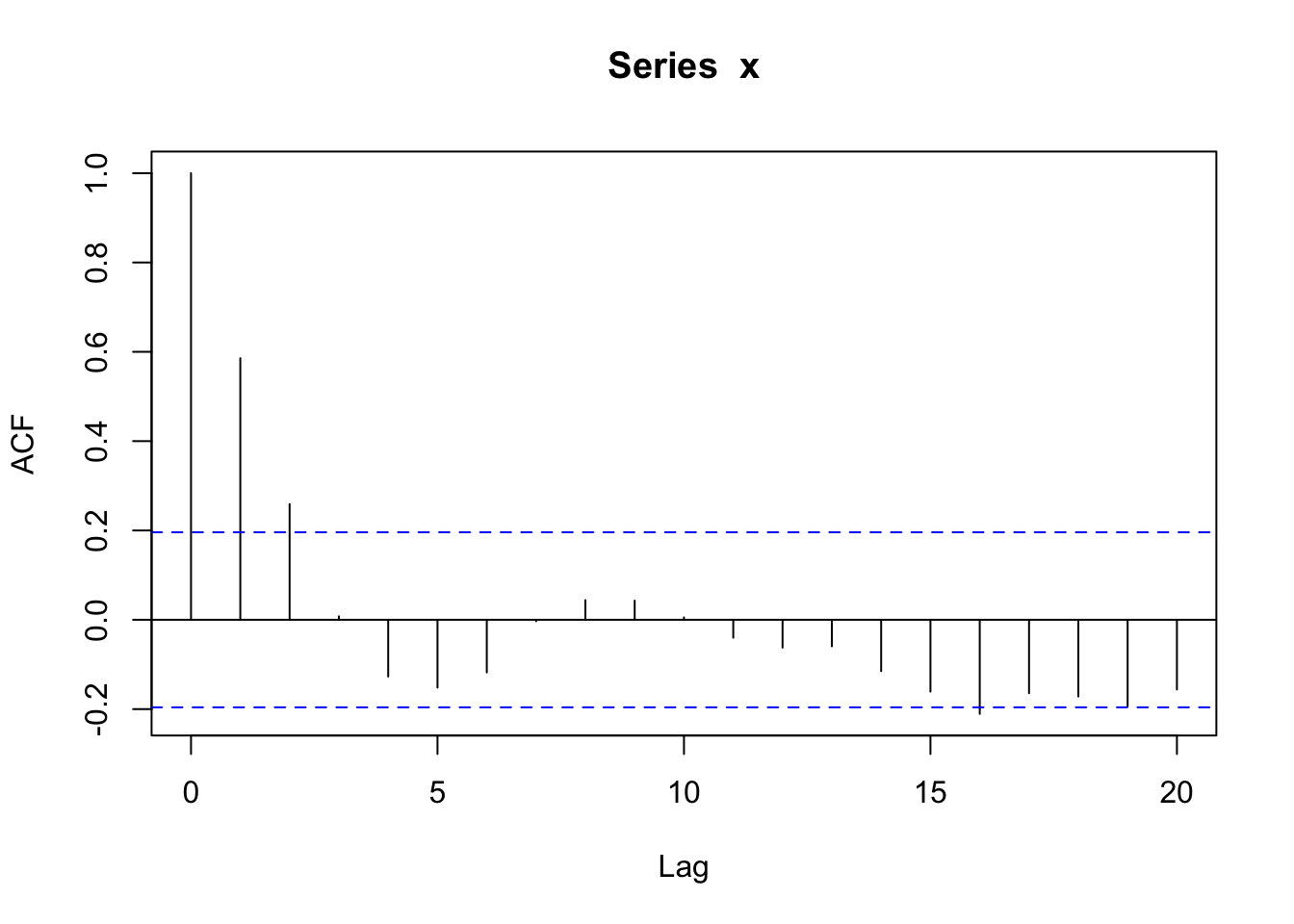

set.seed(2)

acf(rnorm(100))

Tidyverts code

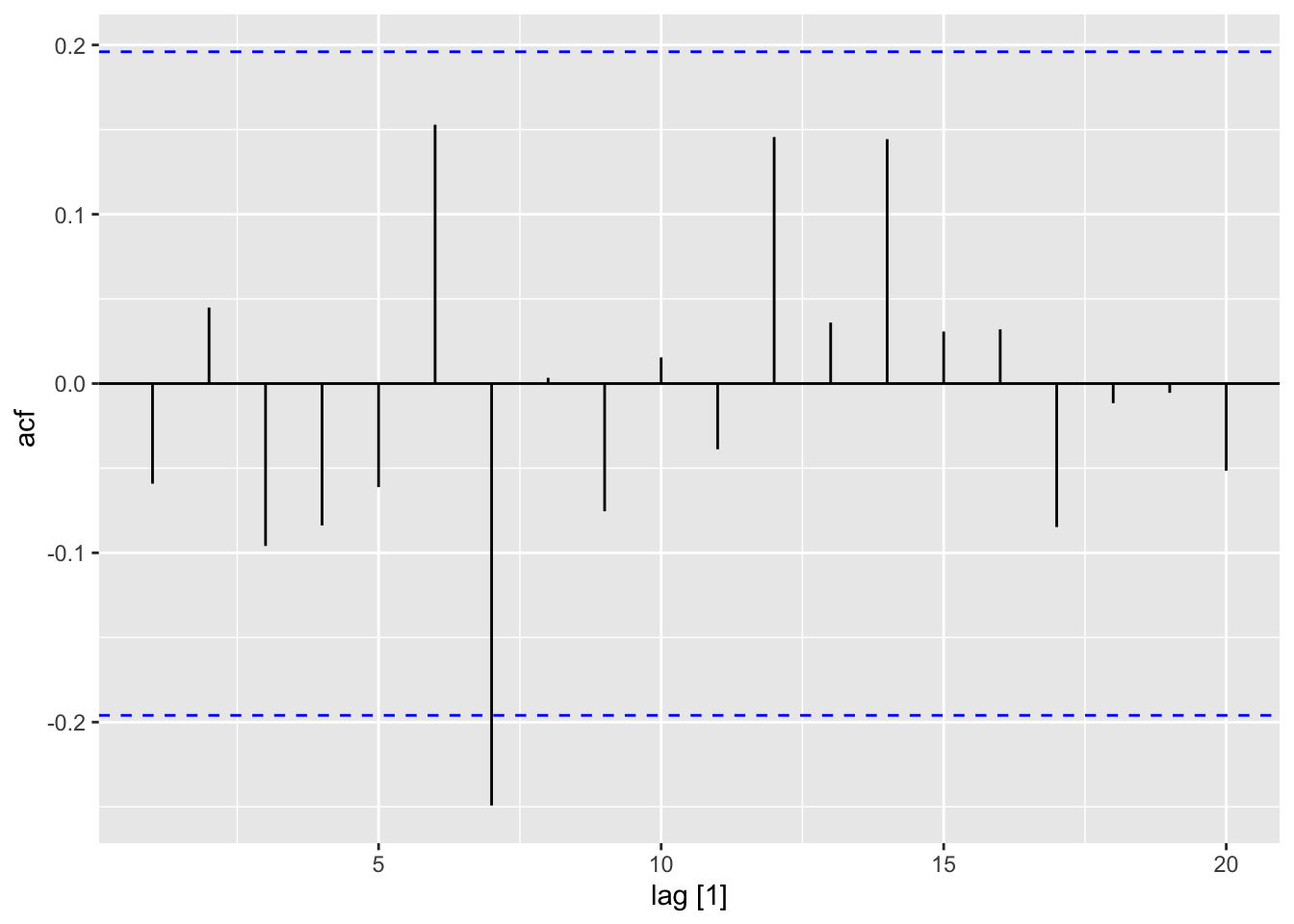

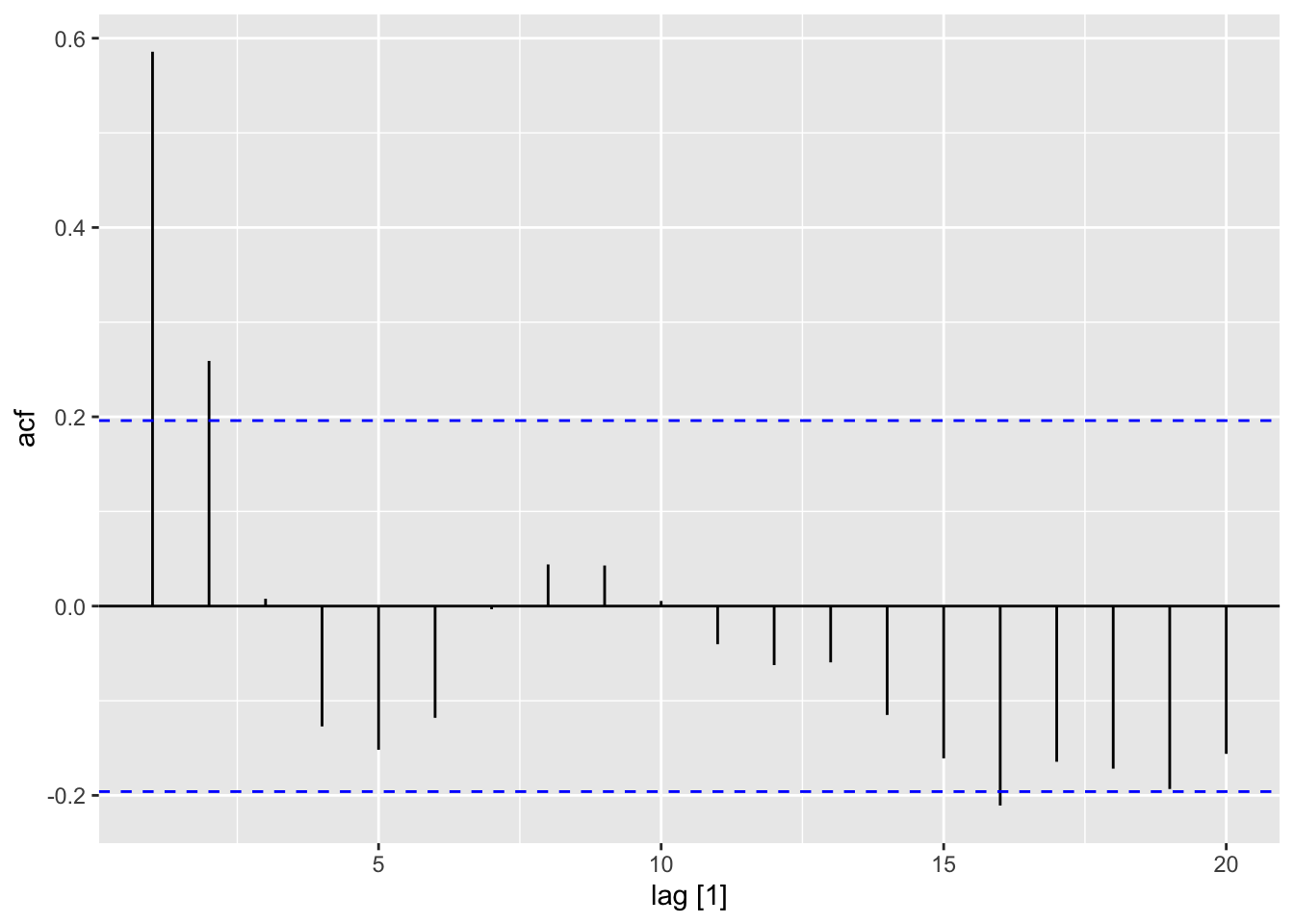

set.seed(2)

tsibble(seq = 1:100,

values = rnorm(100),

index = seq) |>

ACF(values) |>

autoplot()

Book code

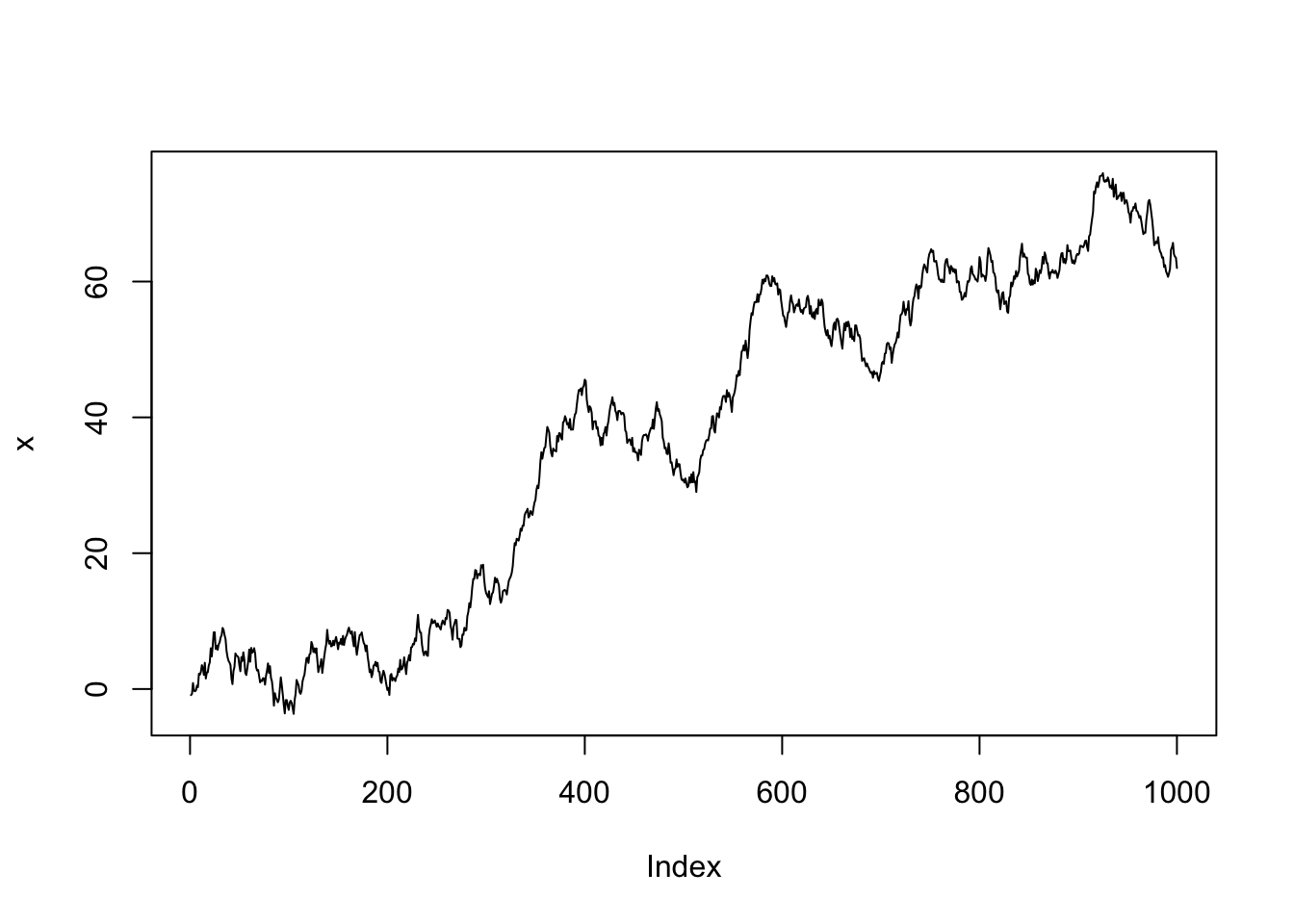

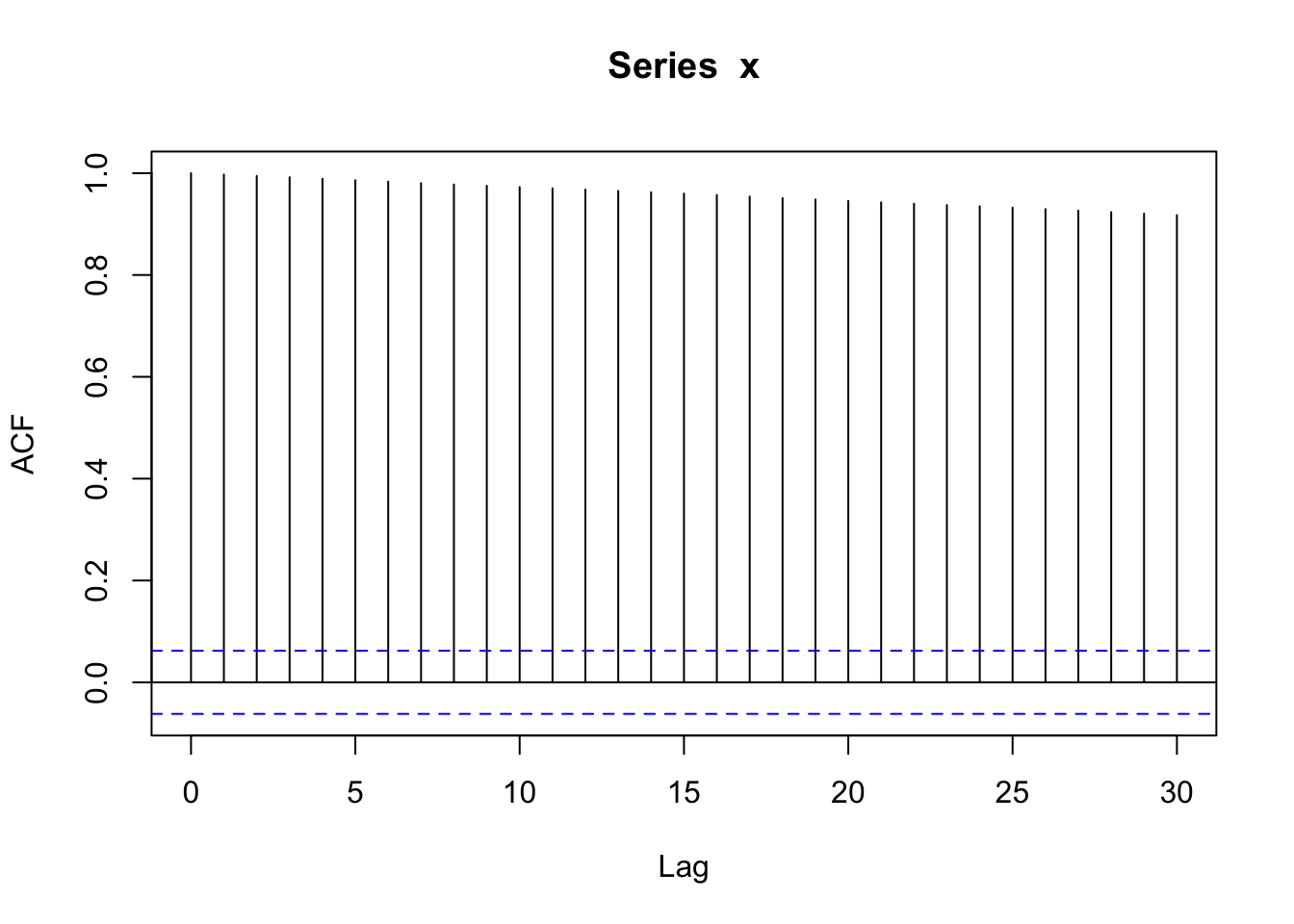

set.seed(2)

x <- w <- rnorm(1000)

for (t in 2:1000) x[t] <- x[t - 1] + w[t]

plot(x, type = "l")

Tidyverts code

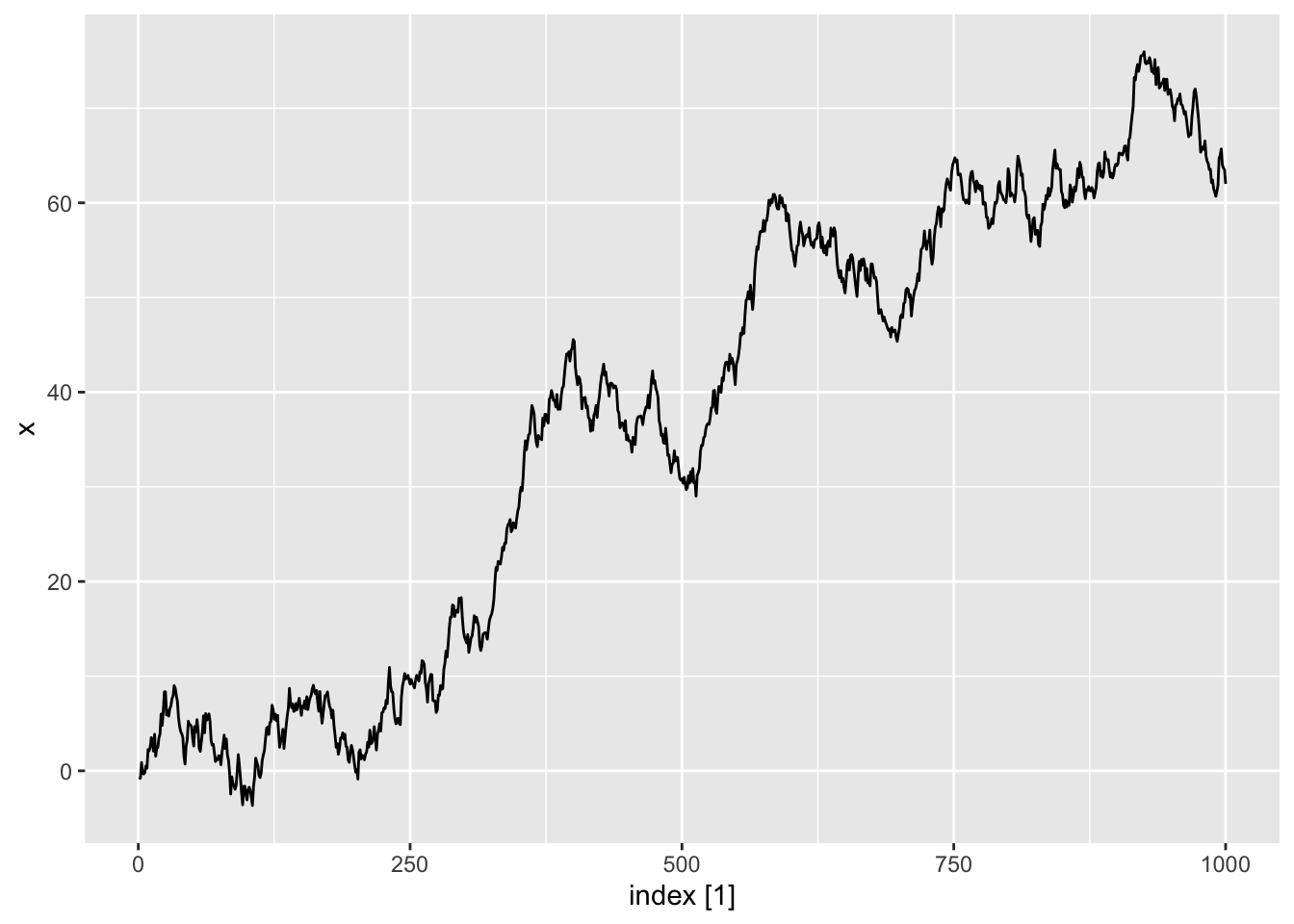

set.seed(2)

dat <- tibble(w = rnorm(1000)) |>

mutate(

index = 1:n(),

x = purrr::accumulate2(

lag(w), w,

\(acc, nxt, w) acc + w,

.init = 0)[-1]) |>

tsibble::as_tsibble(index = index)

autoplot(dat, .var = x)

acf(x)

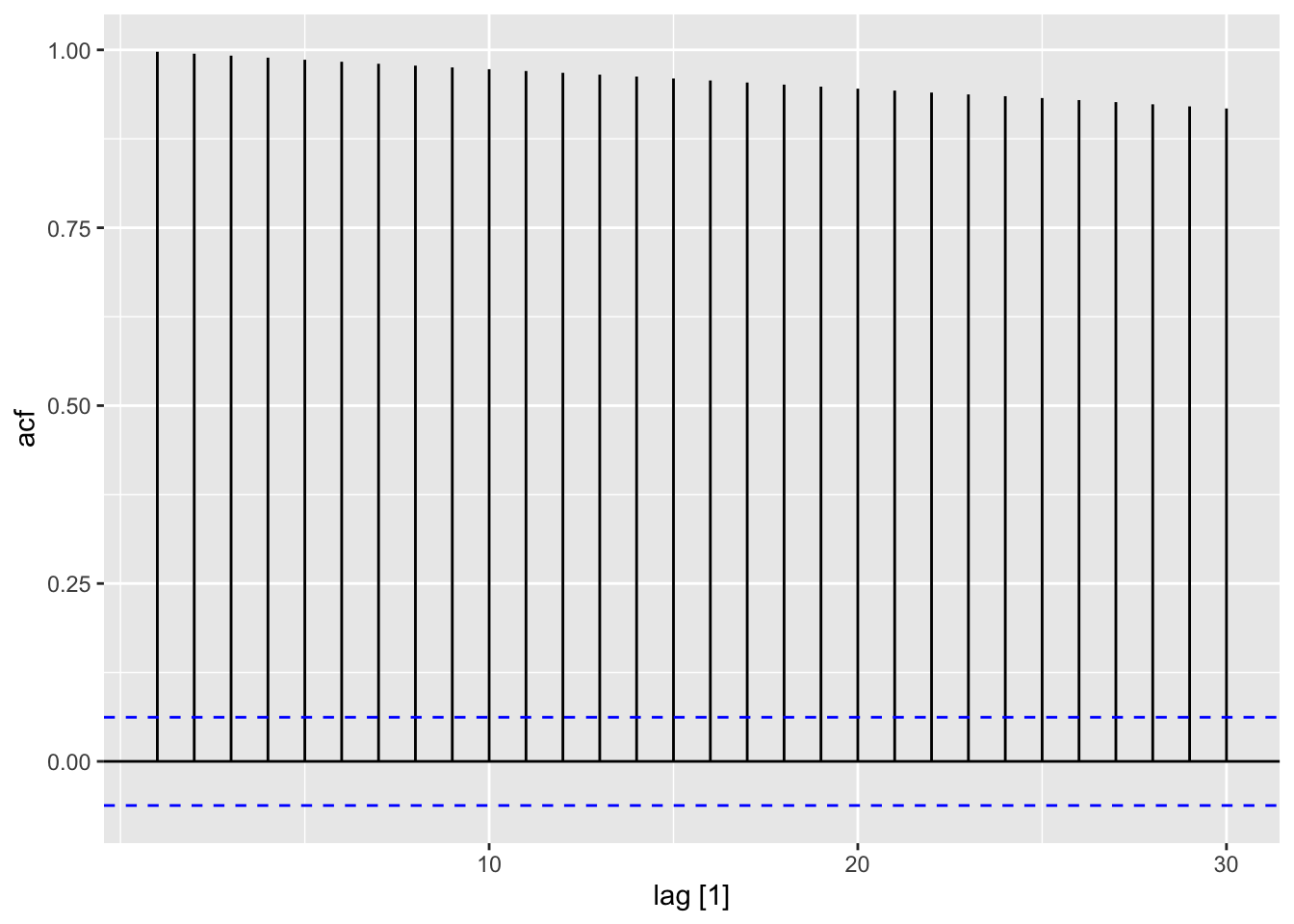

ACF(dat, x) |>

autoplot()

Book code

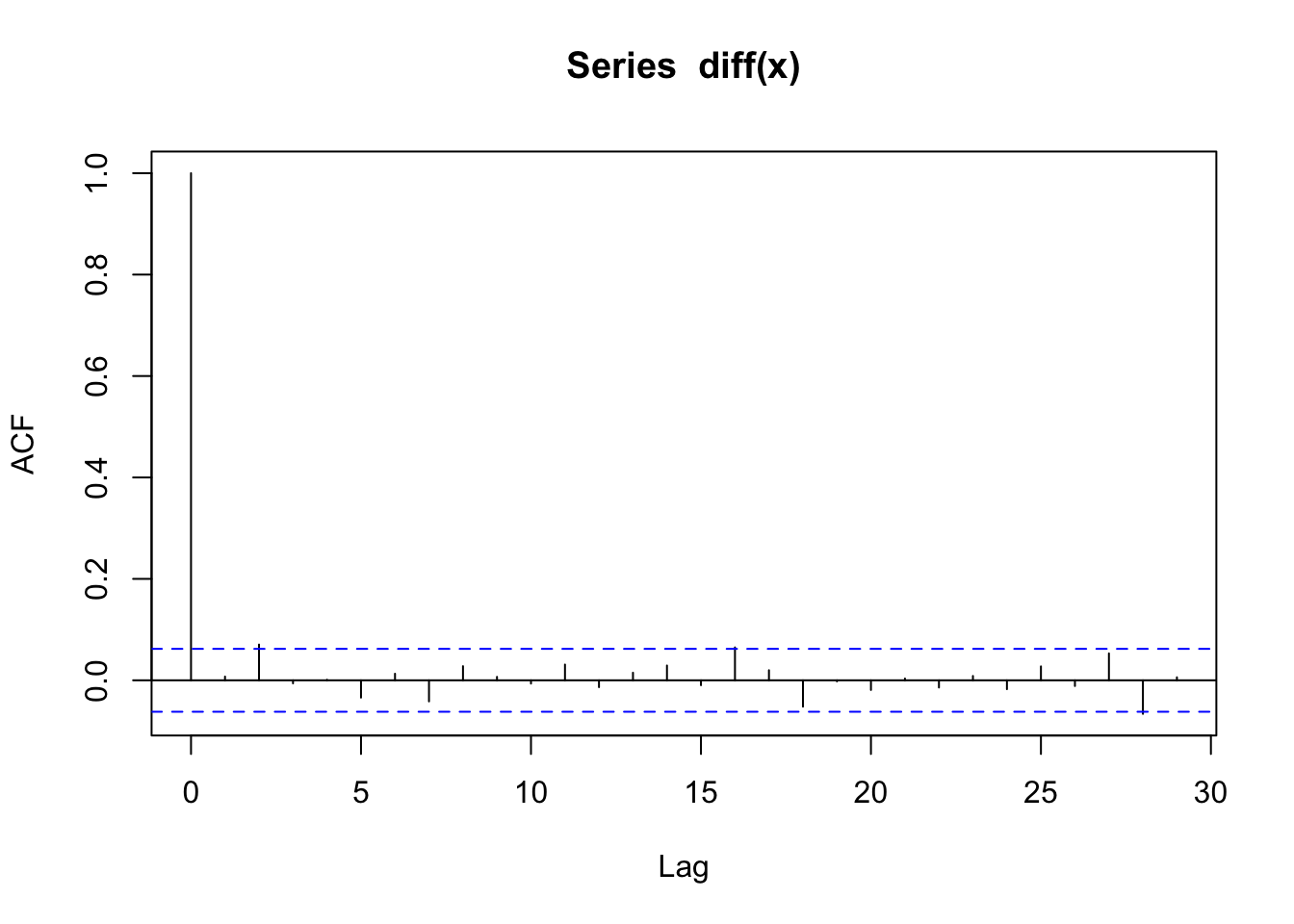

acf(diff(x))

Tidyverts code

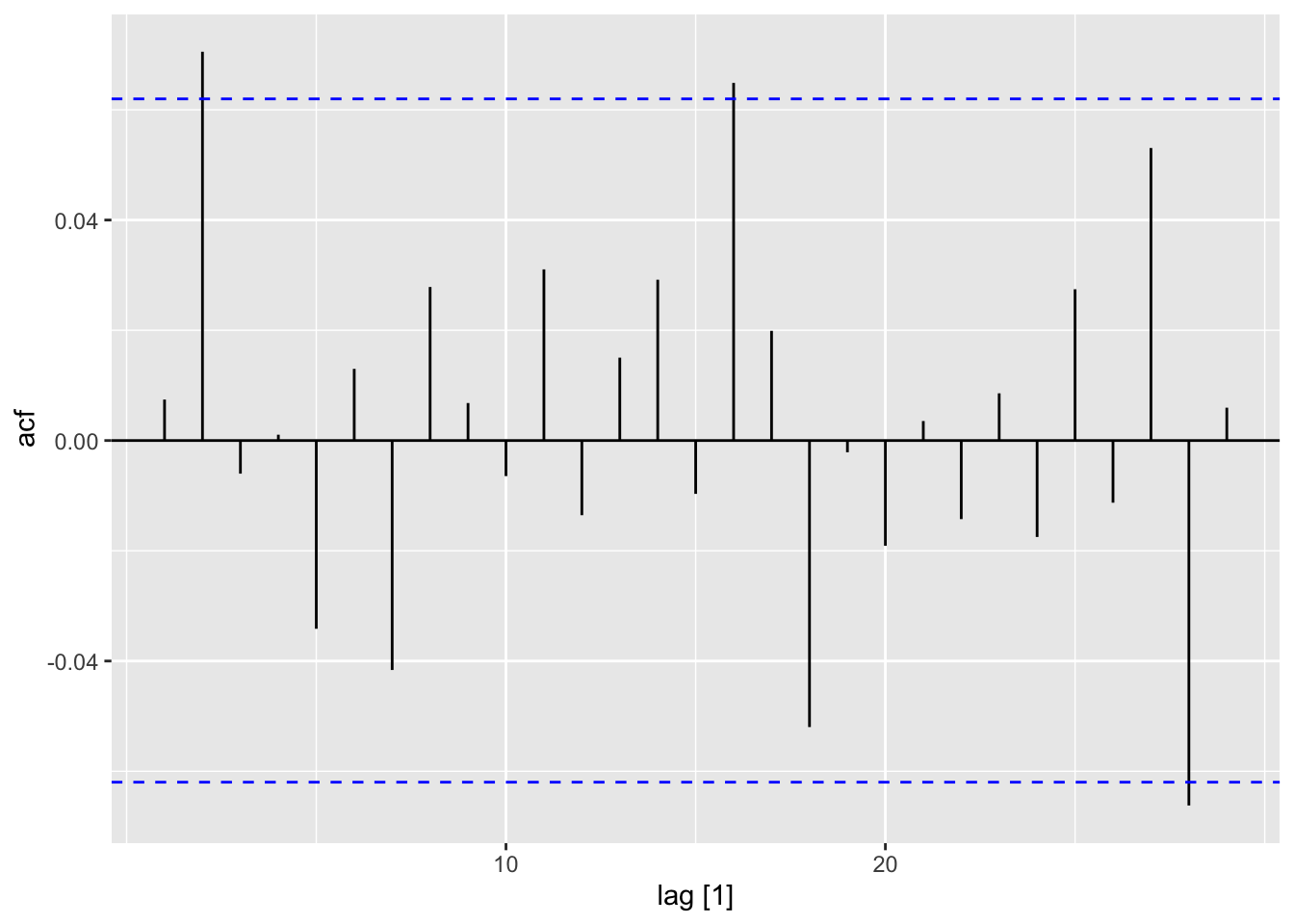

dat |>

mutate(diff = x - lag(x)) |>

ACF(diff) |>

autoplot()

Book code

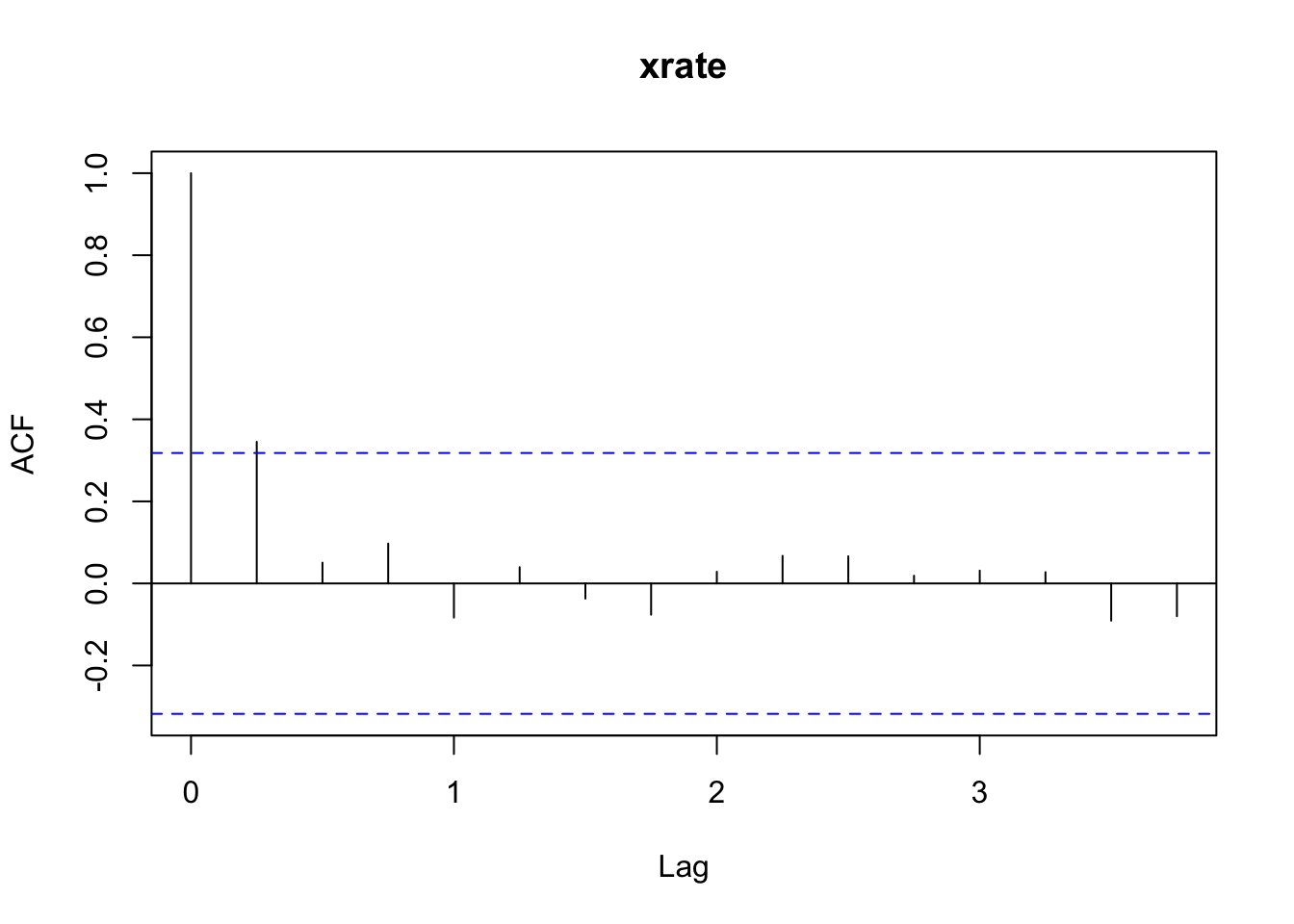

Z <- read.table("data/pounds_nz.dat", header = T)

Z.ts <- ts(Z, st = 1991, fr = 4)

acf(diff(Z.ts))

Tidyverts code

z <- read_table("data/pounds_nz.dat")

date_seq <- seq(

lubridate::ymd("1991-01-01"),

by = "3 months",

length.out = nrow(z))

z_ts <- z |>

mutate(

date = date_seq,

quarter = tsibble::yearquarter(date)) |>

as_tsibble(index = quarter)

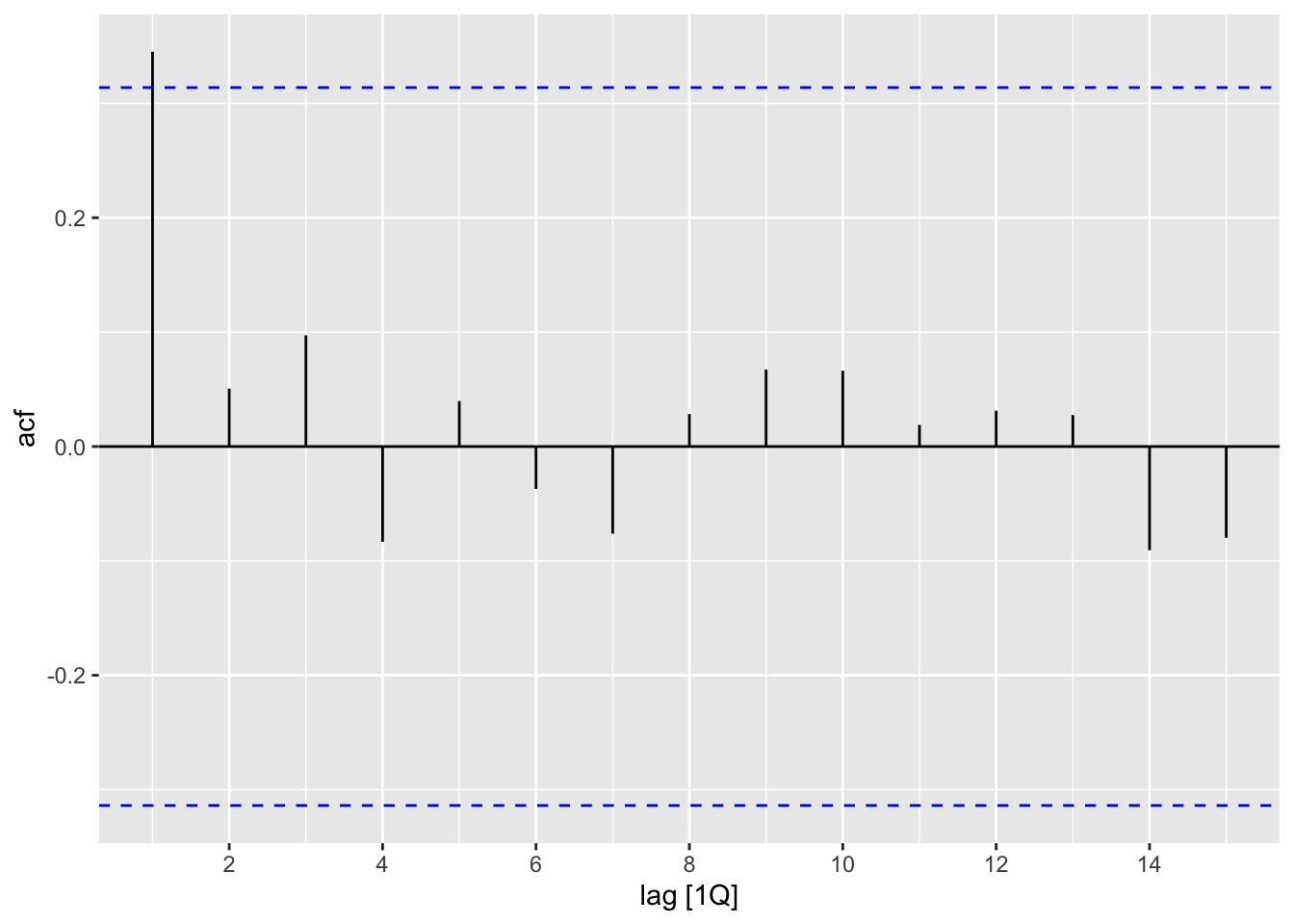

z_ts |>

mutate(diff = xrate - lag(xrate)) |>

ACF(diff) |>

autoplot()

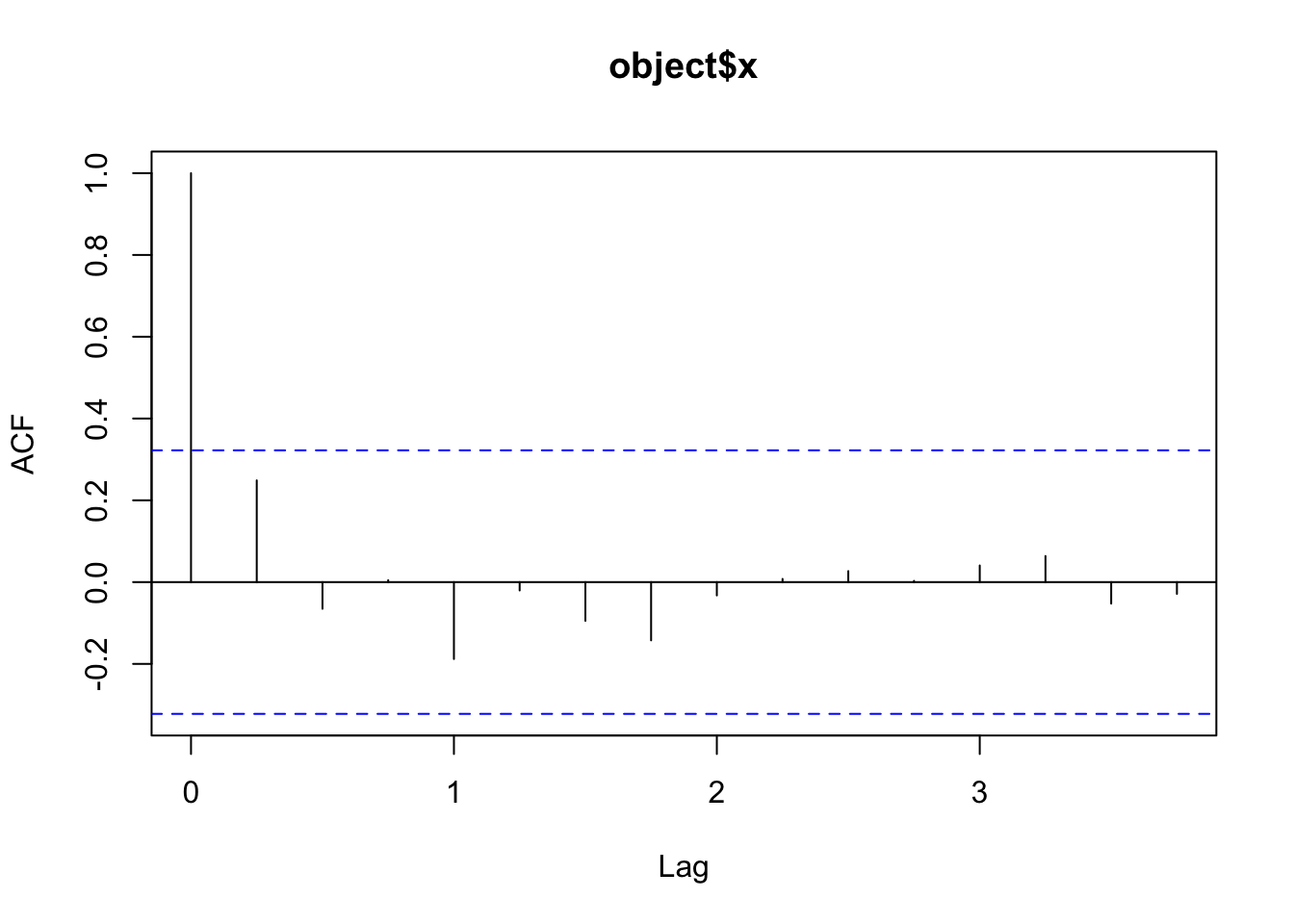

Z.hw <- HoltWinters(Z.ts, alpha = 1, gamma = FALSE) # changed from book

acf(resid(Z.hw)) # not exact match.

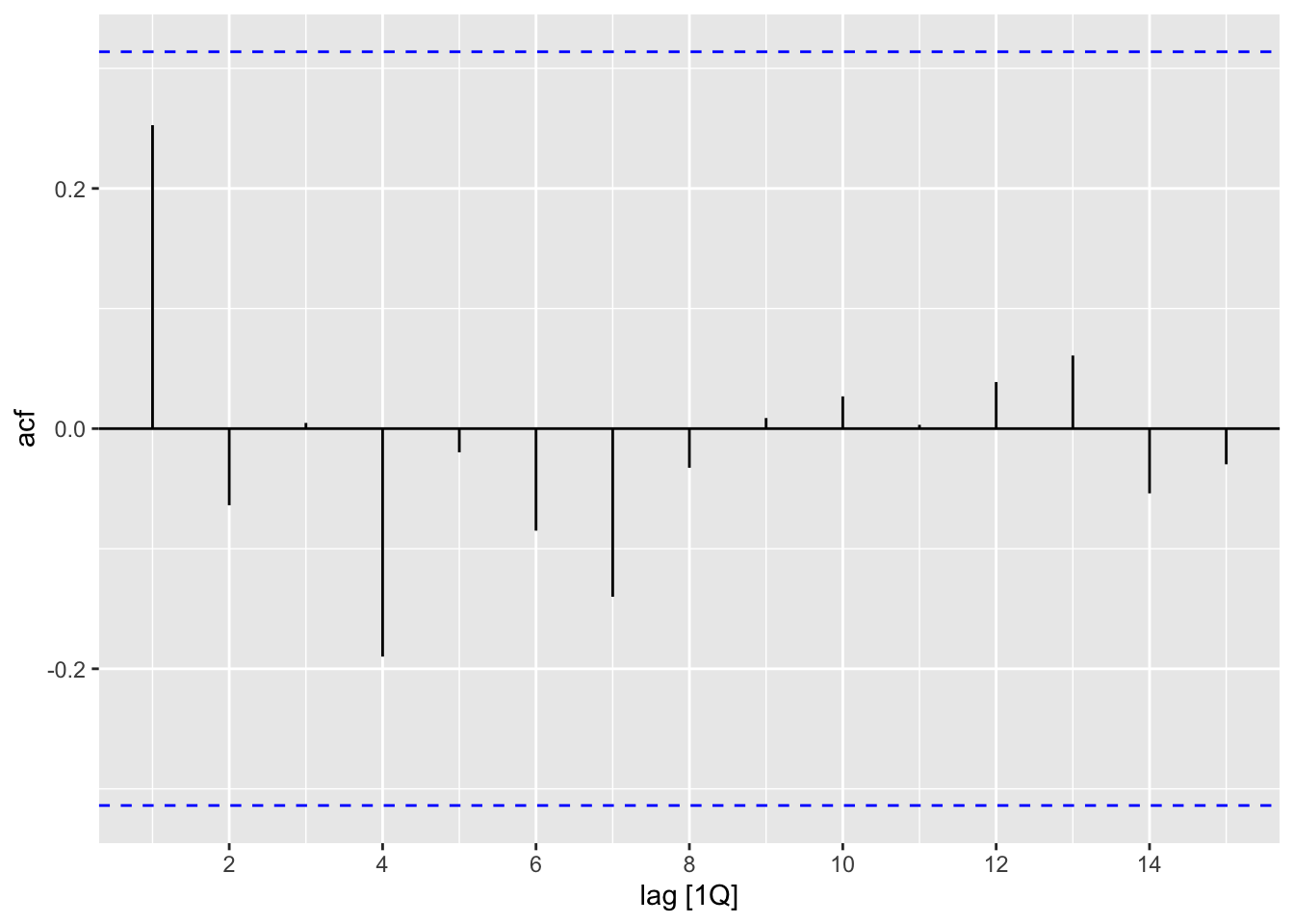

z_hw <- z_ts |>

model(Additive = ETS(xrate ~

trend("A", alpha = 1) +

error("A") + season("N", gamma = 0),

opt_crit = "amse", nmse = 1)) |>

residuals()

ACF(z_hw, .resid) |>

autoplot()

z <- read_table("data/pounds_nz.dat")

date_seq <- seq(

lubridate::ymd("1991-01-01"),

by = "3 months",

length.out = nrow(z))

z_ts <- z |>

mutate(

date = date_seq,

quarter = tsibble::yearquarter(date)) |>

as_tsibble(index = quarter)

z_ts |>

mutate(diff = xrate - lag(xrate)) |>

ACF(diff) |>

autoplot()

z_hw <- z_ts |>

model(Additive = ETS(xrate ~

trend("A", alpha = 1) +

error("A") + season("N", gamma = 0),

opt_crit = "amse", nmse = 1)) |>

residuals()

ACF(z_hw, .resid) |>

autoplot()Book code

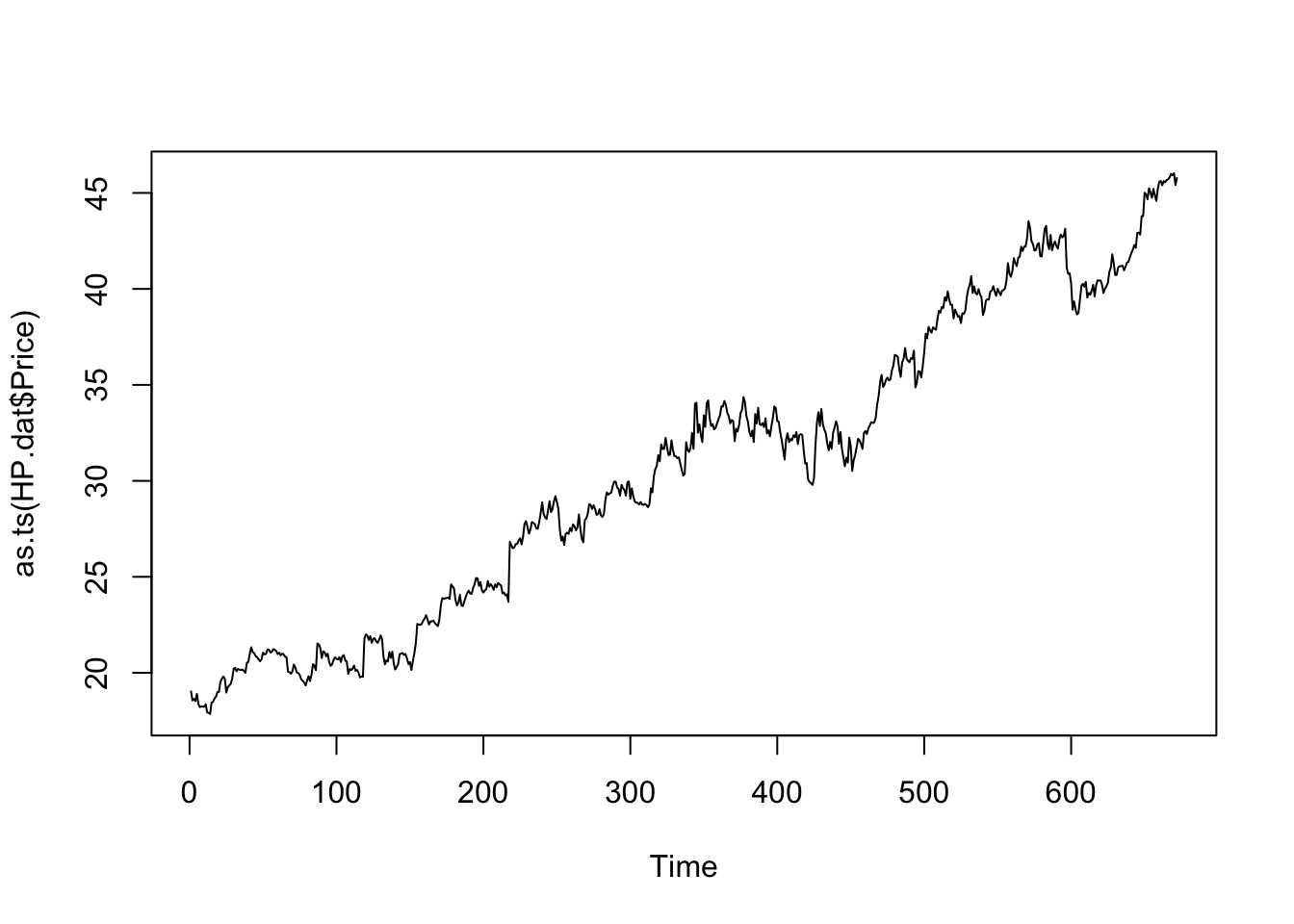

HP.dat <- read.table("data/HP.txt", header = T)

# attach(HP.dat) # bad practice

plot(as.ts(HP.dat$Price))

Tidyverts code

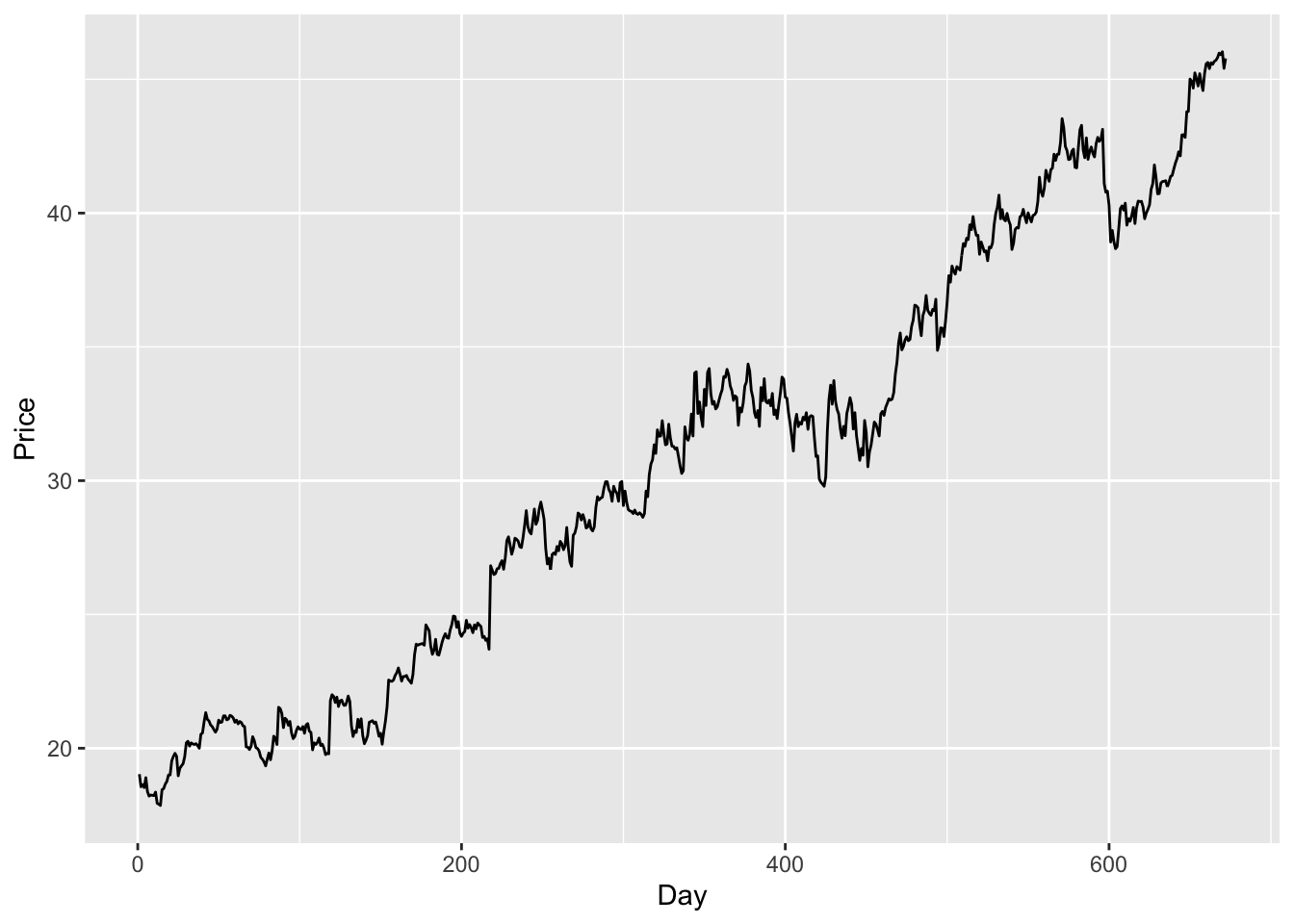

hp_dat <- read_table("data/HP.txt") |>

mutate(Day = 1:n())

ggplot(hp_dat, aes(x = Day, y = Price)) + geom_line()

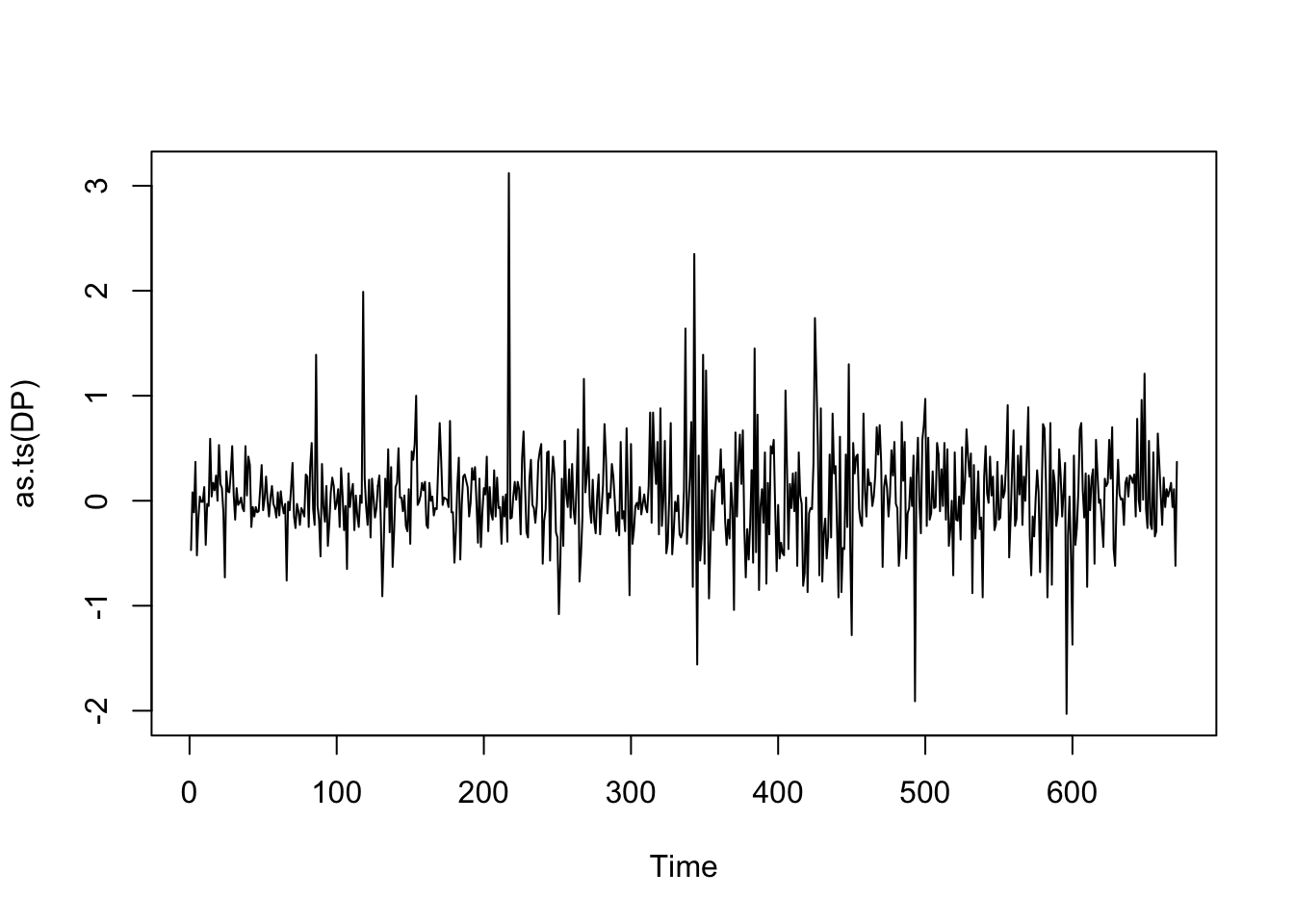

DP <- diff(HP.dat$Price)

plot(as.ts(DP))

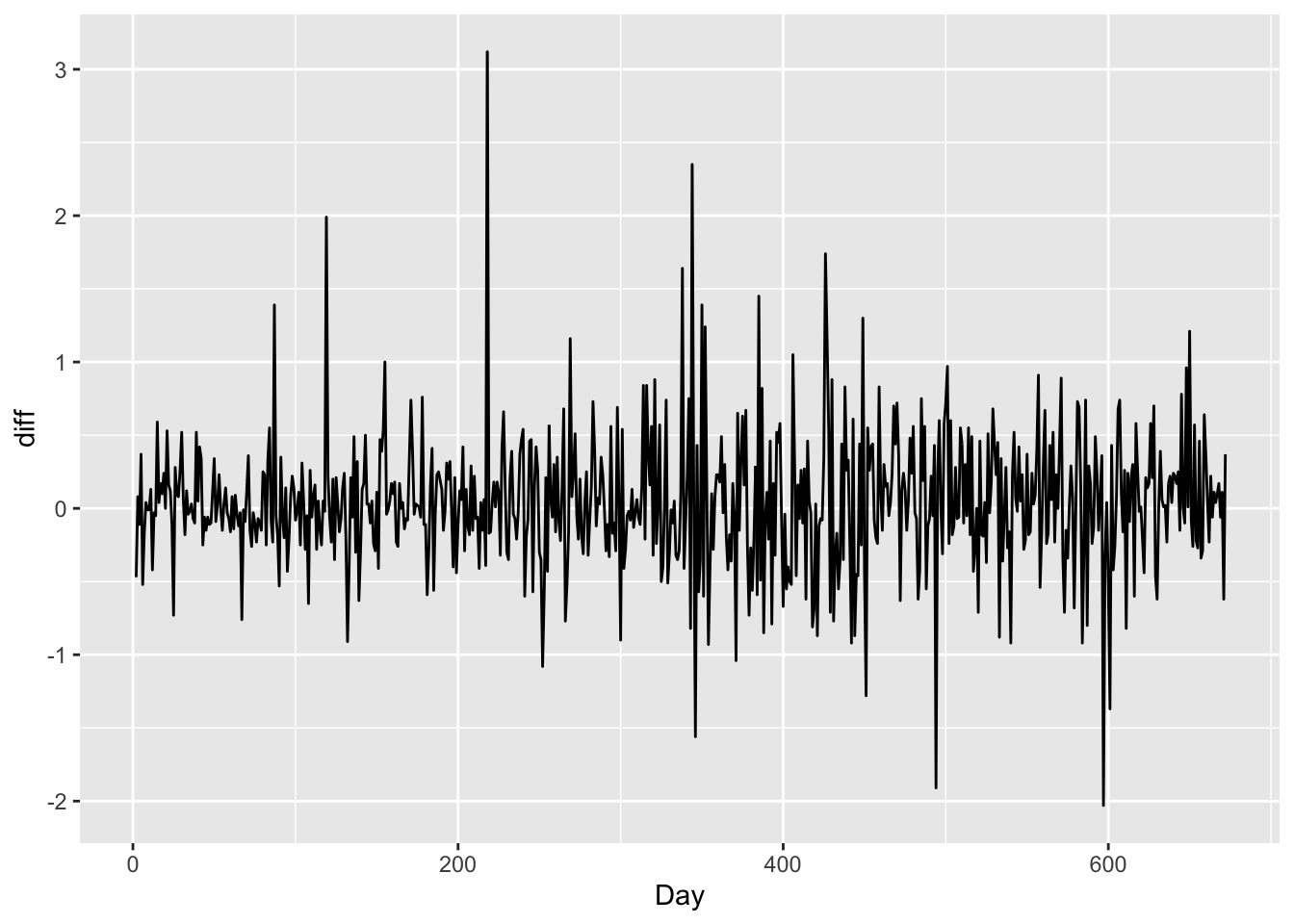

hp_dat |>

mutate(diff = Price - lag(Price)) |>

ggplot(aes(x = Day, y = diff)) +

geom_line()

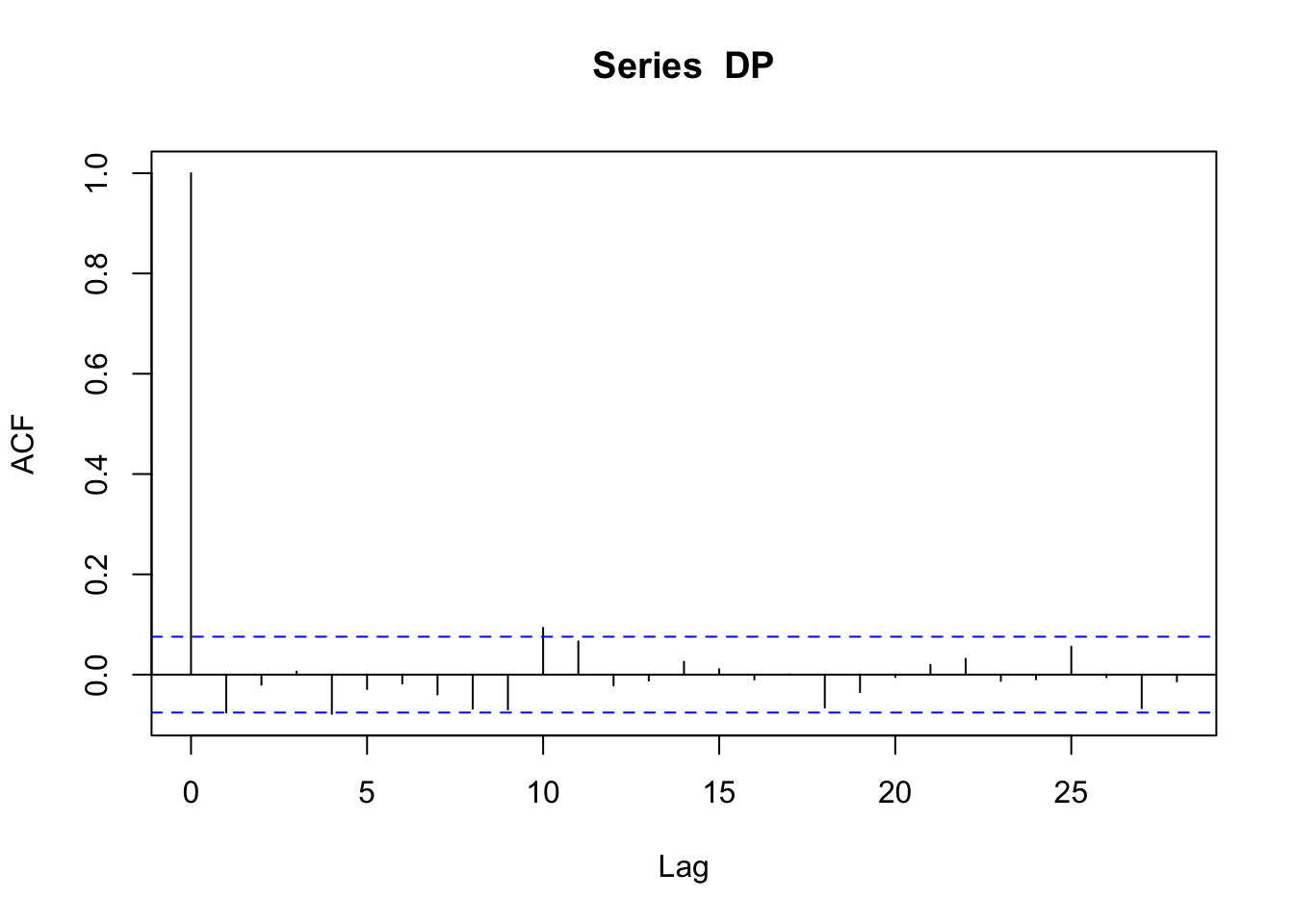

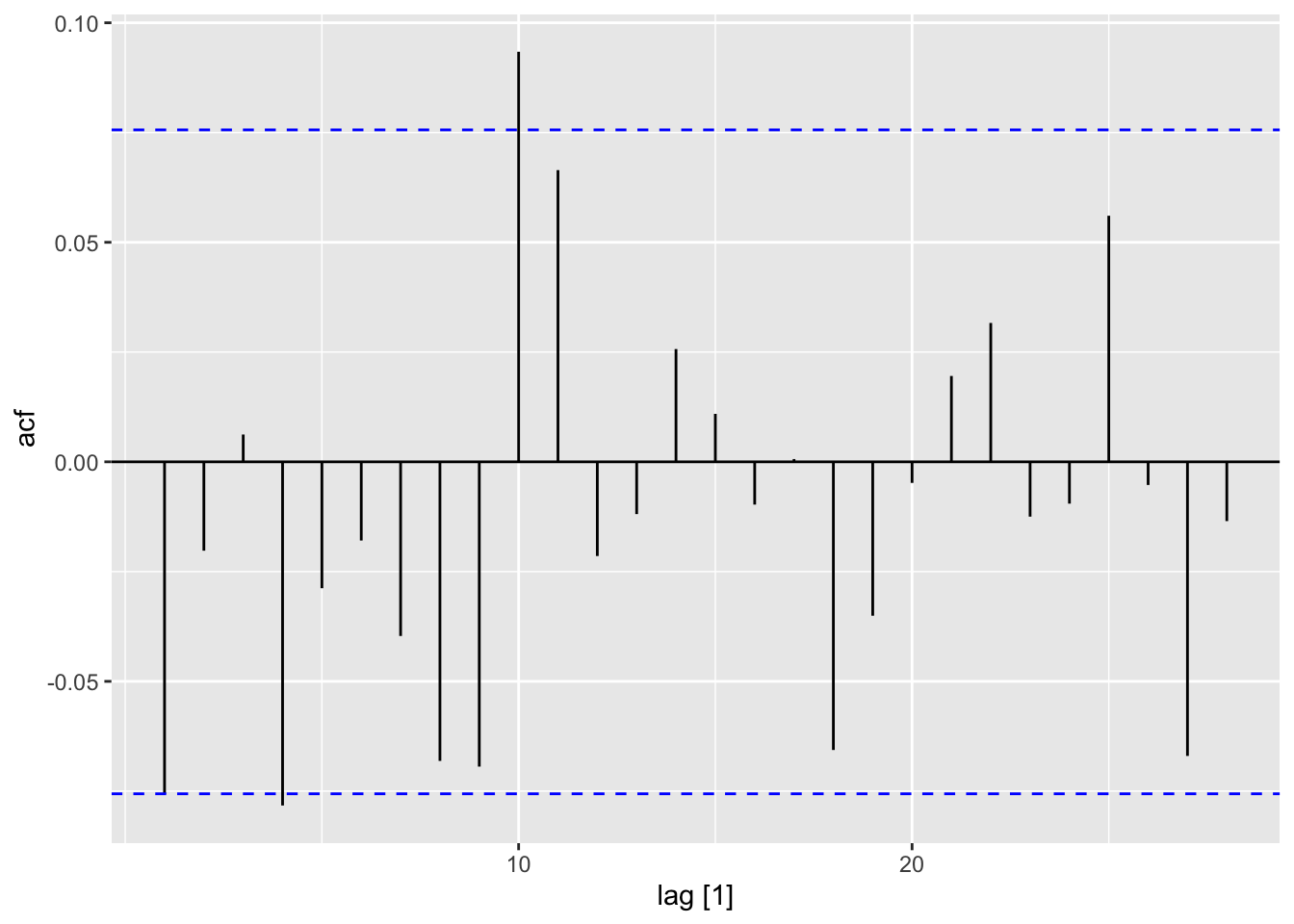

acf(DP)

hp_dat |>

mutate(diff = Price - lag(Price)) |>

as_tsibble(index = Day) |>

ACF(diff) |>

autoplot()

mean(DP) + c(-2, 2) * sd(DP) / sqrt(length(DP))[1] 0.004378275 0.075353468hp_dat |>

mutate(diff = Price - lag(Price)) |>

slice(-1) |>

summarize(

mean = mean(diff),

sd = sd(diff),

n = n(),

std_error = sd / sqrt(n),

lower = mean - 2 * std_error,

upper = mean + 2 * std_error)# A tibble: 1 × 6

mean sd n std_error lower upper

<dbl> <dbl> <int> <dbl> <dbl> <dbl>

1 0.0399 0.460 671 0.0177 0.00438 0.0754hp_dat <- read_table("data/HP.txt") |>

mutate(Day = 1:n())

ggplot(hp_dat, aes(x = Day, y = Price))

geom_line()

hp_dat |>

mutate(diff = Price - lag(Price)) |>

ggplot(aes(x = Day, y = diff)) +

geom_line()

hp_dat |>

mutate(diff = Price - lag(Price)) |>

as_tsibble(index = Day) |>

ACF(diff) |>

autoplot()

hp_dat |>

mutate(diff = Price - lag(Price)) |>

slice(-1) |>

summarize(

mean = mean(diff),

sd = sd(diff),

n = n(),

std_error = sd / sqrt(n),

lower = mean - 2 * std_error,

upper = mean + 2 * std_error)Book code

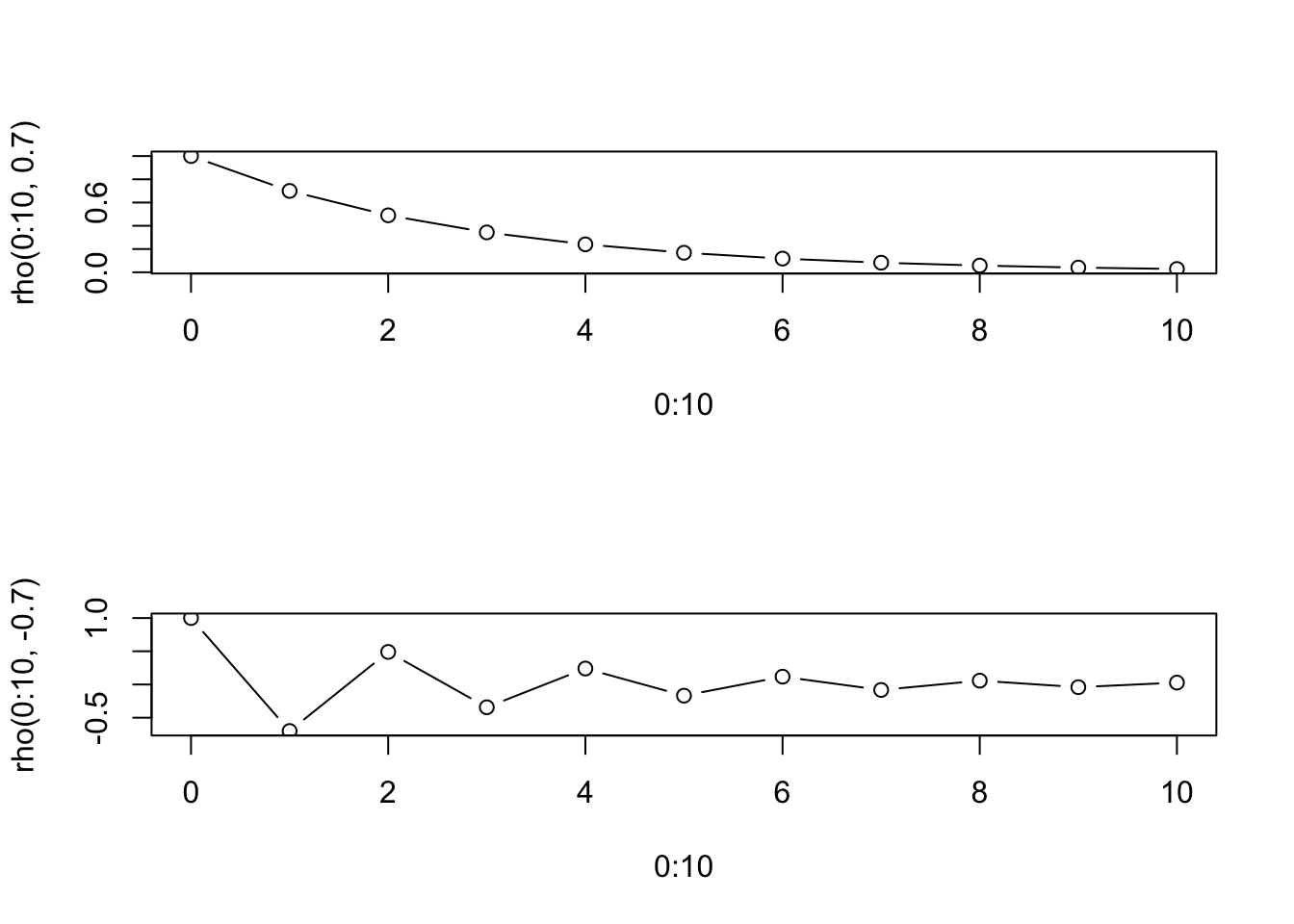

rho <- function(k, alpha) alpha^k

layout(1:2)

plot(0:10, rho(0:10, 0.7), type = "b")

plot(0:10, rho(0:10, -0.7), type = "b")

Tidyverts code

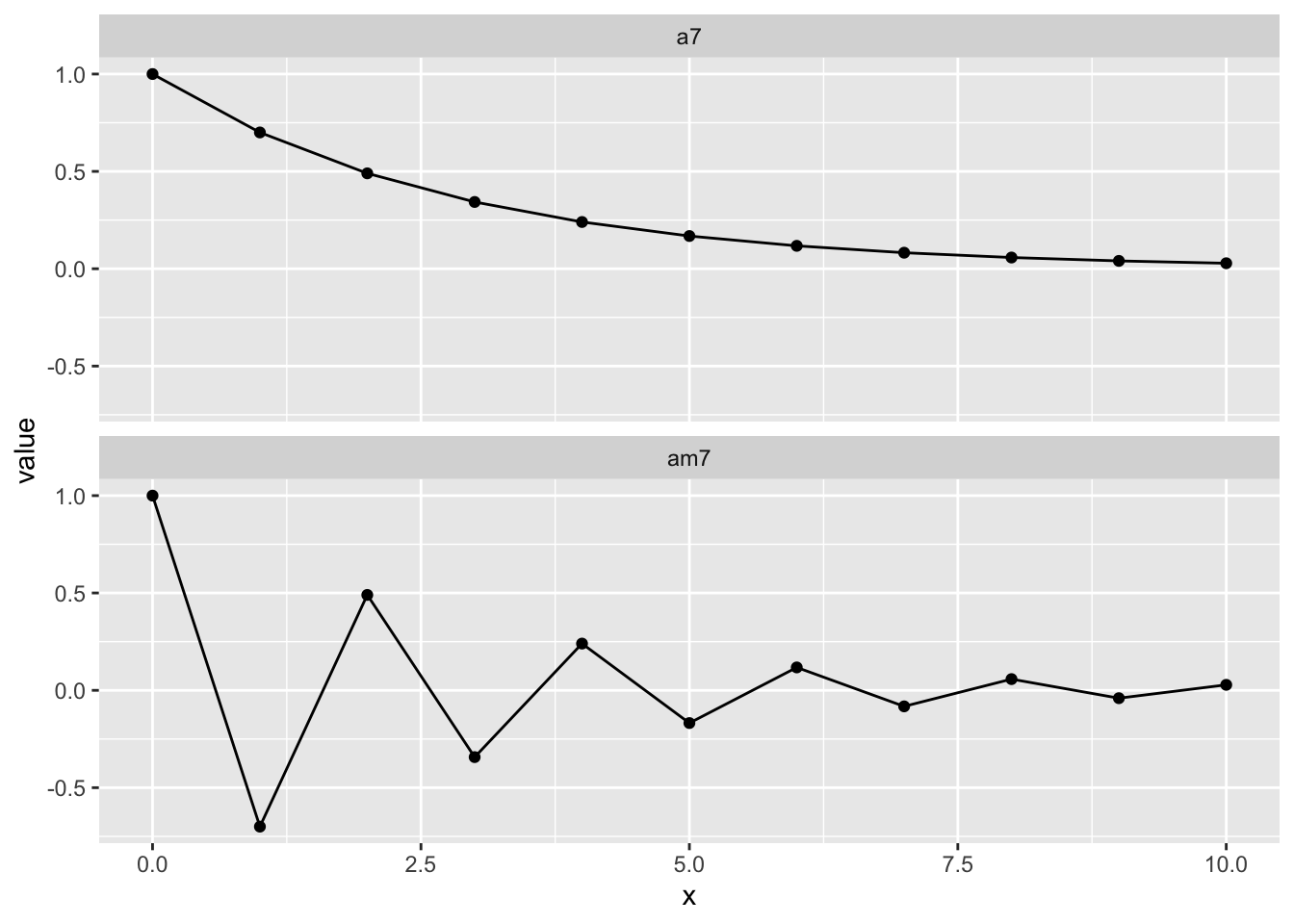

rho <- function(k, alpha) alpha^k

dat <- tibble(

x = 0:10,

a7 = rho(x, .7),

am7 = rho(x, -.7)) |>

pivot_longer(a7:am7,

names_to = "param",

values_to = "value")

ggplot(dat, aes(x = x, y = value)) +

geom_line() +

geom_point() +

facet_wrap(~param, ncol = 1)

set.seed(1)

x <- w <- rnorm(100)

for (t in 2:100) x[t] <- 0.7 * x[t - 1] + w[t]

plot(x, type = "l")

set.seed(1)

dat <- tibble(w = rnorm(100)) |>

mutate(

index = 1:n(),

x = purrr::accumulate2(

lag(w), w,

\(acc, nxt, w) 0.7 * acc + w,

.init = 0)[-1]) |>

tsibble::as_tsibble(index = index)

autoplot(dat, .var = x)

acf(x)

ACF(dat, x) |>

autoplot()

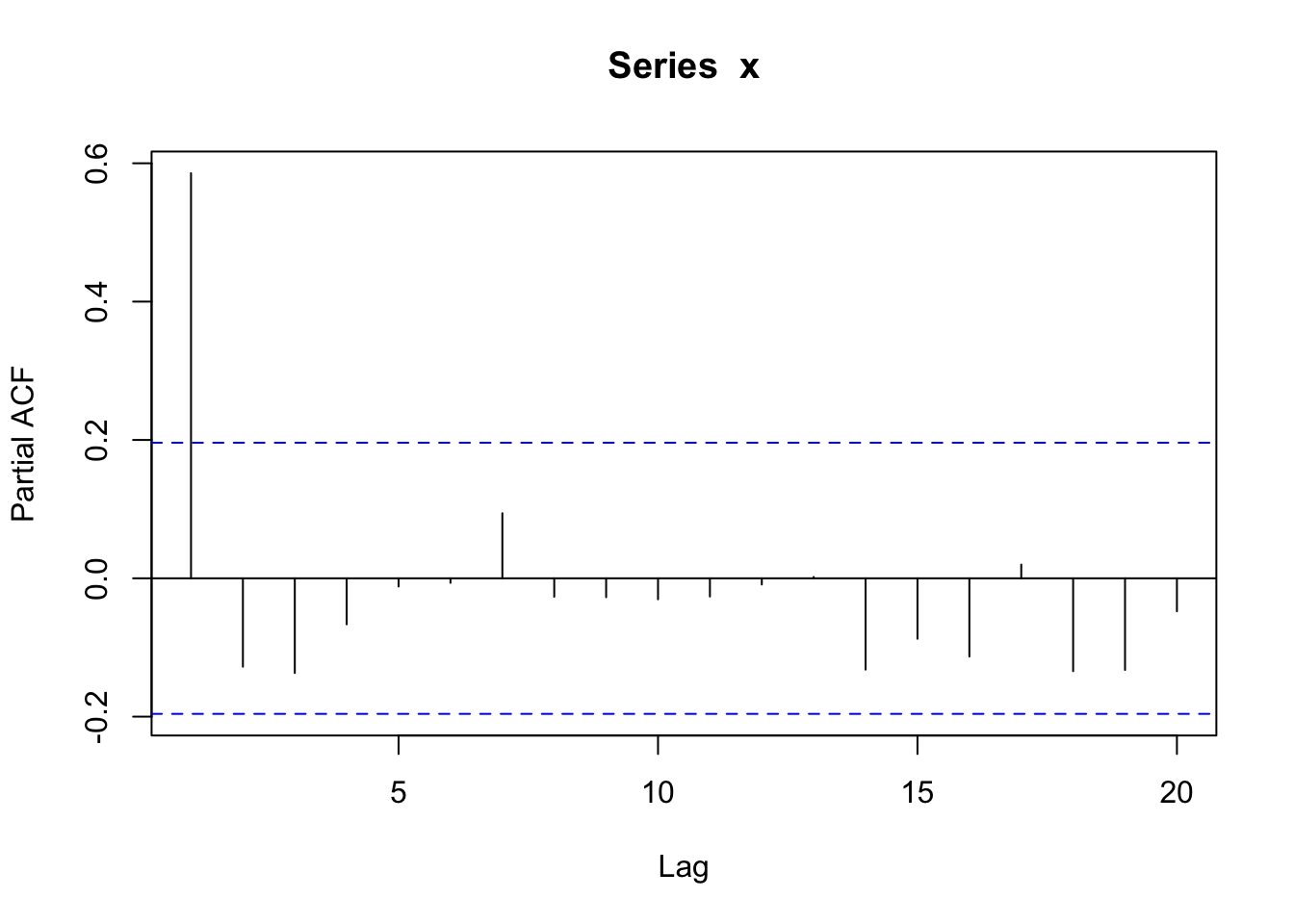

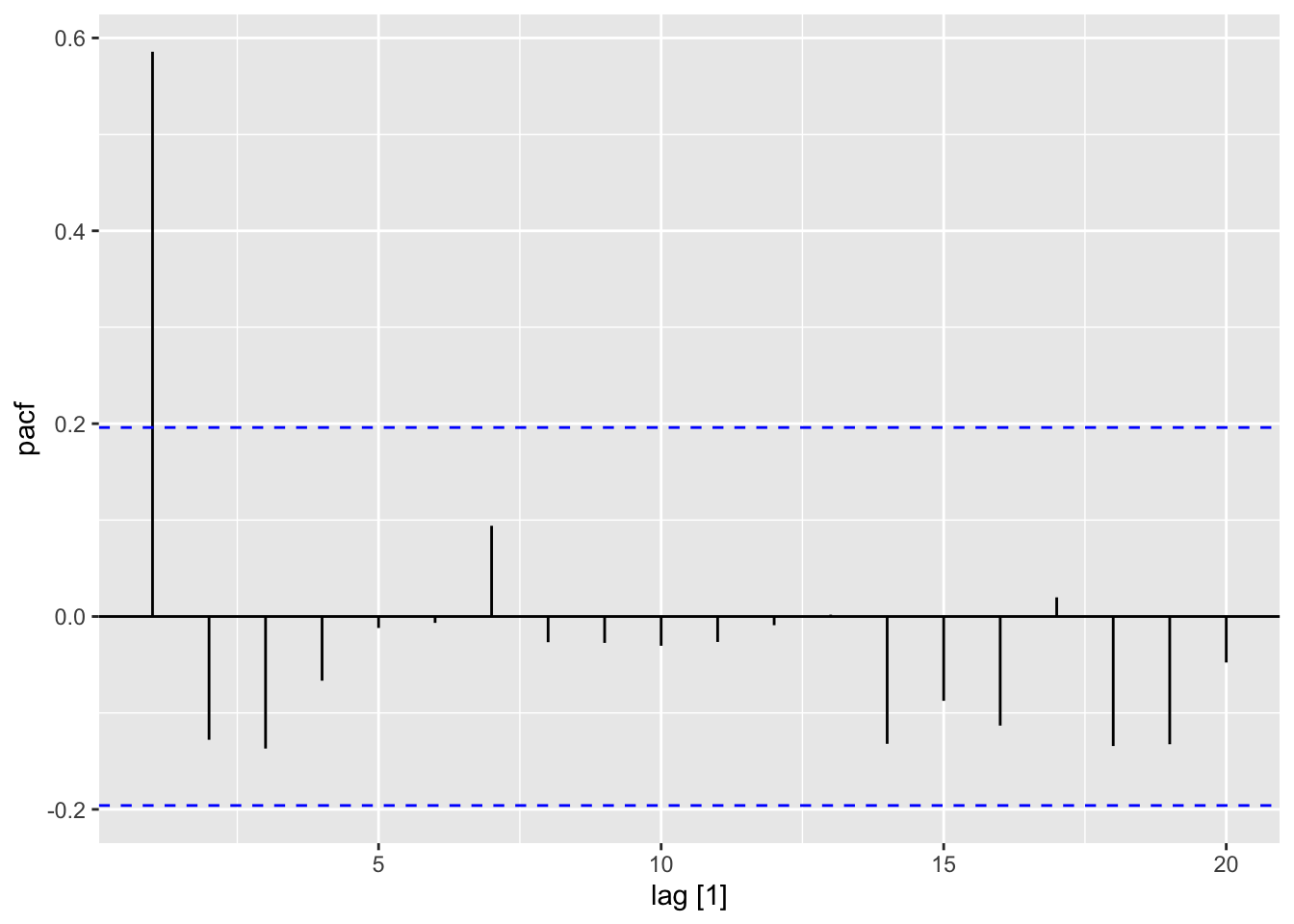

pacf(x)

PACF(dat, x) |>

autoplot()

The stats::ar() and fable::AR() appear to have different optimization routines. For example, the fable::AR() model only allows optimization using Ordinary Least Squares (OLS), and stats::ar() provides multiple options. The textbook uses method = "mle" in these examples. Other differences are also apparent. As such, the results in the remaining sections do not match exactly.

Book code

set.seed(1)

x <- w <- rnorm(100)

for (t in 2:100) x[t] <- 0.7 * x[t - 1] + w[t]

x.ar <- ar(x, method = "mle")

x.ar$order[1] 1Tidyverts code

set.seed(1)

dat <- tibble(w = rnorm(100)) |>

mutate(

index = 1:n(),

x = purrr::accumulate2(

lag(w), w,

\(acc, nxt, w) 0.7 * acc + w,

.init = 0)[-1]) |>

tsibble::as_tsibble(index = index)

# Note that mle is not available using ols in ARMA

# answers slightly different

fit_ar <- dat |>

model(AR(x ~ order(1)))

print("Order defined as 1 using order")[1] "Order defined as 1 using order"x.ar$ar[1] 0.6009459tidy(fit_ar) |>

filter(str_detect(term, "ar")) |>

pull("estimate")[1] 0.6015796x.ar$ar + c(-2, 2) * sqrt(x.ar$asy.var)[1] # slight change[1] 0.4404031 0.7614886tidy(fit_ar) |>

mutate(

lb = estimate - 2 * std.error,

ub = estimate + 2 * std.error

)# A tibble: 2 × 8

.model term estimate std.error statistic p.value lb ub

<chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 AR(x ~ order(1)) constant 0.157 0.0955 1.65 1.03e- 1 -0.0339 0.348

2 AR(x ~ order(1)) ar1 0.602 0.0814 7.39 5.03e-11 0.439 0.764set.seed(1)

dat <- tibble(w = rnorm(100)) |>

mutate(

index = 1:n(),

x = purrr::accumulate2(

lag(w), w,

\(acc, nxt, w) 0.7 * acc + w,

.init = 0)[-1]) |>

tsibble::as_tsibble(index = index)

# Note that mle is not available using ols in ARMA

# answers slightly different

fit_ar <- dat |>

model(AR(x ~ order(1)))

tidy(fit_ar) |>

filter(str_detect(term, "ar")) |>

pull("estimate")

tidy(fit_ar) |>

mutate(

lb = estimate - 2 * std.error,

ub = estimate + 2 * std.error

)See note about stats::ar() and fable::AR() in previous section.

Book code

Z <- read.table("data/pounds_nz.dat", header = T)

Z.ts <- ts(Z, st = 1991, fr = 4)

Z.ar <- ar(Z.ts)

mean(Z.ts)[1] 2.823251Tidyverts code

z <- read_table("data/pounds_nz.dat")

date_seq <- seq(

lubridate::ymd("1991-01-01"),

by = "3 months",

length.out = nrow(z))

z_ts <- z |>

mutate(

date = date_seq,

quarter = tsibble::yearquarter(date)) |>

as_tsibble(index = quarter)

z_ar <- z_ts |>

model(AR(xrate ~ order(1)))

mean(z_ts$xrate)[1] 2.823251c(Z.ar$order, Z.ar$ar)[1] 1.000000 0.890261tidy(z_ar) |>

filter(str_detect(term, "ar")) |>

pull("estimate")[1] 1.005271Z.ar$ar + c(-2, 2) * sqrt(Z.ar$asy.var)[1][1] 0.7405097 1.0400123tidy(z_ar) |>

mutate(

lb = estimate - 2 * std.error,

ub = estimate + 2 * std.error

)# A tibble: 1 × 8

.model term estimate std.error statistic p.value lb ub

<chr> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

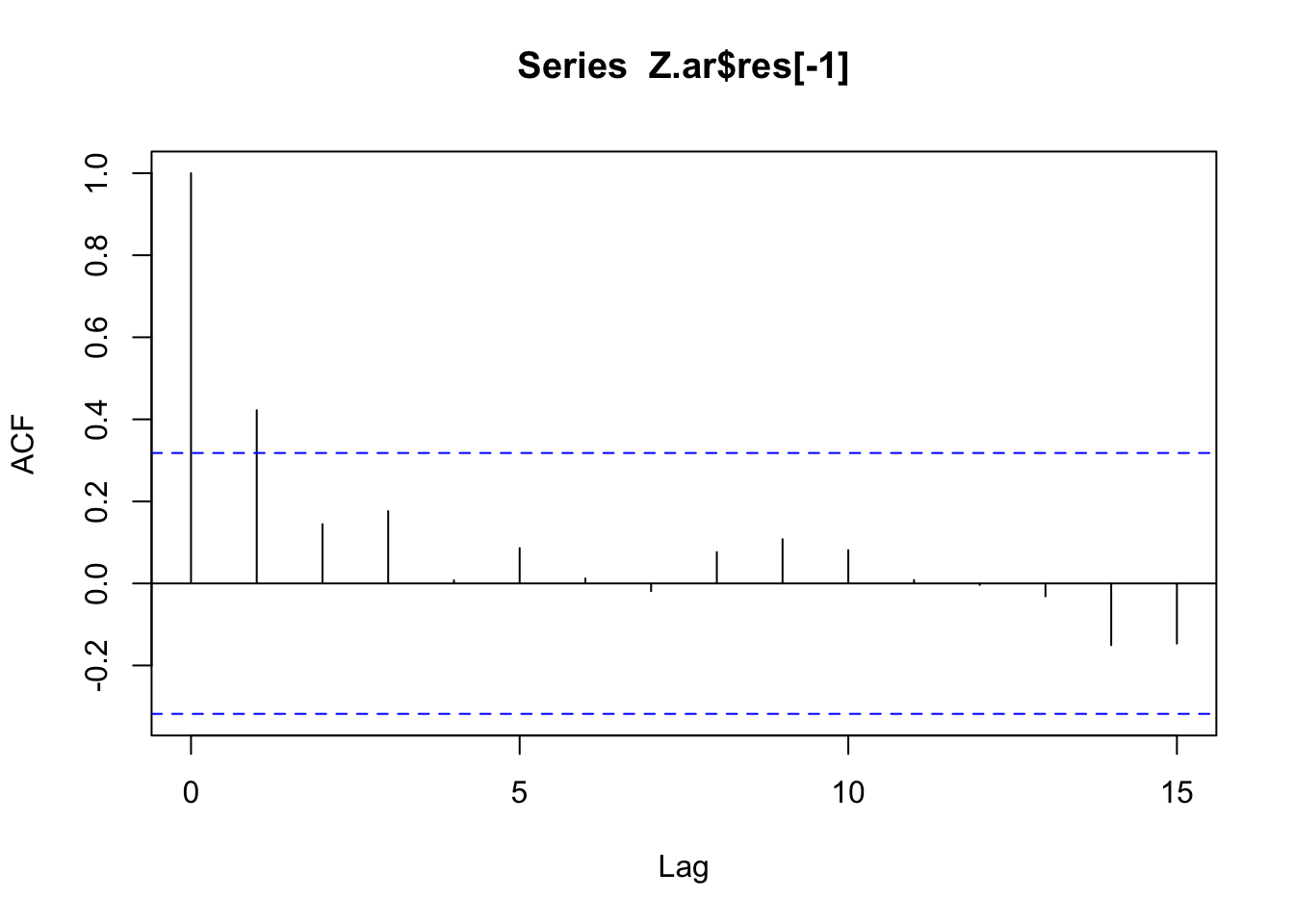

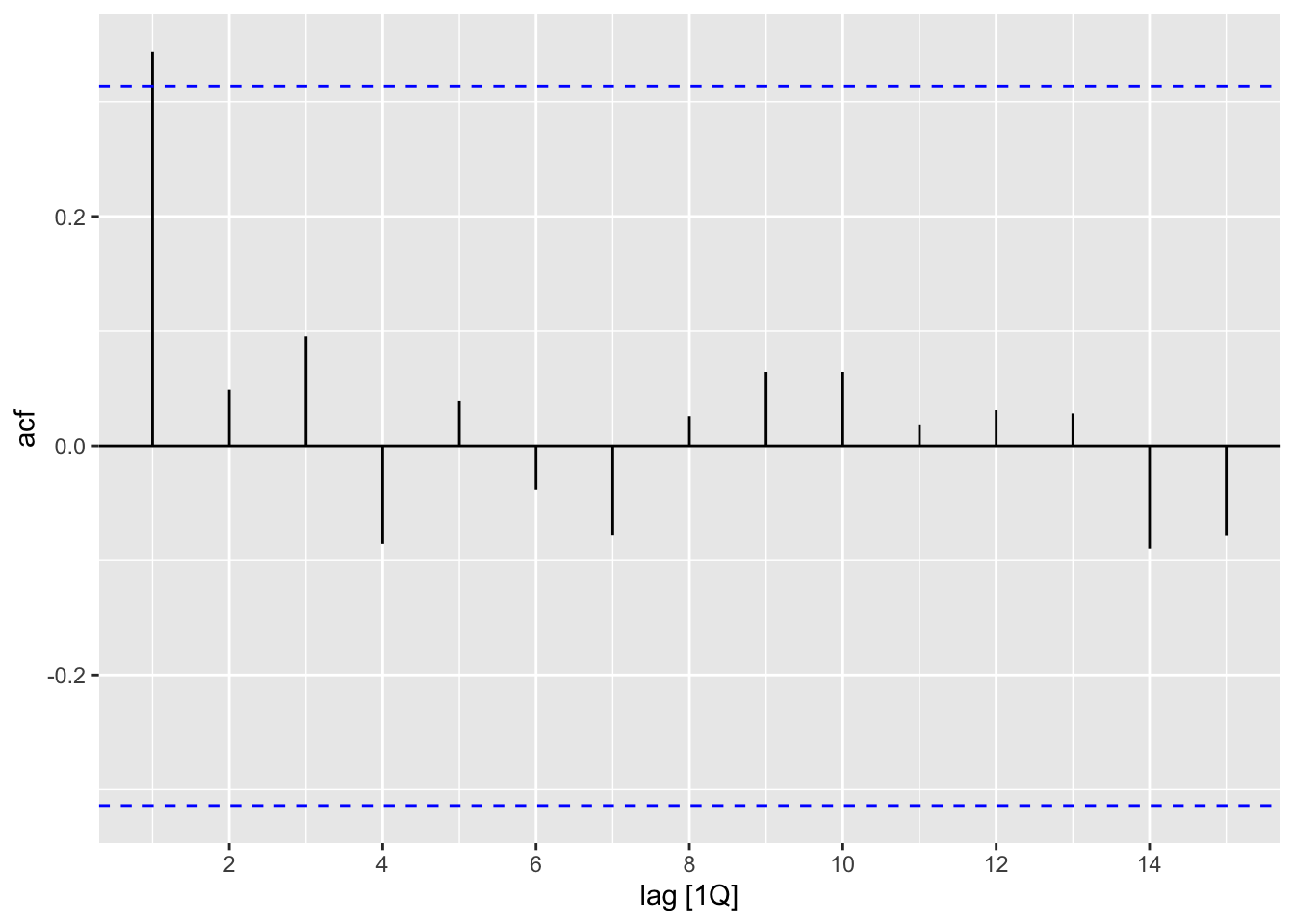

1 AR(xrate ~ order(1)) ar1 1.01 0.00781 129. 8.55e-52 0.990 1.02acf(Z.ar$res[-1])

residuals(z_ar) |> ACF(y = .resid) |> autoplot()

z <- read_table("data/pounds_nz.dat")

date_seq <- seq(

lubridate::ymd("1991-01-01"),

by = "3 months",

length.out = nrow(z))

z_ts <- z |>

mutate(

date = date_seq,

quarter = tsibble::yearquarter(date)) |>

as_tsibble(index = quarter)

z_ar <- z_ts |>

model(AR(xrate ~ order(1)))

mean(z_ts$xrate)

tidy(z_ar) |>

filter(str_detect(term, "ar")) |>

pull("estimate")

tidy(z_ar) |>

mutate(

lb = estimate - 2 * std.error,

ub = estimate + 2 * std.error

)

residuals(z_ar) |> ACF(y = .resid) |> autoplot()See note about stats::ar() and fable::AR() in previous section.

Book code

Global = scan("data/global.dat")

Global.ts = ts(Global, st = c(1856, 1), end = c(2005, 12),fr = 12)

Global.ar <- ar(aggregate(Global.ts, FUN = mean), method = "mle")

mean(aggregate(Global.ts, FUN = mean))[1] -0.1382628Tidyverts code

global <- tibble(x = scan("data/global.dat")) |>

mutate(

date = seq(

ymd("1856-01-01"),

by = "1 months",

length.out = n()),

year = year(date),

year_month = tsibble::yearmonth(date))

global_ts <- global |>

as_tsibble(index = year_month)

global_ts_year <- global |>

summarise(x = mean(x), .by = year) |>

as_tsibble(index = year)

global_ar <- global_ts_year |>

model(AR(x ~ order(1:9)))

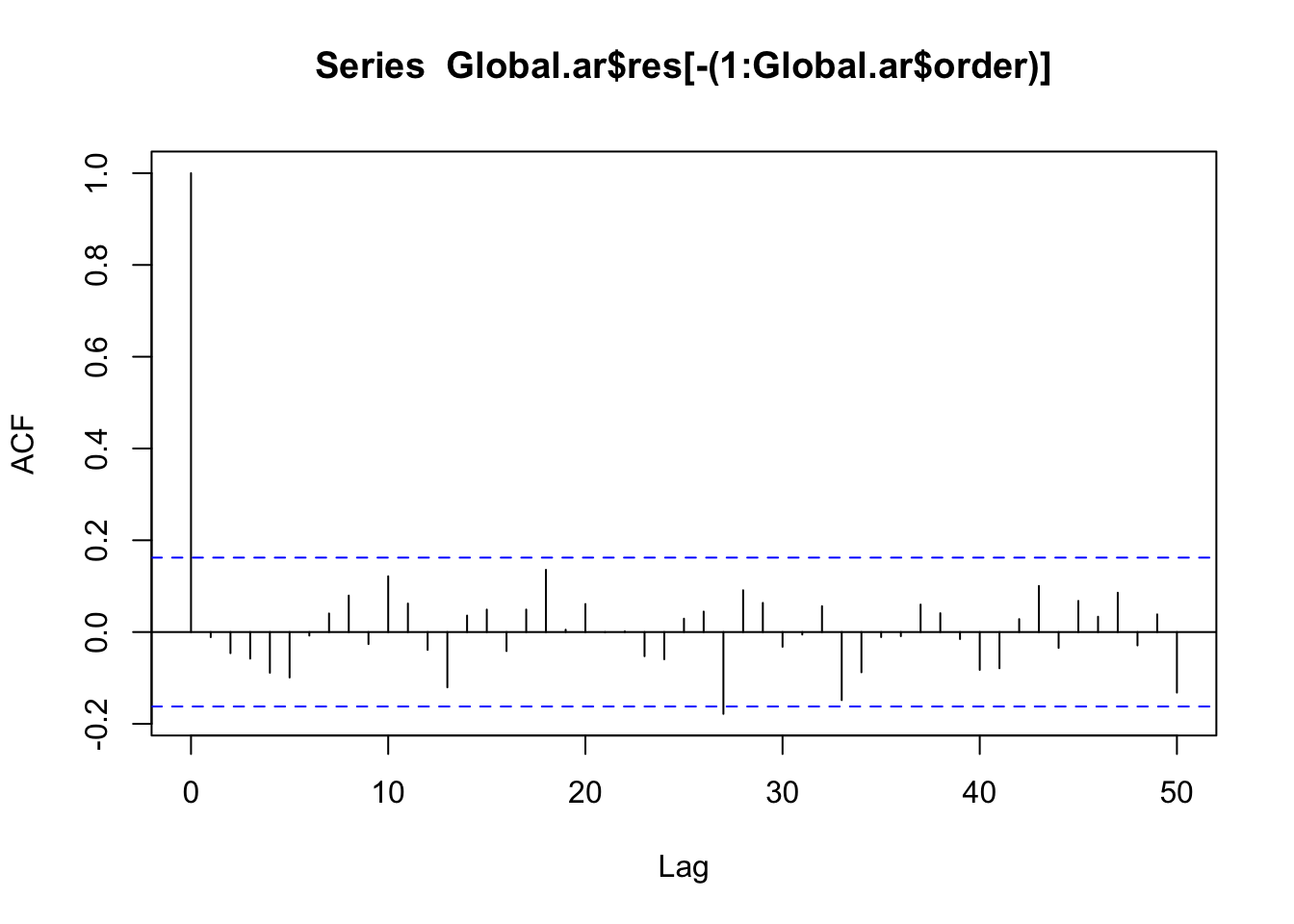

mean(global_ts$x)[1] -0.1382628Global.ar$order[1] 4tidy(global_ar) |> filter(str_detect(term, "ar")) |> nrow()[1] 4Global.ar$ar[1] 0.58762026 0.01260252 0.11116731 0.26763656tidy(global_ar) |> filter(str_detect(term, "ar")) |> pull(estimate)[1] 0.58176066 0.02164876 0.10747306 0.26707158acf(Global.ar$res[-(1:Global.ar$order)], lag = 50)

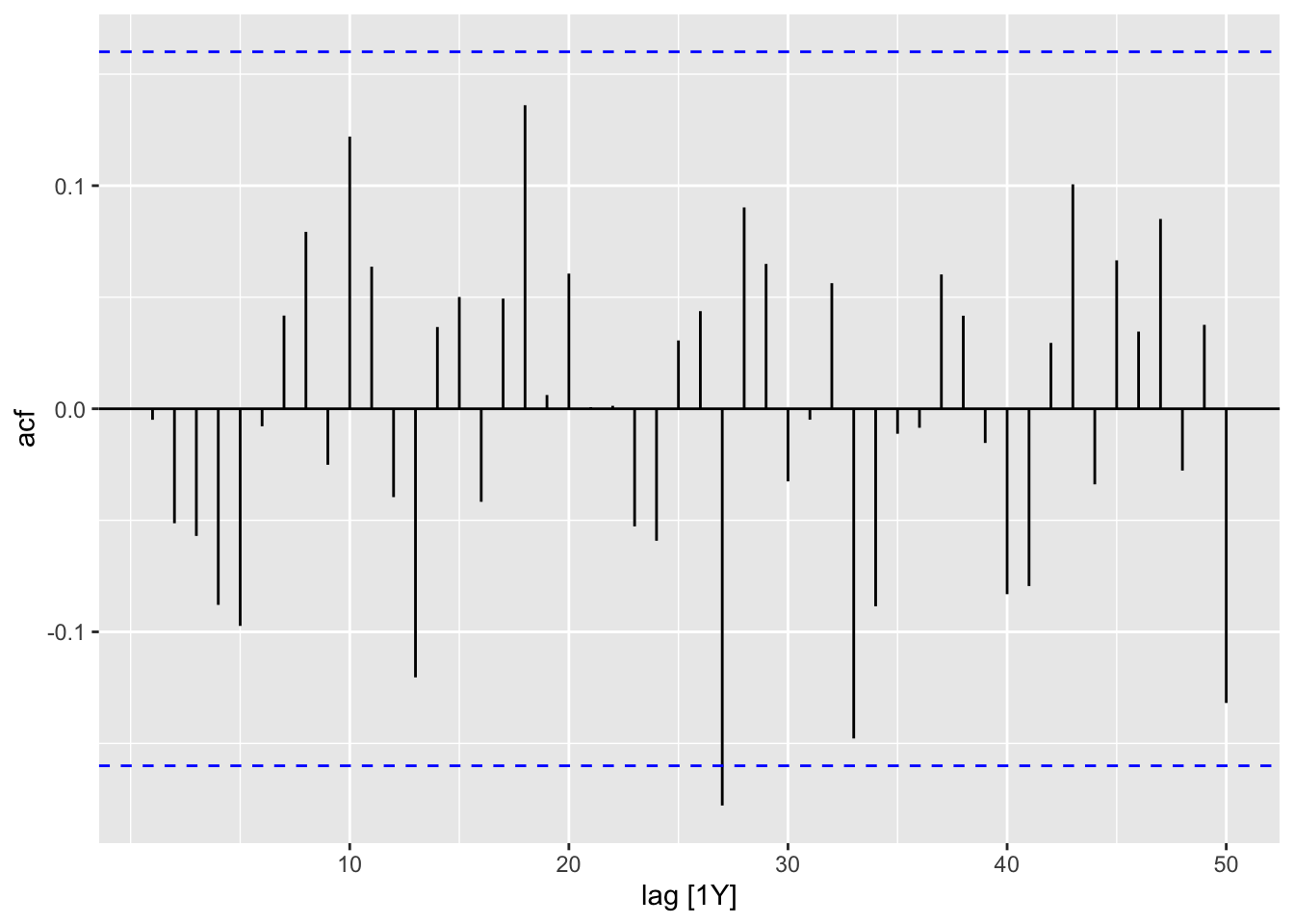

residuals(global_ar) |> ACF(lag_max = 50) |> autoplot()

global <- tibble(x = scan("data/global.dat")) |>

mutate(

date = seq(

ymd("1856-01-01"),

by = "1 months",

length.out = n()),

year = year(date),

year_month = tsibble::yearmonth(date))

global_ts <- global |>

as_tsibble(index = year_month)

global_ts_year <- global |>

summarise(x = mean(x), .by = year) |>

as_tsibble(index = year)

global_ar <- global_ts_year |>

model(AR(x ~ order(1:9)))

mean(global_ts$x)

tidy(global_ar) |> filter(str_detect(term, "ar")) |> nrow()

tidy(global_ar) |> filter(str_detect(term, "ar")) |> pull(estimate)

residuals(global_ar) |> ACF(lag_max = 50) |> autoplot()R commands used in examplesggplot2::geom_histogram(): Histograms and frequency polygonsggplot2::after_stat(): Control aesthetic evaluationdplyr::slice(): Subset rows using their positionsggplot2::facet_wrap(): Wrap a 1d ribbon of panels into 2dpurr::accumulate2(): Accumulate intermediate results of a vector reduction\():fable::AR(): Estimate a AR modelstats::residuals(): Extract Model Residuals