Businesses rely on forecasts of sales to plan production, justify marketing decisions, and guide research. A very efficient method of forecasting one variable is to find a related variable that leads it by one or more time intervals. The closer the relationship and the longer the lead time, the better this strategy becomes.

3.2.2 ‘Building Approvals’ Modern Look

Book code

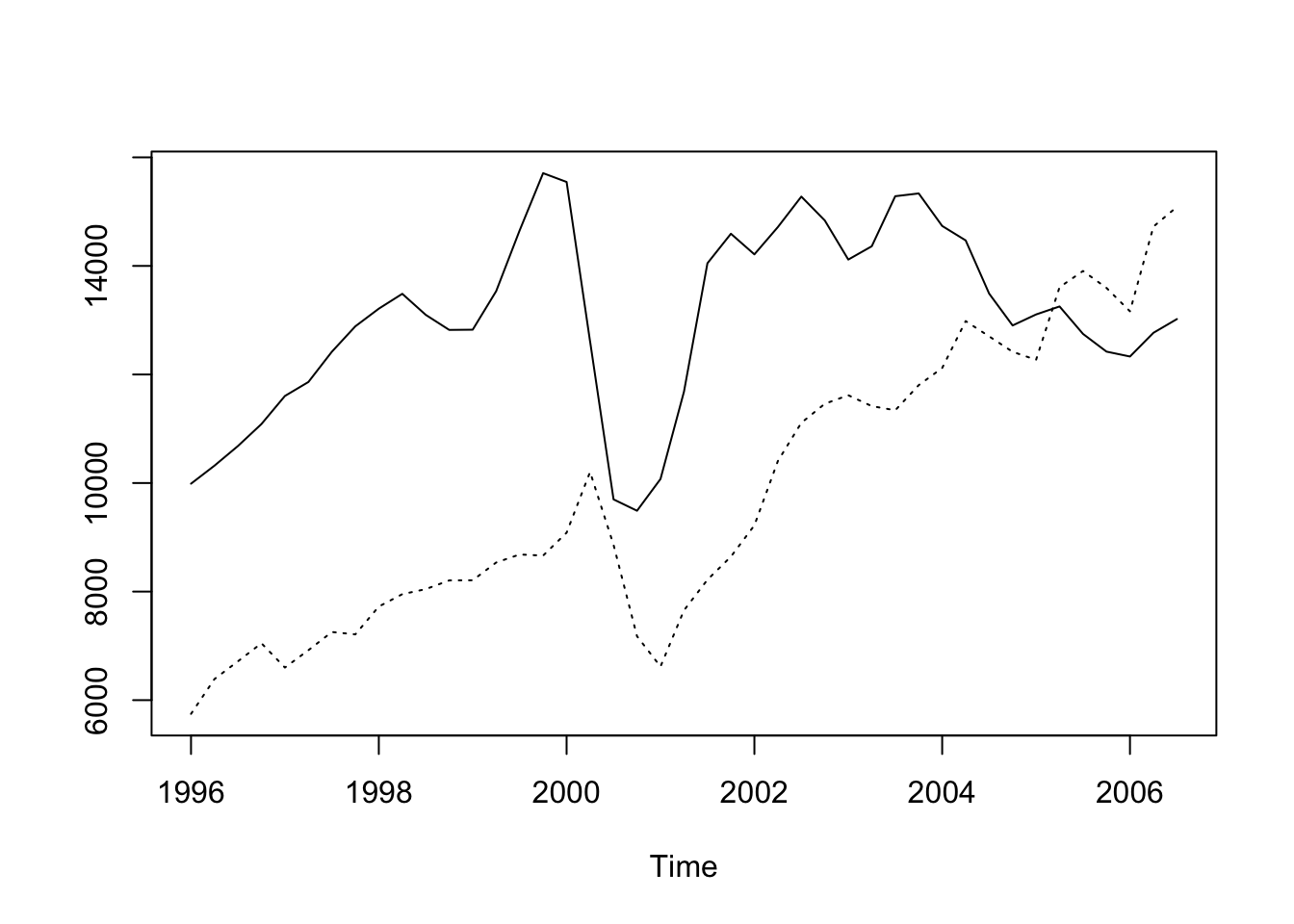

<- read.table ("data/ApprovActiv.dat" , header= T)# attach(Build.dat) # bad practice <- ts (Build.dat$ Approvals, start = c (1996 ,1 ), freq= 4 )<- ts (Build.dat$ Activity, start = c (1996 ,1 ), freq= 4 )ts.plot (App.ts, Act.ts, lty = c (1 ,3 ))

Tidyverts code

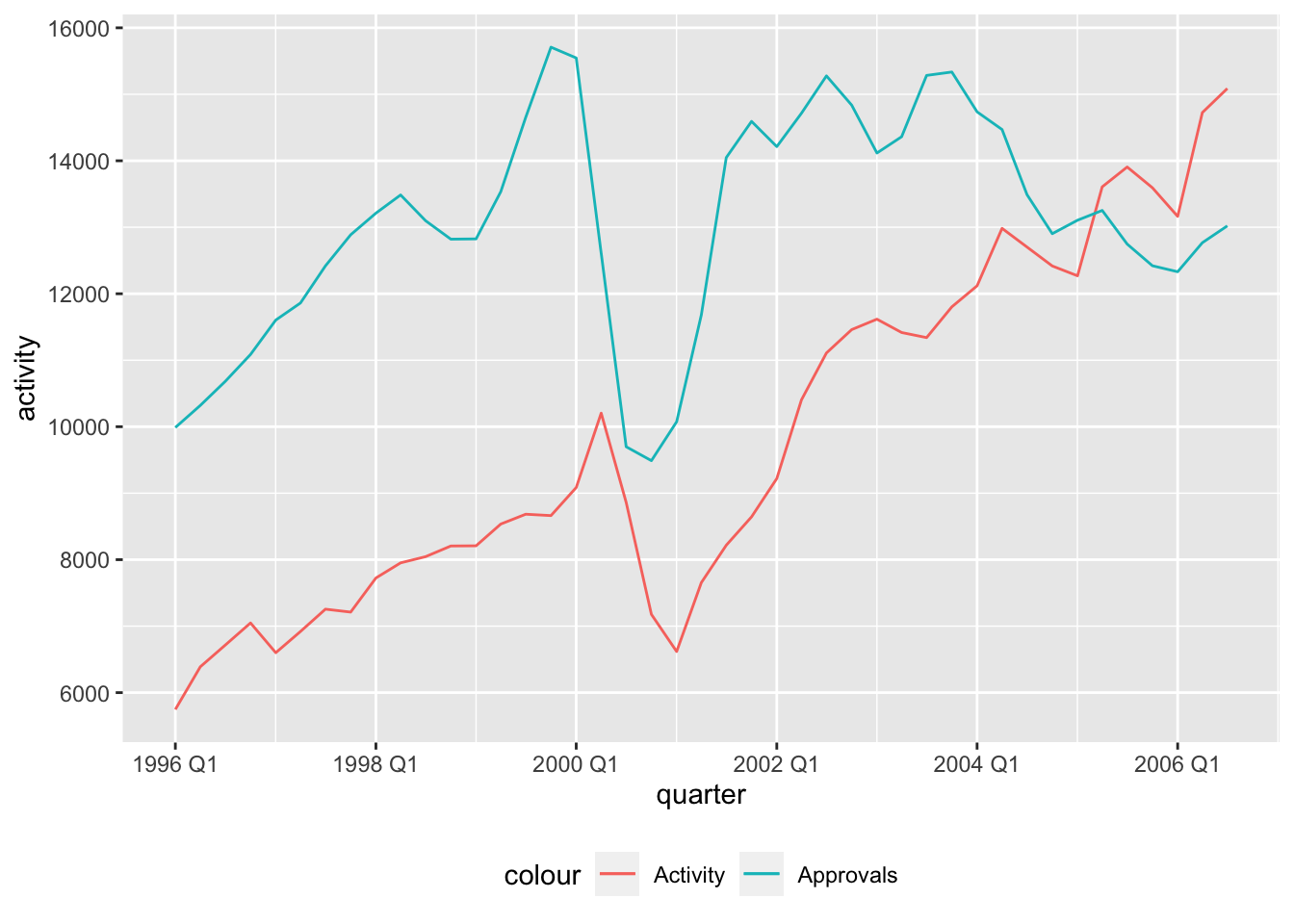

:: p_load ("tsibble" , "fable" , "feasts" ,"tsibbledata" , "fable.prophet" , "tidyverse" , "patchwork" )<- read_table ("data/ApprovActiv.dat" ) |> rename_all (str_to_lower) |> mutate (dates = seq (ymd ("1996-01-01" ), by = "3 months" , length.out = n ()),quarter = yearquarter (dates)) |> as_tsibble (index = quarter)ggplot (build_dat, aes (x = quarter)) + geom_line (aes (y = activity, color = "Activity" )) + geom_line (aes (y = approvals, color = "Approvals" )) + theme (legend.position = "bottom" )

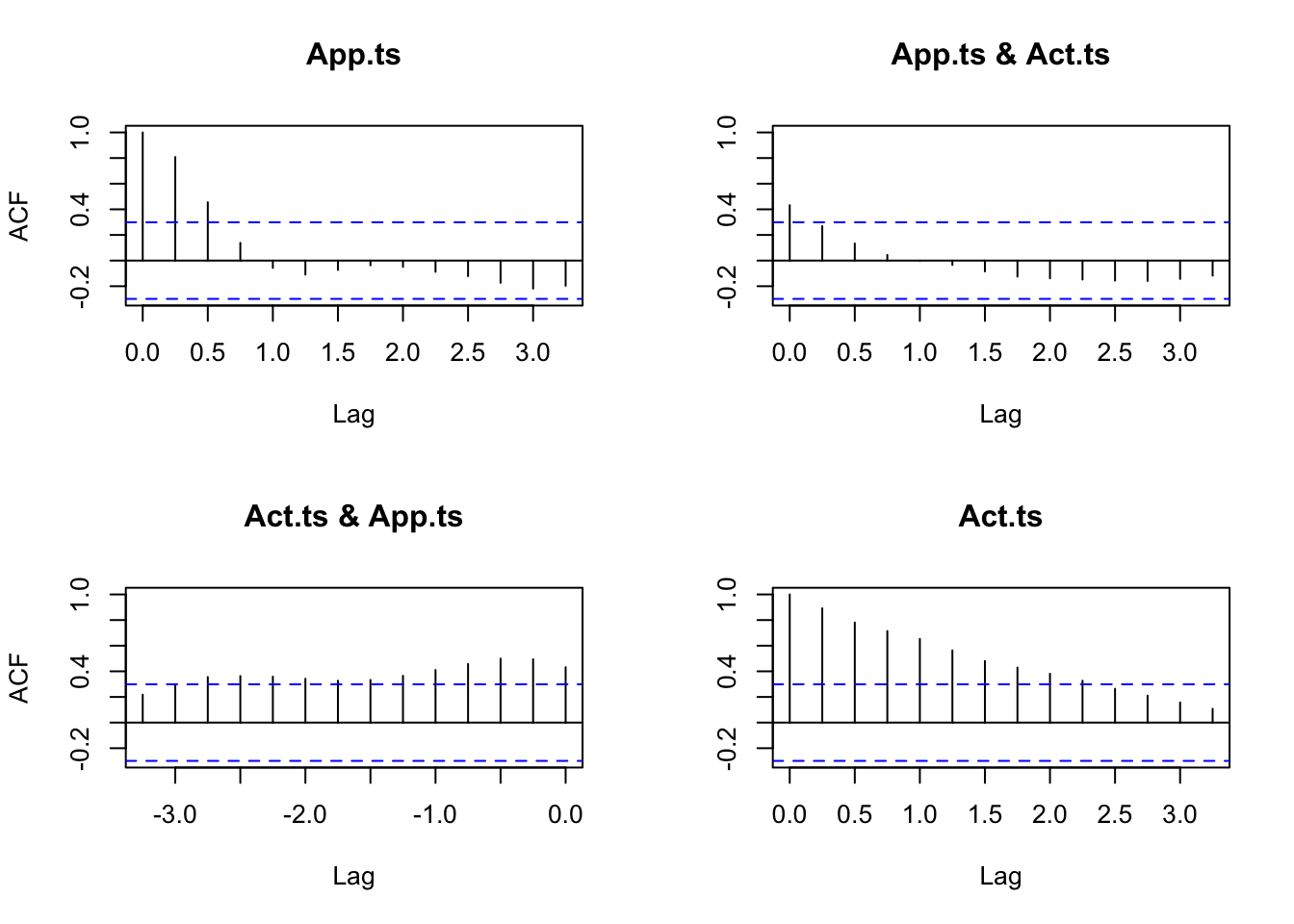

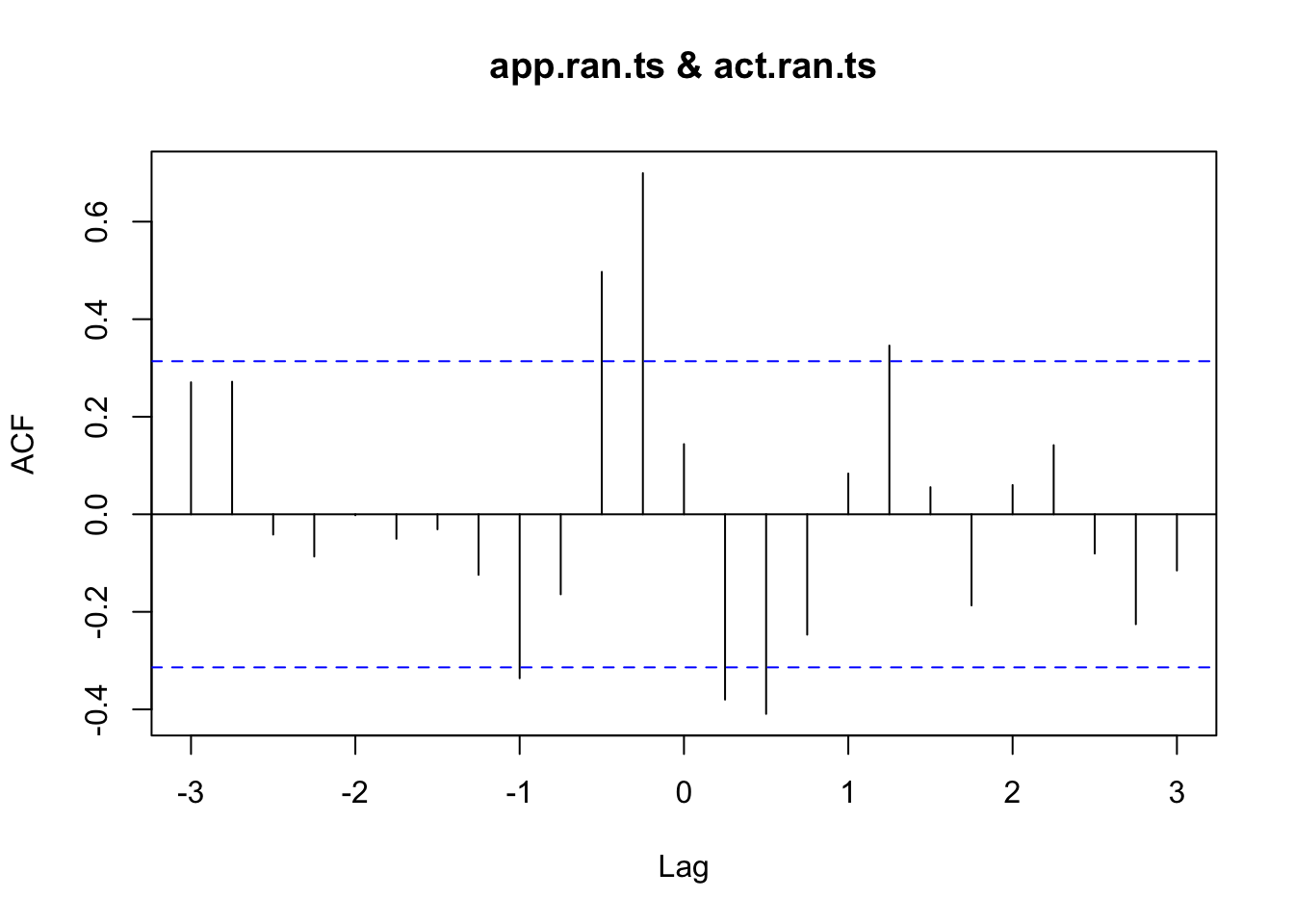

acf (ts.union (App.ts, Act.ts))

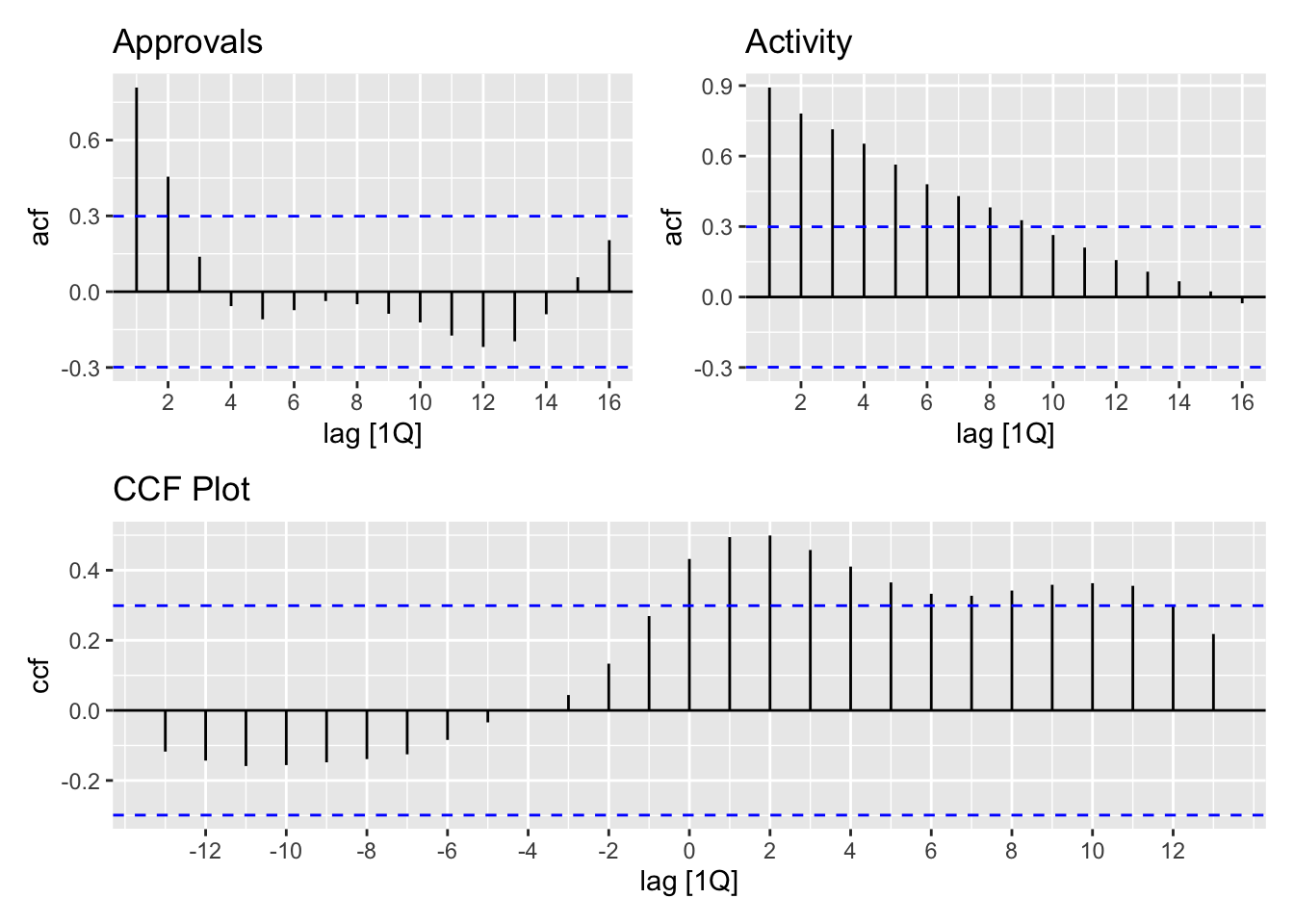

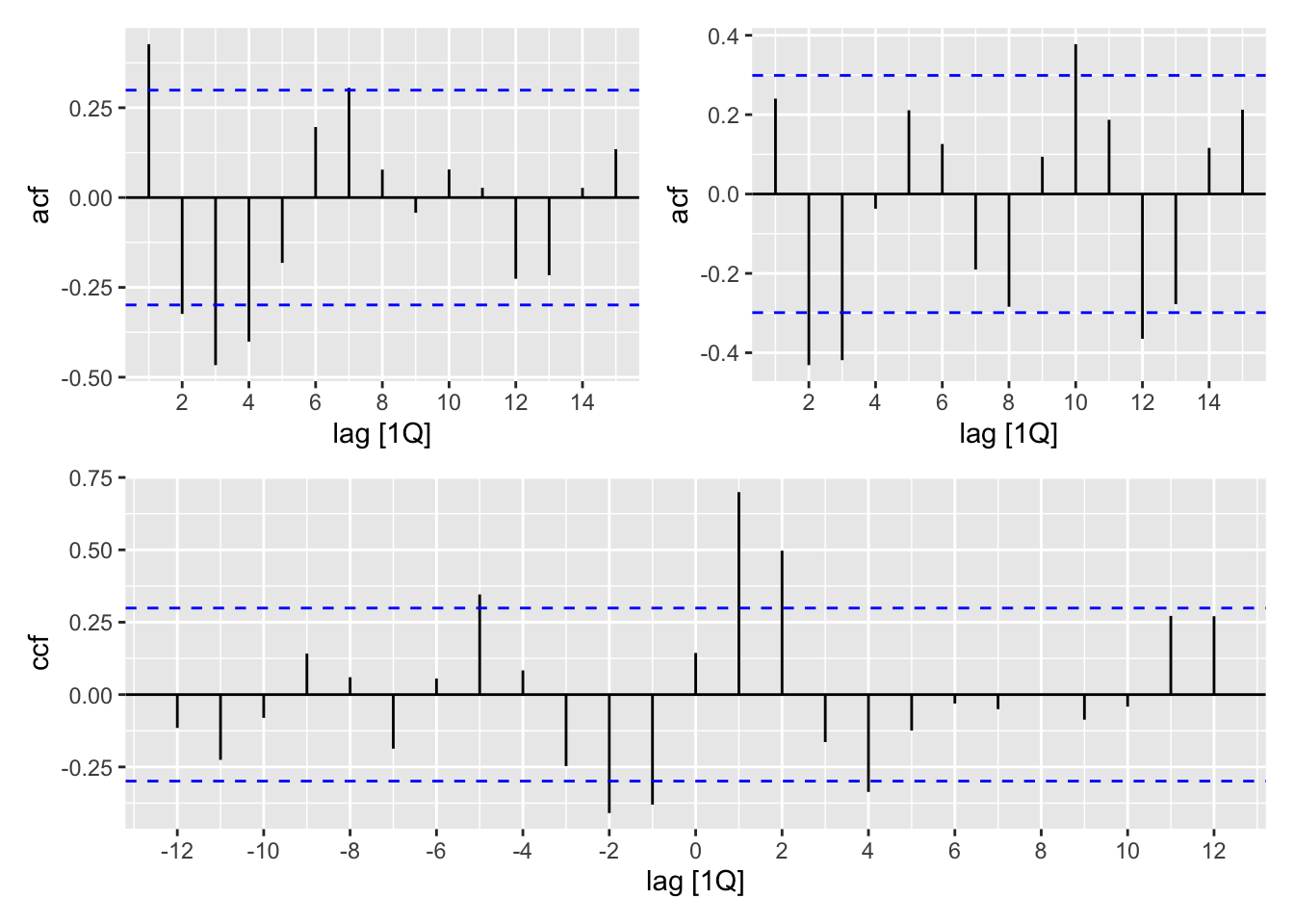

<- ACF (build_dat, y = approvals) |> autoplot () + labs (title = "Approvals" )<- ACF (build_dat, y = activity) |> autoplot () + labs (title = "Activity" )<- build_dat |> CCF (y = approvals, x = activity) |> autoplot () + labs (title = "CCF Plot" )+ acf_act) / joint_ccf_plot

print (acf (ts.union (App.ts, Act.ts), plot = FALSE ))

Autocorrelations of series 'ts.union(App.ts, Act.ts)', by lag

, , App.ts

App.ts Act.ts

1.000 ( 0.00) 0.432 ( 0.00)

0.808 ( 0.25) 0.494 (-0.25)

0.455 ( 0.50) 0.499 (-0.50)

0.138 ( 0.75) 0.458 (-0.75)

-0.057 ( 1.00) 0.410 (-1.00)

-0.109 ( 1.25) 0.365 (-1.25)

-0.073 ( 1.50) 0.333 (-1.50)

-0.037 ( 1.75) 0.327 (-1.75)

-0.050 ( 2.00) 0.342 (-2.00)

-0.087 ( 2.25) 0.358 (-2.25)

-0.122 ( 2.50) 0.363 (-2.50)

-0.174 ( 2.75) 0.356 (-2.75)

-0.219 ( 3.00) 0.298 (-3.00)

-0.196 ( 3.25) 0.218 (-3.25)

, , Act.ts

App.ts Act.ts

0.432 ( 0.00) 1.000 ( 0.00)

0.269 ( 0.25) 0.892 ( 0.25)

0.133 ( 0.50) 0.781 ( 0.50)

0.044 ( 0.75) 0.714 ( 0.75)

-0.002 ( 1.00) 0.653 ( 1.00)

-0.034 ( 1.25) 0.564 ( 1.25)

-0.084 ( 1.50) 0.480 ( 1.50)

-0.125 ( 1.75) 0.430 ( 1.75)

-0.139 ( 2.00) 0.381 ( 2.00)

-0.148 ( 2.25) 0.327 ( 2.25)

-0.156 ( 2.50) 0.264 ( 2.50)

-0.159 ( 2.75) 0.210 ( 2.75)

-0.143 ( 3.00) 0.157 ( 3.00)

-0.118 ( 3.25) 0.108 ( 3.25)

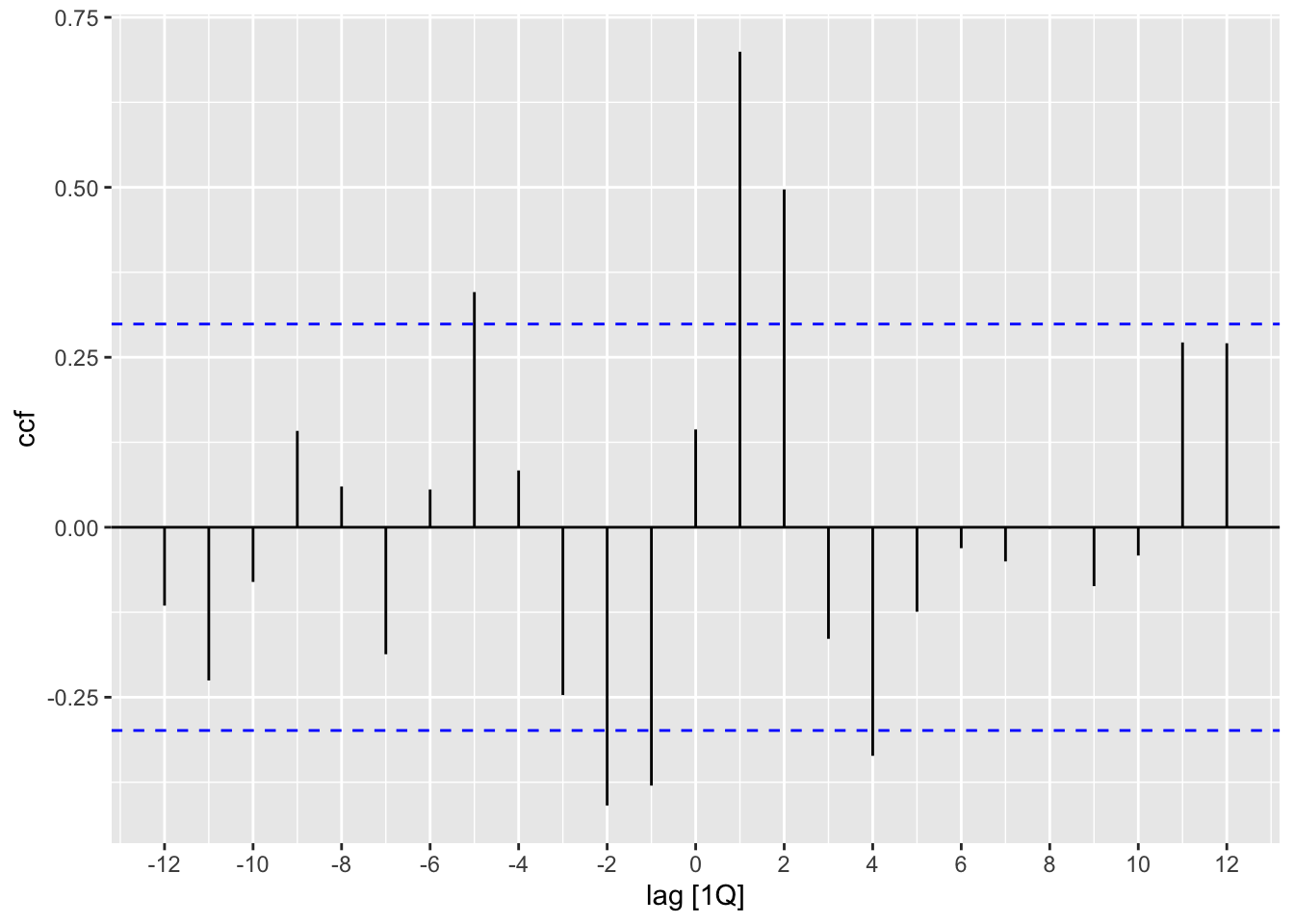

CCF (build_dat, approvals, activity)

# A tsibble: 27 x 2 [1Q]

lag ccf

<cf_lag> <dbl>

1 -13Q -0.118

2 -12Q -0.143

3 -11Q -0.159

4 -10Q -0.156

5 -9Q -0.148

6 -8Q -0.139

7 -7Q -0.125

8 -6Q -0.0843

9 -5Q -0.0342

10 -4Q -0.00202

# ℹ 17 more rows

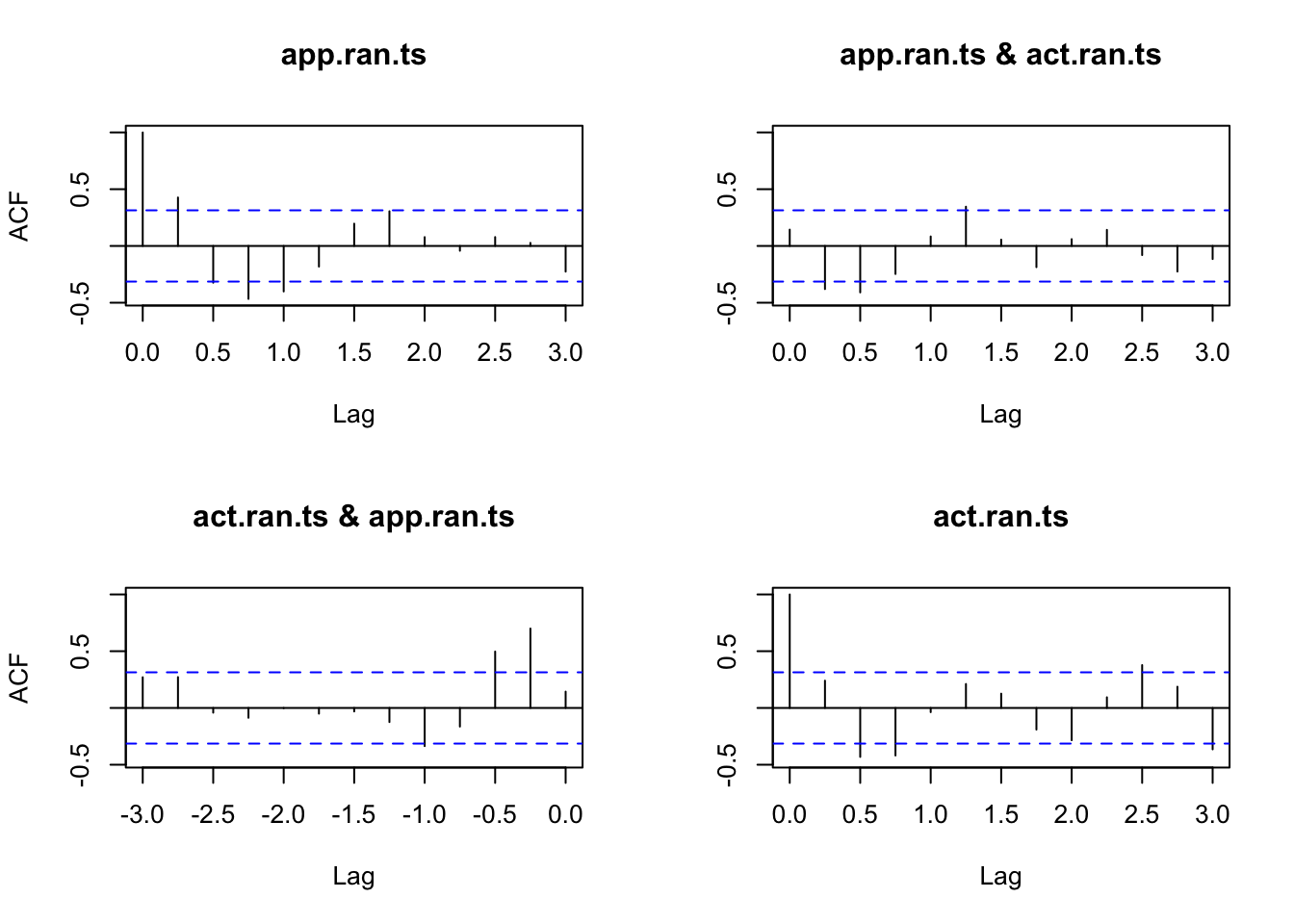

<- decompose (App.ts)$ random<- window (app.ran, start = c (1996 , 3 ), end = c (2006 ,1 )) # add end to fix <- decompose (Act.ts)$ random<- window (act.ran, start = c (1996 , 3 ), end = c (2006 ,1 )) # add end to fix acf (ts.union (app.ran.ts, act.ran.ts))

<- model (build_dat, feasts:: classical_decomposition (approvals)) |> components ()<- model (build_dat, feasts:: classical_decomposition (activity)) |> components ()<- ACF (app_decompose, random) |> autoplot ()<- ACF (act_decompose, random) |> autoplot ()<- select (app_decompose, quarter, random_app = random) |> left_join (select (act_decompose, quarter, random_act = random))<- random_decompose |> CCF (y = random_app, x = random_act) |> autoplot () + act_random) / joint_ccf_random

ccf (app.ran.ts, act.ran.ts)

<- random_decompose |> CCF (y = random_app, x = random_act) |> autoplot ()

print (acf (ts.union (app.ran.ts, act.ran.ts), plot = FALSE ))

Autocorrelations of series 'ts.union(app.ran.ts, act.ran.ts)', by lag

, , app.ran.ts

app.ran.ts act.ran.ts

1.000 ( 0.00) 0.144 ( 0.00)

0.427 ( 0.25) 0.699 (-0.25)

-0.324 ( 0.50) 0.497 (-0.50)

-0.466 ( 0.75) -0.164 (-0.75)

-0.401 ( 1.00) -0.336 (-1.00)

-0.182 ( 1.25) -0.124 (-1.25)

0.196 ( 1.50) -0.031 (-1.50)

0.306 ( 1.75) -0.050 (-1.75)

0.078 ( 2.00) -0.002 (-2.00)

-0.042 ( 2.25) -0.087 (-2.25)

0.078 ( 2.50) -0.042 (-2.50)

0.027 ( 2.75) 0.272 (-2.75)

-0.226 ( 3.00) 0.271 (-3.00)

, , act.ran.ts

app.ran.ts act.ran.ts

0.144 ( 0.00) 1.000 ( 0.00)

-0.380 ( 0.25) 0.240 ( 0.25)

-0.409 ( 0.50) -0.431 ( 0.50)

-0.247 ( 0.75) -0.419 ( 0.75)

0.084 ( 1.00) -0.037 ( 1.00)

0.346 ( 1.25) 0.211 ( 1.25)

0.056 ( 1.50) 0.126 ( 1.50)

-0.187 ( 1.75) -0.190 ( 1.75)

0.060 ( 2.00) -0.284 ( 2.00)

0.142 ( 2.25) 0.094 ( 2.25)

-0.080 ( 2.50) 0.378 ( 2.50)

-0.225 ( 2.75) 0.187 ( 2.75)

-0.115 ( 3.00) -0.365 ( 3.00)

|> CCF (y = random_app, x = random_act)

# A tsibble: 25 x 2 [1Q]

lag ccf

<cf_lag> <dbl>

1 -12Q -0.115

2 -11Q -0.225

3 -10Q -0.0804

4 -9Q 0.142

5 -8Q 0.0600

6 -7Q -0.187

7 -6Q 0.0556

8 -5Q 0.346

9 -4Q 0.0836

10 -3Q -0.247

# ℹ 15 more rows

Show the Book code in full

<- read.table ("data/ApprovActiv.dat" , header= T)# attach(Build.dat) # bad practice <- ts (Build.dat$ Approvals, start = c (1996 ,1 ), freq= 4 )<- ts (Build.dat$ Activity, start = c (1996 ,1 ), freq= 4 )ts.plot (App.ts, Act.ts, lty = c (1 ,3 ))acf (ts.union (App.ts, Act.ts))print (acf (ts.union (App.ts, Act.ts)))<- decompose (App.ts)$ random<- window (app.ran, start = c (1996 , 3 ), end = c (2006 ,1 )) # add end to fix <- decompose (Act.ts)$ random<- window (act.ran, start = c (1996 , 3 ), end = c (2006 ,1 )) # add end to fix acf (ts.union (app.ran.ts, act.ran.ts))ccf (app.ran.ts, act.ran.ts)print (acf (ts.union (app.ran.ts, act.ran.ts)))

Show the Tidyverts code in full

:: p_load ("tsibble" , "fable" , "feasts" ,"tsibbledata" , "fable.prophet" , "tidyverse" , "patchwork" )<- read_table ("data/ApprovActiv.dat" ) |> rename_all (str_to_lower) |> mutate (dates = seq (ymd ("1996-01-01" ), by = "3 months" , length.out = n ()),quarter = yearquarter (dates)) |> as_tsibble (index = quarter)ggplot (build_dat, aes (x = quarter)) + geom_line (aes (y = activity, color = "Activity" )) + geom_line (aes (y = approvals, color = "Approvals" )) + theme (legend.position = "bottom" )<- ACF (build_dat, y = approvals) |> autoplot () + labs (title = "Approvals" )<- ACF (build_dat, y = activity) |> autoplot () + labs (title = "Activity" )<- build_dat |> CCF (y = approvals, x = activity) |> autoplot () + labs (title = "CCF Plot" )+ acf_act) / joint_ccf_plotCCF (build_dat, approvals, activity)<- model (build_dat, feasts:: classical_decomposition (approvals)) |> components ()<- model (build_dat, feasts:: classical_decomposition (activity)) |> components ()<- ACF (app_decompose, random) |> autoplot ()<- ACF (act_decompose, random) |> autoplot ()<- select (app_decompose, quarter, random_app = random) |> left_join (select (act_decompose, quarter, random_act = random))<- random_decompose |> CCF (y = random_app, x = random_act) |> autoplot () + act_random) / joint_ccf_random<- random_decompose |> CCF (y = random_app, x = random_act) |> autoplot ()|> CCF (y = random_app, x = random_act)

The output from feasts::ACF() has a starkly different structure than the output of acf(). The following code snippet does additional wrangling to get the output in a more comparable format as shown below.

Explore Tidyverts code to match base R acf() output

<- read_table ("data/ApprovActiv.dat" ) |> rename_all (str_to_lower) |> mutate (dates = seq (ymd ("1996-01-01" ), by = "3 months" , length.out = n ()),quarter = yearquarter (dates)) |> pivot_longer (approvals: activity) |> as_tsibble (index = quarter, key = name)<- ACF (build_dat, y = value) |> pivot_wider (names_from = "name" ,values_from = "acf" ,names_prefix = "acf_" |> as_tibble () |> mutate (lag = as.character (lag)) |> bind_rows (tibble (lag = "0Q" , acf_activity = NA ,acf_approvals = NA <- build_dat |> pivot_wider (values_from = "value" , names_from = "name" ) |> CCF (y = approvals, x = activity) |> as_tibble () |> mutate (relation = ifelse (str_detect (lag, "-" ),"appTOact" , "actTOapp" ),lag = str_remove (lag, "-" )) |> pivot_wider (names_from = "relation" ,values_from = "ccf" ,names_prefix = "ccf_" ) |> mutate (ccf_appTOact = ifelse (is.na (ccf_appTOact), ccf_actTOapp, ccf_appTOact)left_join (ccf_dat, acf_dat) |> arrange (- row_number ()) |> select (acf_approvals, ccf_actTOapp, ccf_appTOact, acf_activity)

# A tibble: 14 × 4

acf_approvals ccf_actTOapp ccf_appTOact acf_activity

<dbl> <dbl> <dbl> <dbl>

1 NA 0.432 0.432 NA

2 0.808 0.494 0.269 0.892

3 0.455 0.499 0.133 0.781

4 0.138 0.458 0.0439 0.714

5 -0.0572 0.410 -0.00202 0.653

6 -0.109 0.365 -0.0342 0.564

7 -0.0731 0.333 -0.0843 0.480

8 -0.0371 0.327 -0.125 0.430

9 -0.0496 0.342 -0.139 0.381

10 -0.0874 0.358 -0.148 0.327

11 -0.122 0.363 -0.156 0.264

12 -0.174 0.356 -0.159 0.210

13 -0.219 0.298 -0.143 0.157

14 -0.196 0.218 -0.118 0.108

3.3.4 Bass Model Example Modern Look

Book code

<- 1 : 10 <- (1 : 100 ) / 10 <- c (840 ,1470 ,2110 ,4000 , 7590 , 10950 , 10530 , 9470 , 7790 , 5890 )<- cumsum (Sales)<- nls (Sales ~ M * ( ((P+ Q)^ 2 / P) * exp (- (P+ Q) * T79) ) / 1 + (Q/ P)* exp (- (P+ Q)* T79))^ 2 , start = list (M= 60630 , P= 0.03 , Q= 0.38 ))summary (Bass.nls)

Formula: Sales ~ M * (((P + Q)^2/P) * exp(-(P + Q) * T79))/(1 + (Q/P) *

exp(-(P + Q) * T79))^2

Parameters:

Estimate Std. Error t value Pr(>|t|)

M 6.798e+04 3.128e+03 21.74 1.10e-07 ***

P 6.594e-03 1.430e-03 4.61 0.00245 **

Q 6.381e-01 4.140e-02 15.41 1.17e-06 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 727.2 on 7 degrees of freedom

Number of iterations to convergence: 8

Achieved convergence tolerance: 7.395e-06

Tidyverts code

<- tibble (T79 = 1 : 10 ,Sales = c (840 ,1470 ,2110 ,4000 , 7590 , 10950 , 10530 , 9470 , 7790 , 5890 )) |> mutate (Cusales = cumsum (Sales))<- Sales ~ M * ( ((P+ Q)^ 2 / P) * exp (- (P+ Q) * T79) ) / (1 + (Q/ P)* exp (- (P+ Q)* T79))^ 2 <- nls (equation, data = dat, start = list (M= 60630 , P= 0.03 , Q= 0.38 ))summary (bass_nls)

Formula: Sales ~ M * (((P + Q)^2/P) * exp(-(P + Q) * T79))/(1 + (Q/P) *

exp(-(P + Q) * T79))^2

Parameters:

Estimate Std. Error t value Pr(>|t|)

M 6.798e+04 3.128e+03 21.74 1.10e-07 ***

P 6.594e-03 1.430e-03 4.61 0.00245 **

Q 6.381e-01 4.140e-02 15.41 1.17e-06 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 727.2 on 7 degrees of freedom

Number of iterations to convergence: 8

Achieved convergence tolerance: 7.395e-06

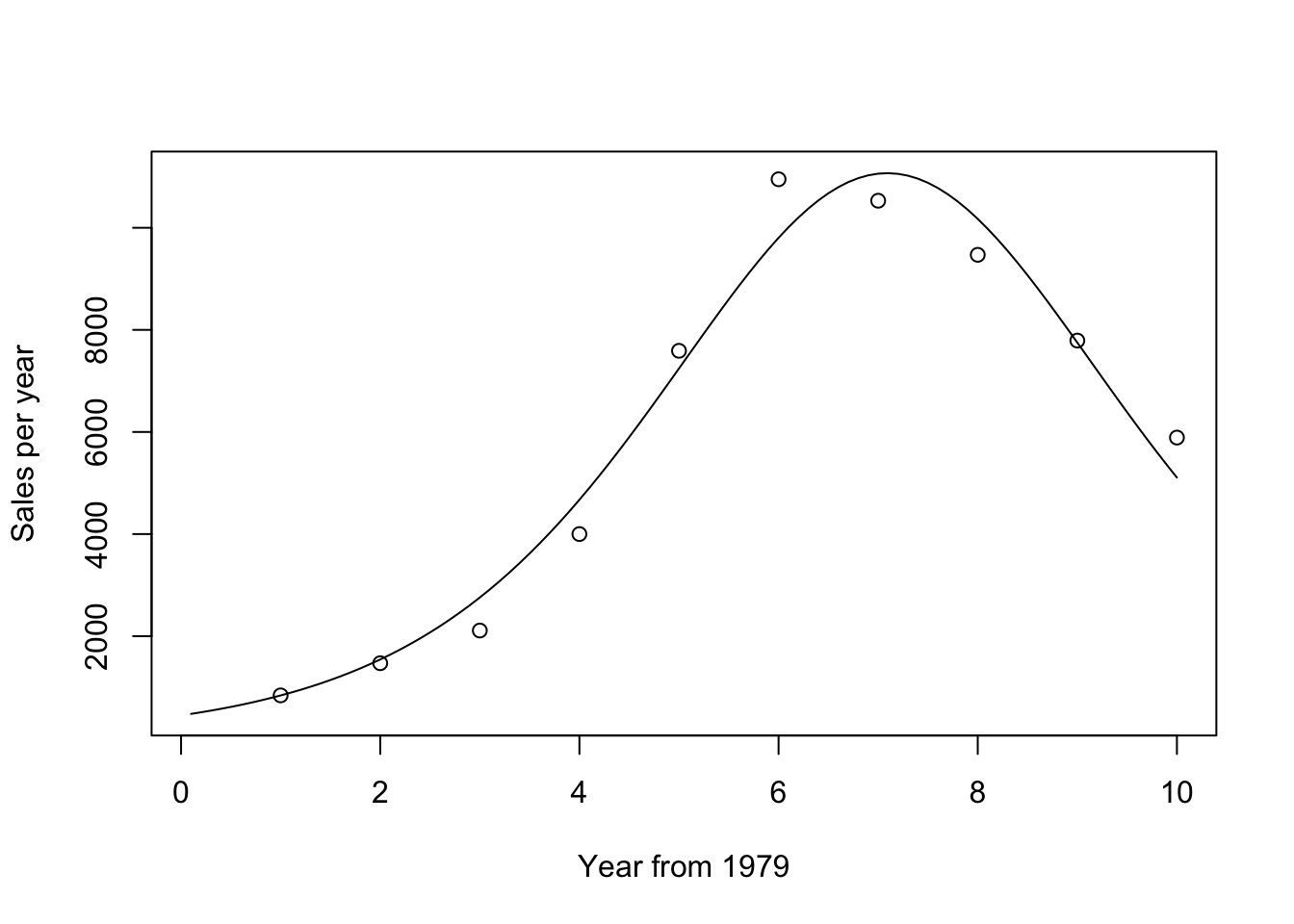

<- coef (Bass.nls)<- Bcoef[1 ]<- Bcoef[2 ]<- Bcoef[3 ]<- exp (- (p+ q) * Tdelt)<- m * ( (p+ q)^ 2 / p ) * ngete / (1 + (q/ p) * ngete)^ 2 plot (Tdelt, Bpdf,xlab = "Year from 1979" ,ylab = "Sales per year" , type= 'l' )points (T79, Sales)

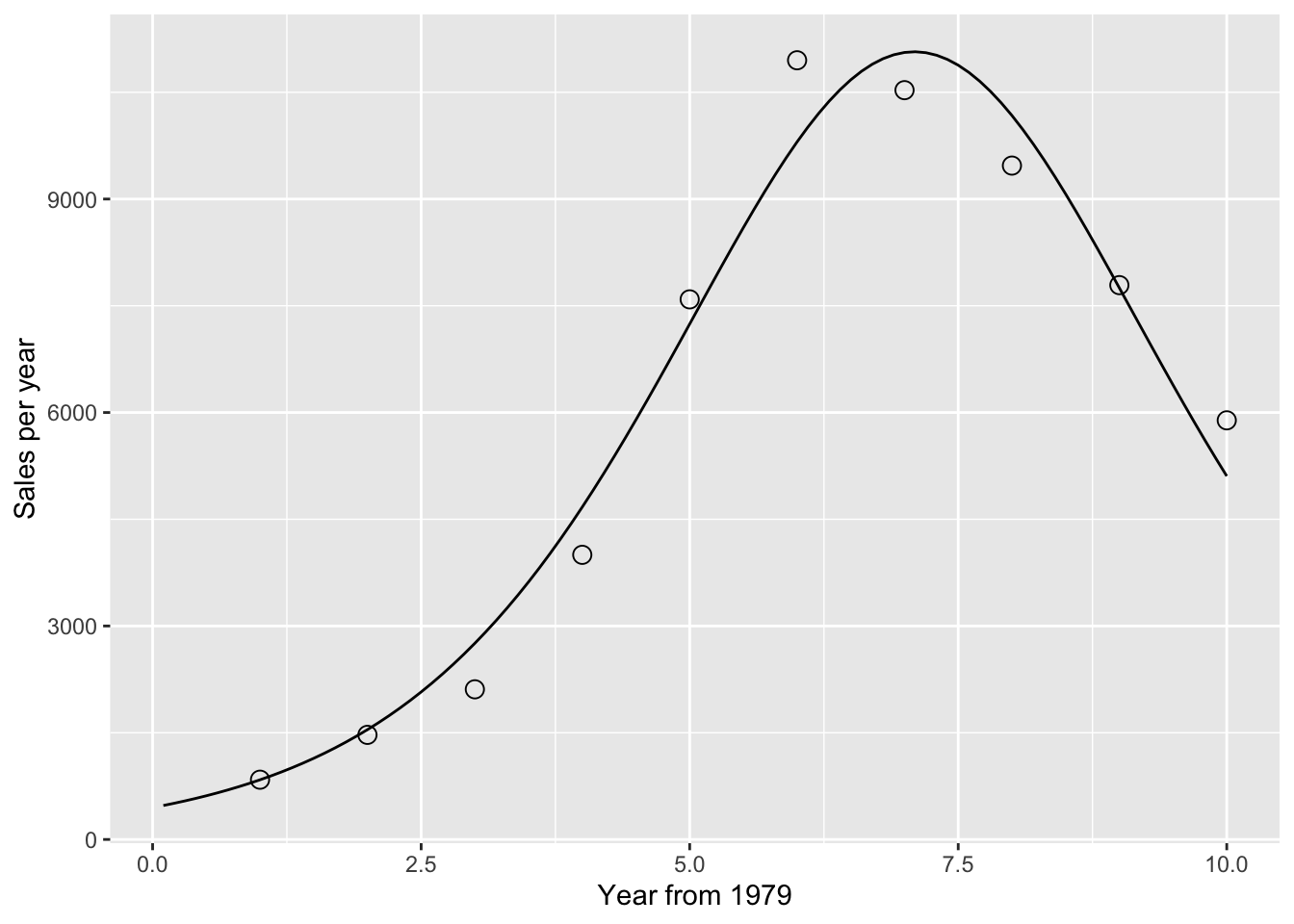

<- tibble (tdelt = (1 : 100 ) / 10 ,m = coef (bass_nls)["M" ],p = coef (bass_nls)["P" ],q = coef (bass_nls)["Q" ]) |> mutate (ngete = exp (- (p+ q) * tdelt),bpdf = m * ( (p+ q)^ 2 / p ) * ngete / (1 + (q/ p) * ngete)^ 2 )ggplot (pdat, aes (x = tdelt, y = bpdf)) + geom_line () + geom_point (data = dat,aes (x = T79, y = Sales),size = 3 , shape = 1 ) + labs (x = "Year from 1979" , y = "Sales per year" )

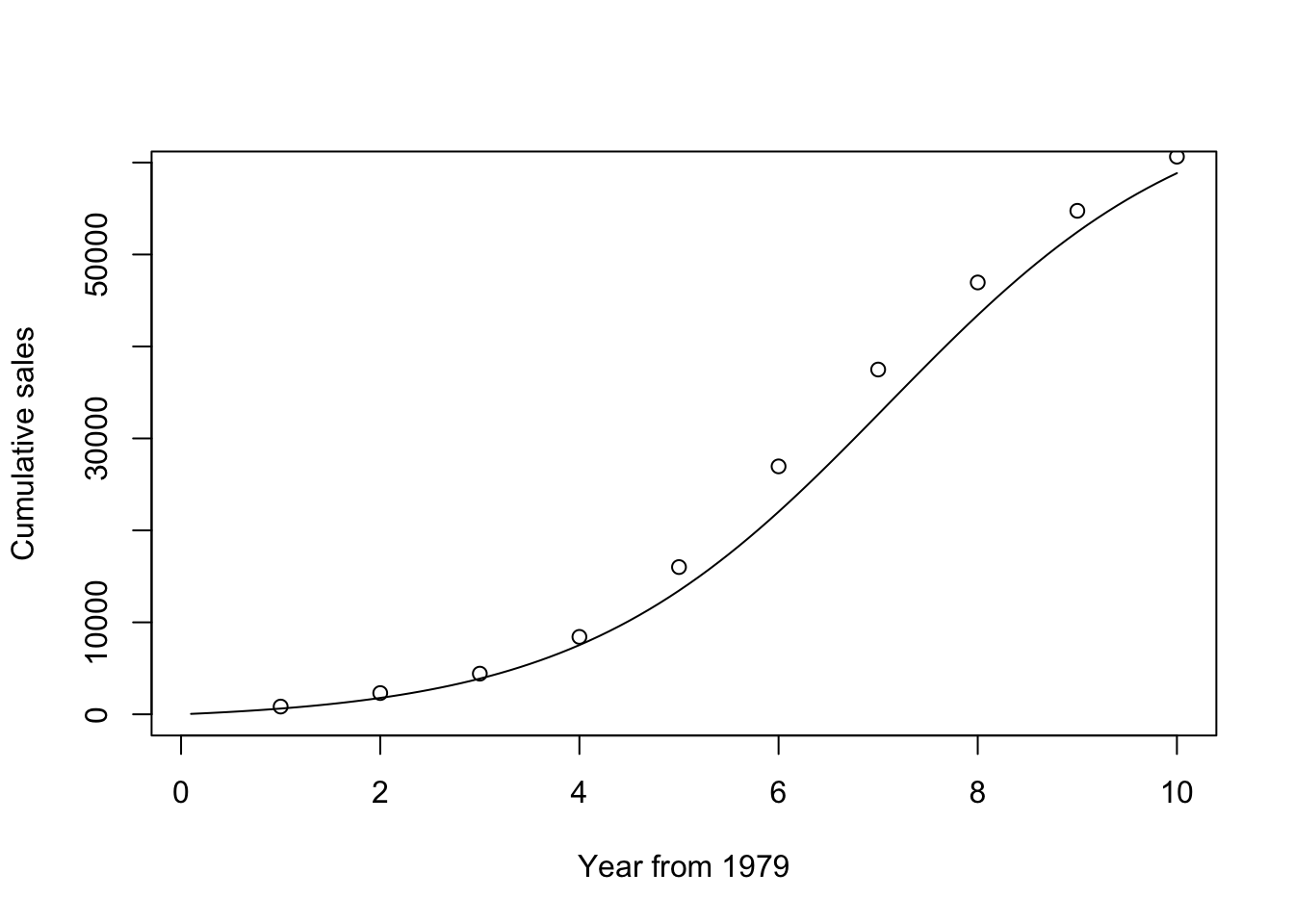

<- m * (1 - ngete)/ (1 + (q/ p)* ngete)plot (Tdelt, Bcdf,xlab = "Year from 1979" ,ylab = "Cumulative sales" , type= 'l' )points (T79, Cusales)

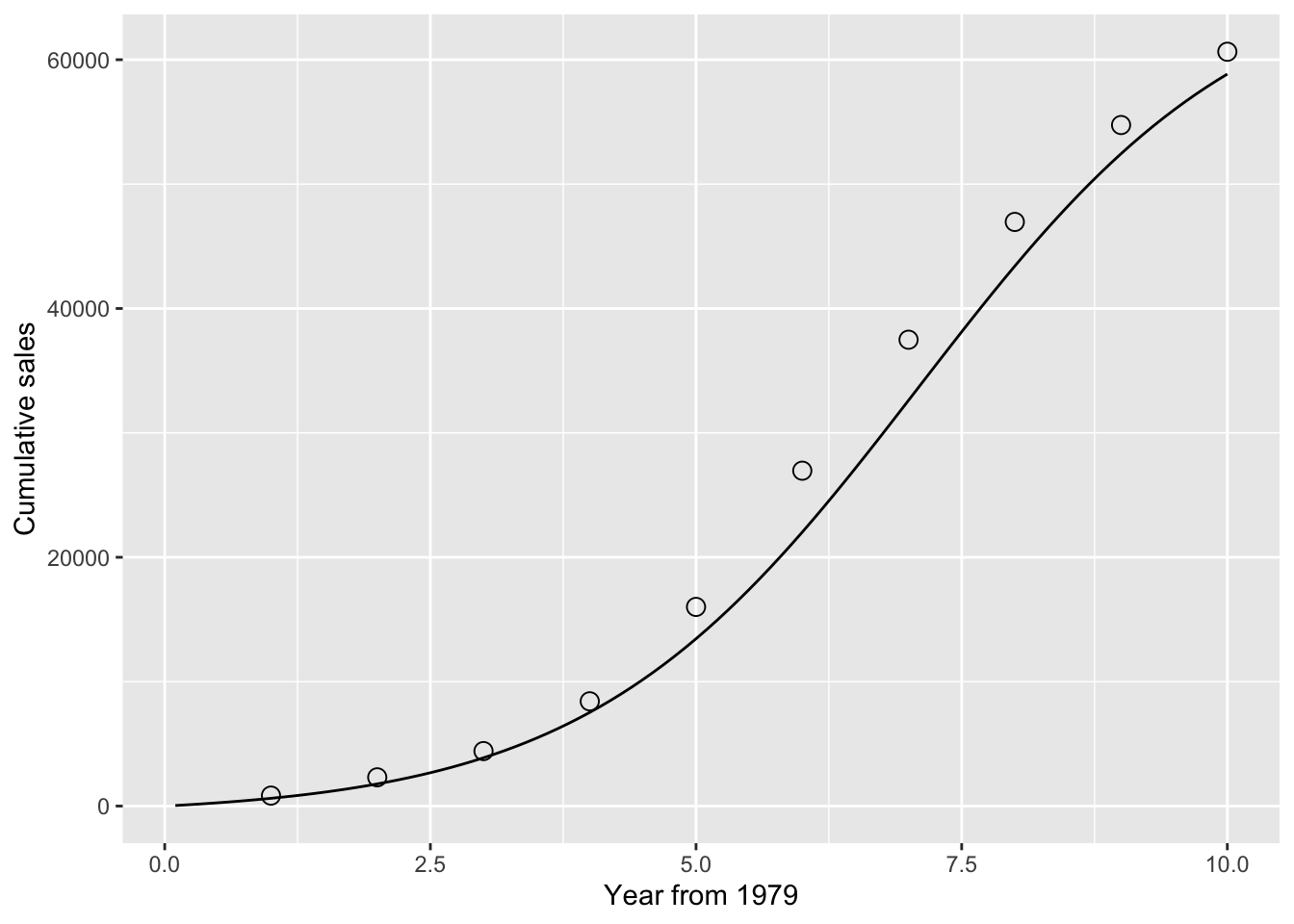

<- mutate (pdat, bcdf = m * (1 - ngete)/ (1 + (q/ p) * ngete))ggplot (pdat, aes (x = tdelt, y = bcdf)) + geom_line () + geom_point (data = dat,aes (x = T79, y = Cusales),size = 3 , shape = 1 ) + labs (x = "Year from 1979" ,y = "Cumulative sales" )

Show the Book code in full

<- 1 : 10 <- (1 : 100 ) / 10 <- c (840 ,1470 ,2110 ,4000 , 7590 , 10950 , 10530 , 9470 , 7790 , 5890 )<- cumsum (Sales)<- nls (Sales ~ M * ( ((P+ Q)^ 2 / P) * exp (- (P+ Q) * T79) ) / 1 + (Q/ P)* exp (- (P+ Q)* T79))^ 2 , start = list (M= 60630 , P= 0.03 , Q= 0.38 ))summary (Bass.nls)<- coef (Bass.nls)<- Bcoef[1 ]<- Bcoef[2 ]<- Bcoef[3 ]<- exp (- (p+ q) * Tdelt)<- m * ( (p+ q)^ 2 / p ) * ngete / (1 + (q/ p) * ngete)^ 2 plot (Tdelt, Bpdf,xlab = "Year from 1979" ,ylab = "Sales per year" , type= 'l' )points (T79, Sales)<- m * (1 - ngete)/ (1 + (q/ p)* ngete)plot (Tdelt, Bcdf,xlab = "Year from 1979" ,ylab = "Cumulative sales" , type= 'l' )points (T79, Cusales)

Show the Tidyverts code in full

<- tibble (T79 = 1 : 10 ,Sales = c (840 ,1470 ,2110 ,4000 , 7590 , 10950 , 10530 , 9470 , 7790 , 5890 )) |> mutate (Cusales = cumsum (Sales))<- Sales ~ M * ( ((P+ Q)^ 2 / P) * exp (- (P+ Q) * T79) ) / (1 + (Q/ P)* exp (- (P+ Q)* T79))^ 2 <- nls (equation, data = dat, start = list (M= 60630 , P= 0.03 , Q= 0.38 ))summary (bass_nls)<- tibble (tdelt = (1 : 100 ) / 10 ,m = coef (bass_nls)["M" ],p = coef (bass_nls)["P" ],q = coef (bass_nls)["Q" ]) |> mutate (ngete = exp (- (p+ q) * tdelt),bpdf = m * ( (p+ q)^ 2 / p ) * ngete / (1 + (q/ p) * ngete)^ 2 )ggplot (pdat, aes (x = tdelt, y = bpdf)) + geom_line () + geom_point (data = dat,aes (x = T79, y = Sales),size = 3 , shape = 1 ) + labs (x = "Year from 1979" , y = "Sales per year" )<- mutate (pdat, bcdf = m * (1 - ngete)/ (1 + (q/ p) * ngete))ggplot (pdat, aes (x = tdelt, y = bcdf)) + geom_line () + geom_point (data = dat,aes (x = T79, y = Cusales),size = 3 , shape = 1 ) + labs (x = "Year from 1979" , y = "Cumulative sales" )

3.4.1 “Exponential smoothing” and “Complaints” Modern Look

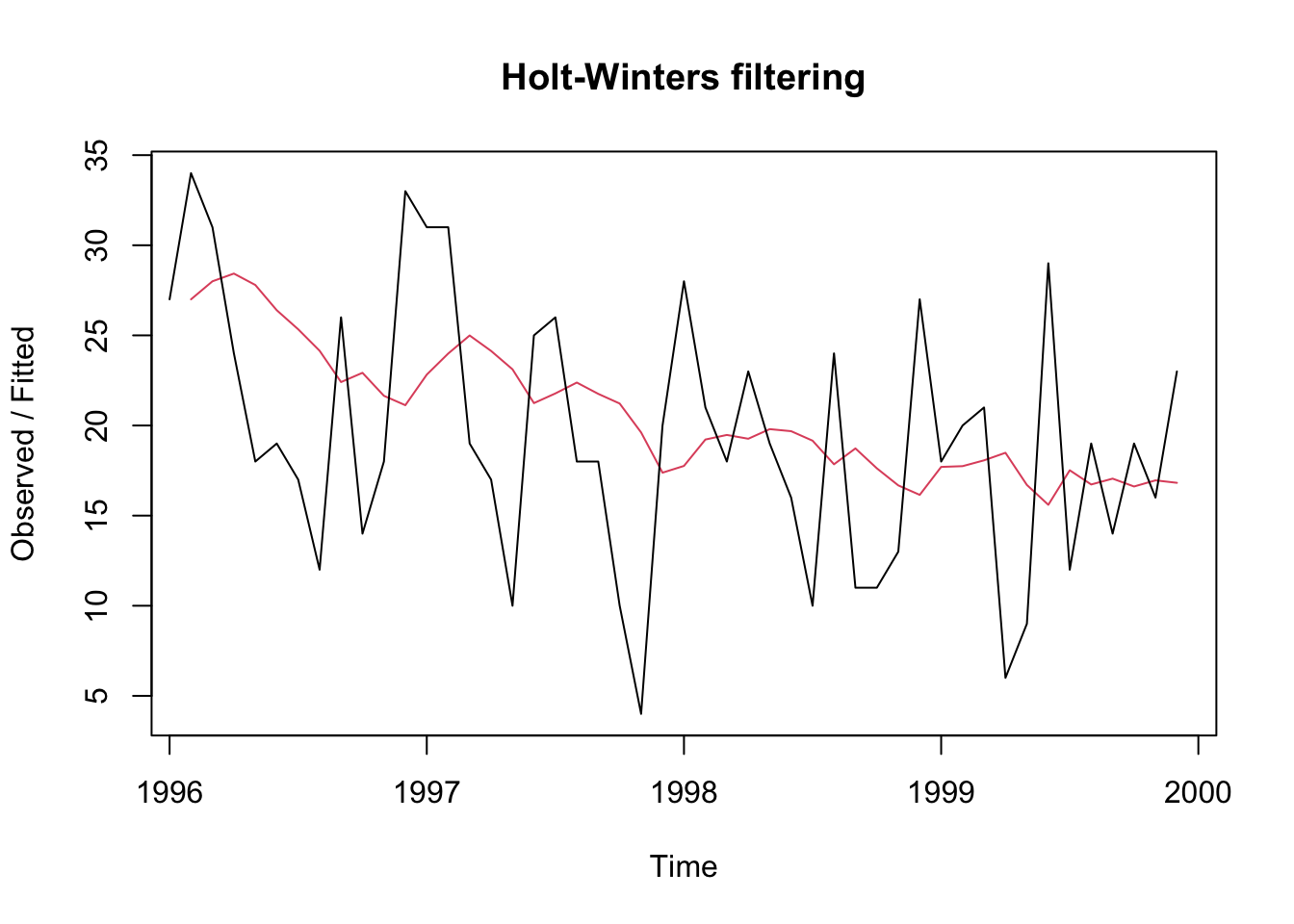

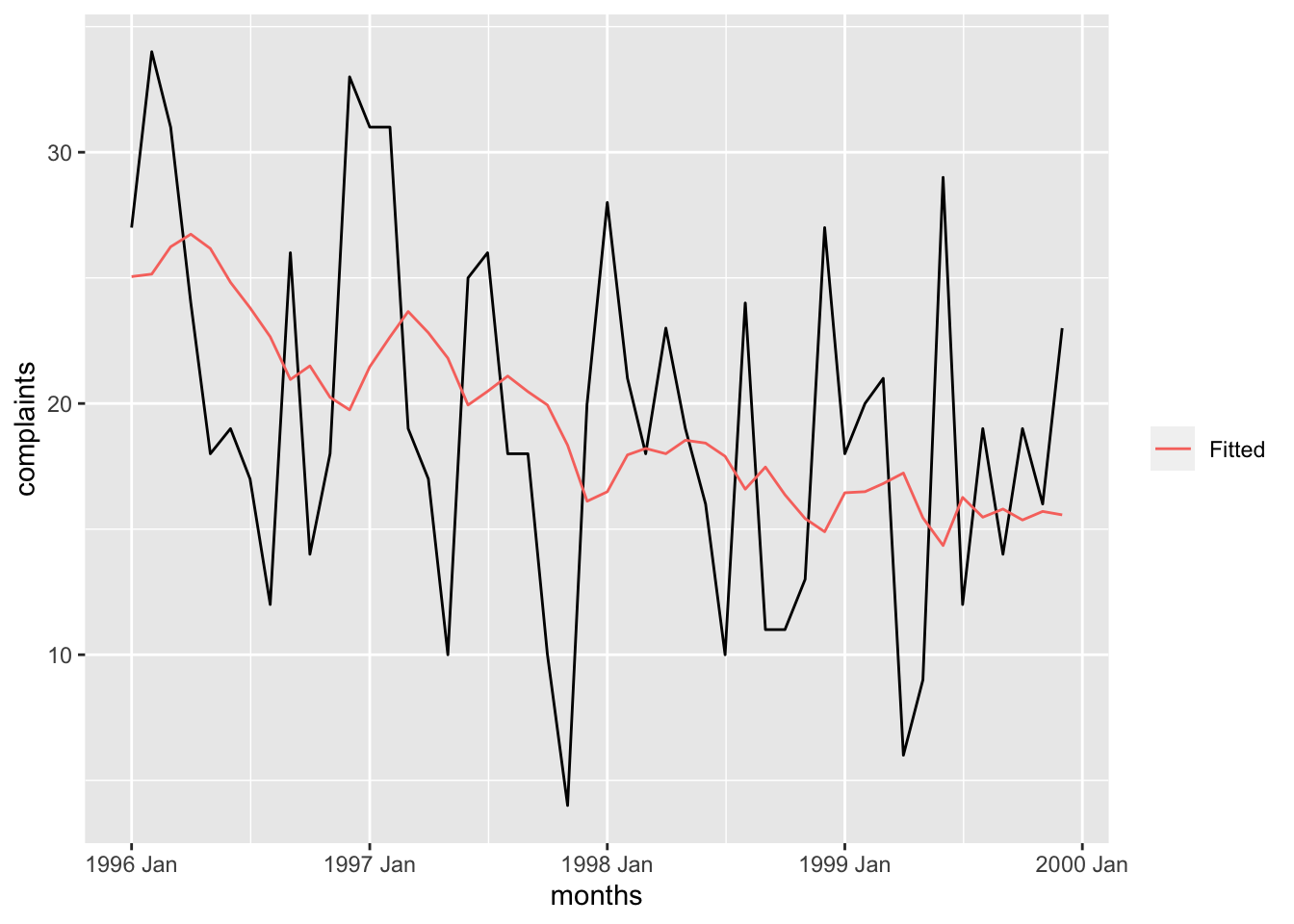

The HoltWinters methods do not return the same results between the HoltWinters() and the feasts::model(ETS()) methods. It appears that the estimation methods used within each package to implement the HoltWinters methods differ slightly.

Book code

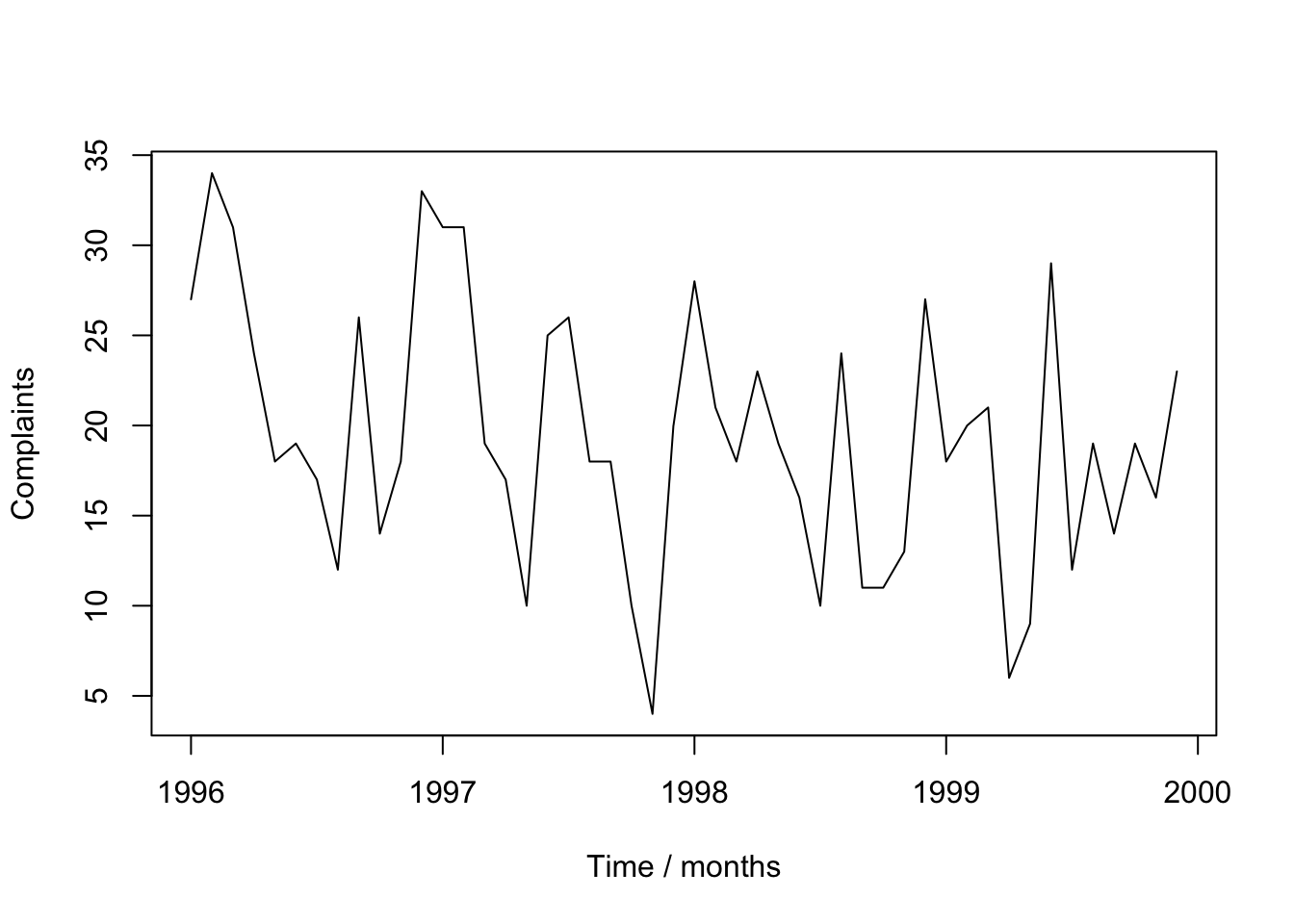

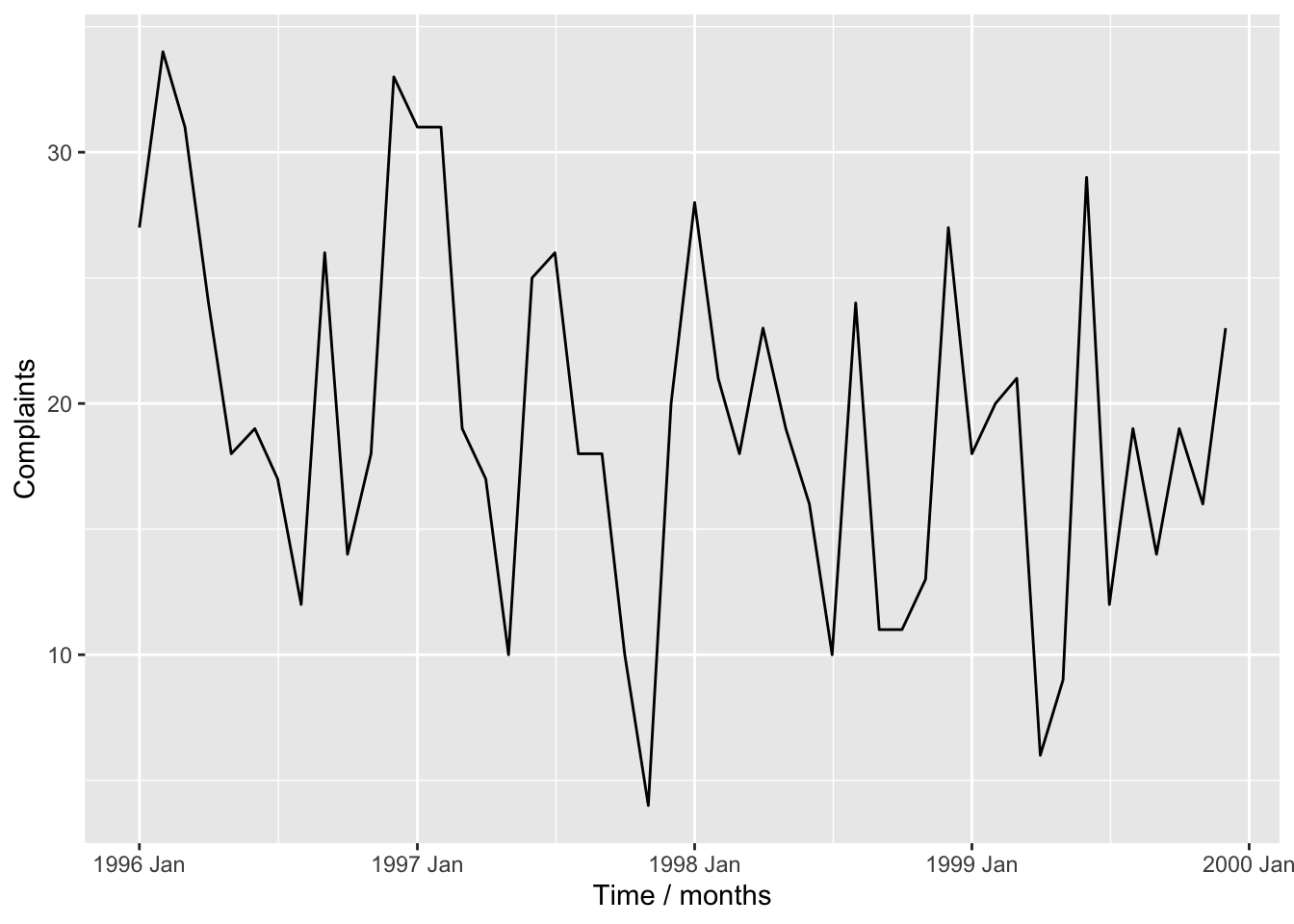

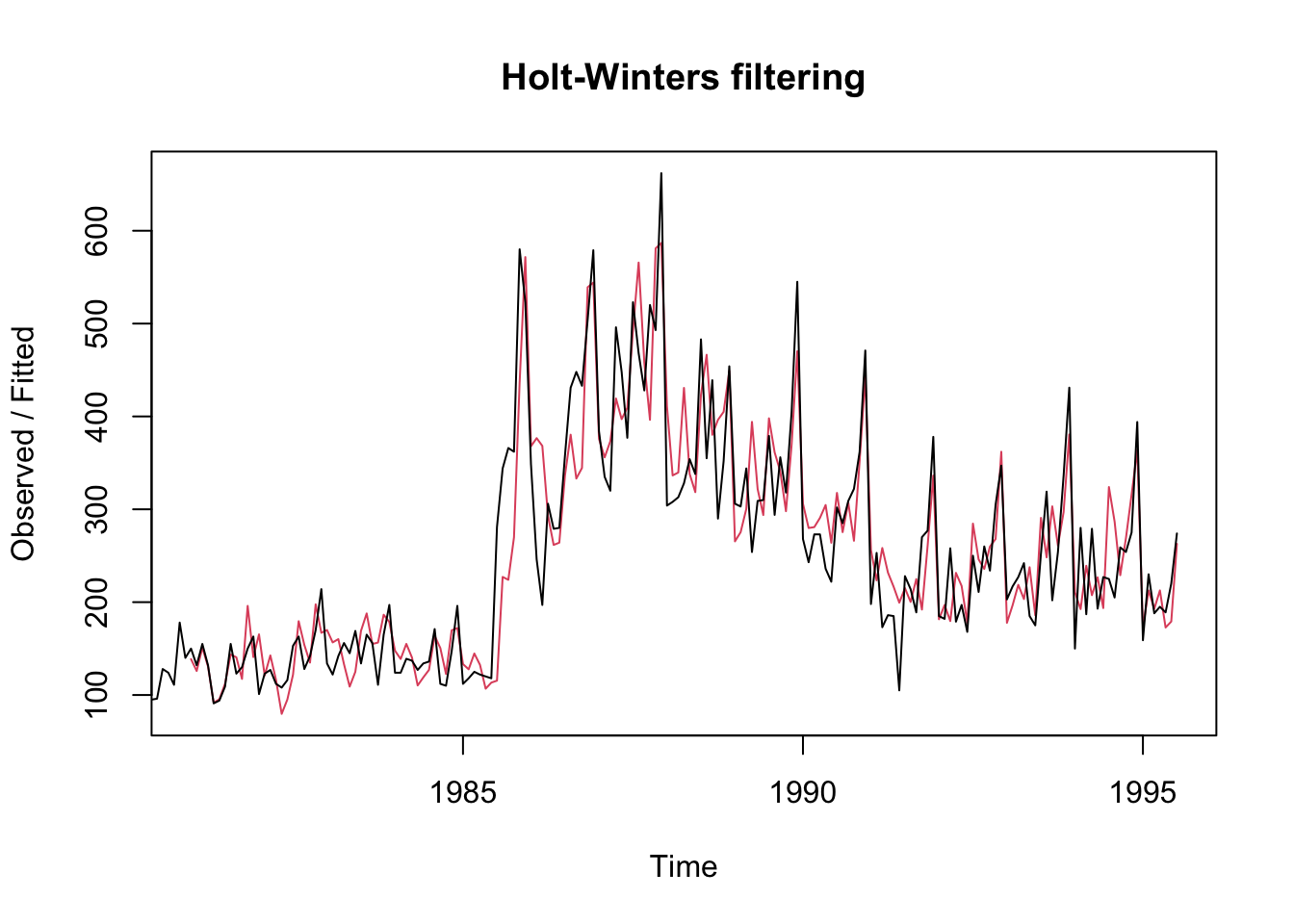

<- read.table ("data/motororg.dat" , header = T)# attach(Motor.dat) # bad practice <- ts (Motor.dat$ complaints, start = c (1996 , 1 ), freq = 12 )plot (Comp.ts, xlab = "Time / months" , ylab = "Complaints" )

Tidyverts code

<- read_table ("data/motororg.dat" ) |> mutate (dates = seq (ymd ("1996-01-01" ), by = "1 months" ,length.out = n ()),months = yearmonth (dates)<- as_tsibble (motor_dat, index = months)autoplot (comp_ts) + labs (x = "Time / months" , y = "Complaints" )

<- HoltWinters (Comp.ts,beta = FALSE , gamma = FALSE )) # edits to book code

Holt-Winters exponential smoothing without trend and without seasonal component.

Call:

HoltWinters(x = Comp.ts, beta = FALSE, gamma = FALSE)

Smoothing parameters:

alpha: 0.1429622

beta : FALSE

gamma: FALSE

Coefficients:

[,1]

a 17.70343

<- comp_ts |> model (Additive = ETS (complaints ~ trend ("A" , alpha = 0.1429622 , beta = 0 ) + error ("A" ) + season ("N" ),opt_crit = "amse" , nmse = 1 ))report (comp_hw1)

Series: complaints

Model: ETS(A,A,N)

Smoothing parameters:

alpha = 0.1429622

beta = 0

Initial states:

l[0] b[0]

25.22968 -0.1790294

sigma^2: 54.8316

AIC AICc BIC

379.8459 380.3914 385.4595

augment (comp_hw1) |> ggplot (aes (x = months, y = complaints)) + geom_line () + geom_line (aes (y = .fitted, color = "Fitted" )) + labs (color = "" )

sum (components (comp_hw1)$ remainder^ 2 , na.rm = T)

<- HoltWinters (Comp.ts, alpha = 0.2 ,beta = FALSE , gamma = FALSE ) # edits to book code $ SSE

<- comp_ts |> model (Additive = ETS (complaints ~ trend ("A" , alpha = 0.2 , beta = 0 ) + error ("A" ) + season ("N" ),opt_crit = "amse" , nmse = 1 ))sum (components (comp_hw2)$ remainder^ 2 , na.rm = T)

Show the Book code in full

#https://rpubs.com/pg2000in/TimeSeries5 <- read.table ("data/motororg.dat" , header = T)# attach(Motor.dat) # bad practice <- ts (Motor.dat$ complaints,start = c (1996 , 1 ),freq = 12 )plot (Comp.ts,xlab = "Time / months" ,ylab = "Complaints" )<- HoltWinters (Comp.ts,beta = FALSE , gamma = FALSE ) # edits to book code plot (Comp.hw1)$ SSE<- HoltWinters (Comp.ts, alpha = 0.2 ,beta = FALSE , gamma = FALSE ) # edits to book code $ SSE

Show the Tidyverts code in full

<- read_table ("data/motororg.dat" ) |> mutate (dates = seq (ymd ("1996-01-01" ), by = "1 months" ,length.out = n ()),months = yearmonth (dates)<- as_tsibble (motor_dat, index = months)autoplot (comp_ts) + labs (x = "Time / months" , y = "Complaints" )<- comp_ts |> model (Additive = ETS (complaints ~ trend ("A" , alpha = 0.1429622 , beta = 0 ) + error ("A" ) + season ("N" ),opt_crit = "amse" , nmse = 1 ))augment (comp_hw1) |> ggplot (aes (x = months, y = complaints)) + geom_line () + geom_line (aes (y = .fitted, color = "Fitted" )) + labs (color = "" )<- comp_ts |> model (Additive = ETS (complaints ~ trend ("A" , alpha = 0.2 , beta = 0 ) + error ("A" ) + season ("N" ),opt_crit = "amse" , nmse = 1 ))sum (components (comp_hw2)$ remainder^ 2 , na.rm = T)

3.4.2 “Holt-Winters” and “Australian wine” Modern Look

Book code

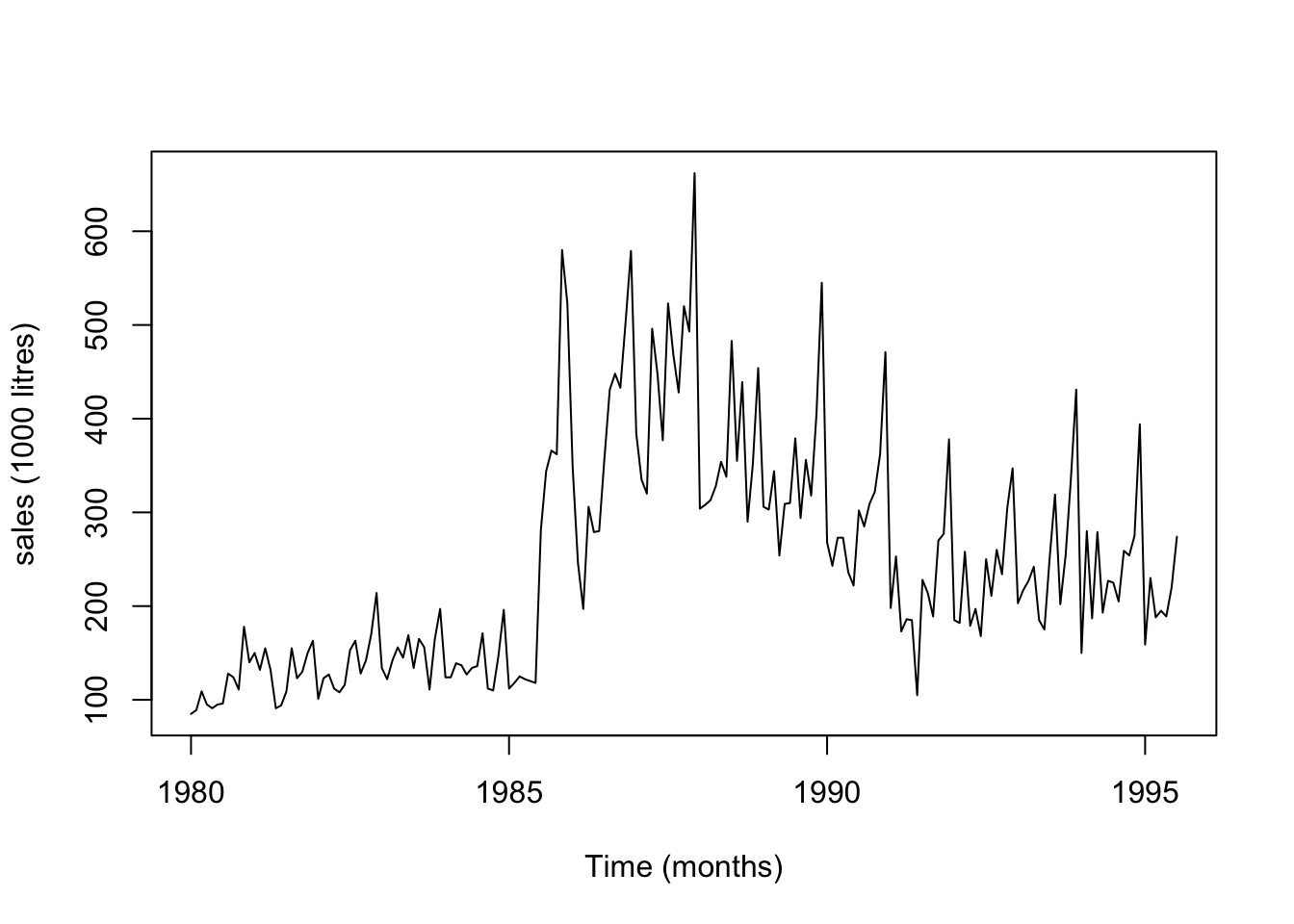

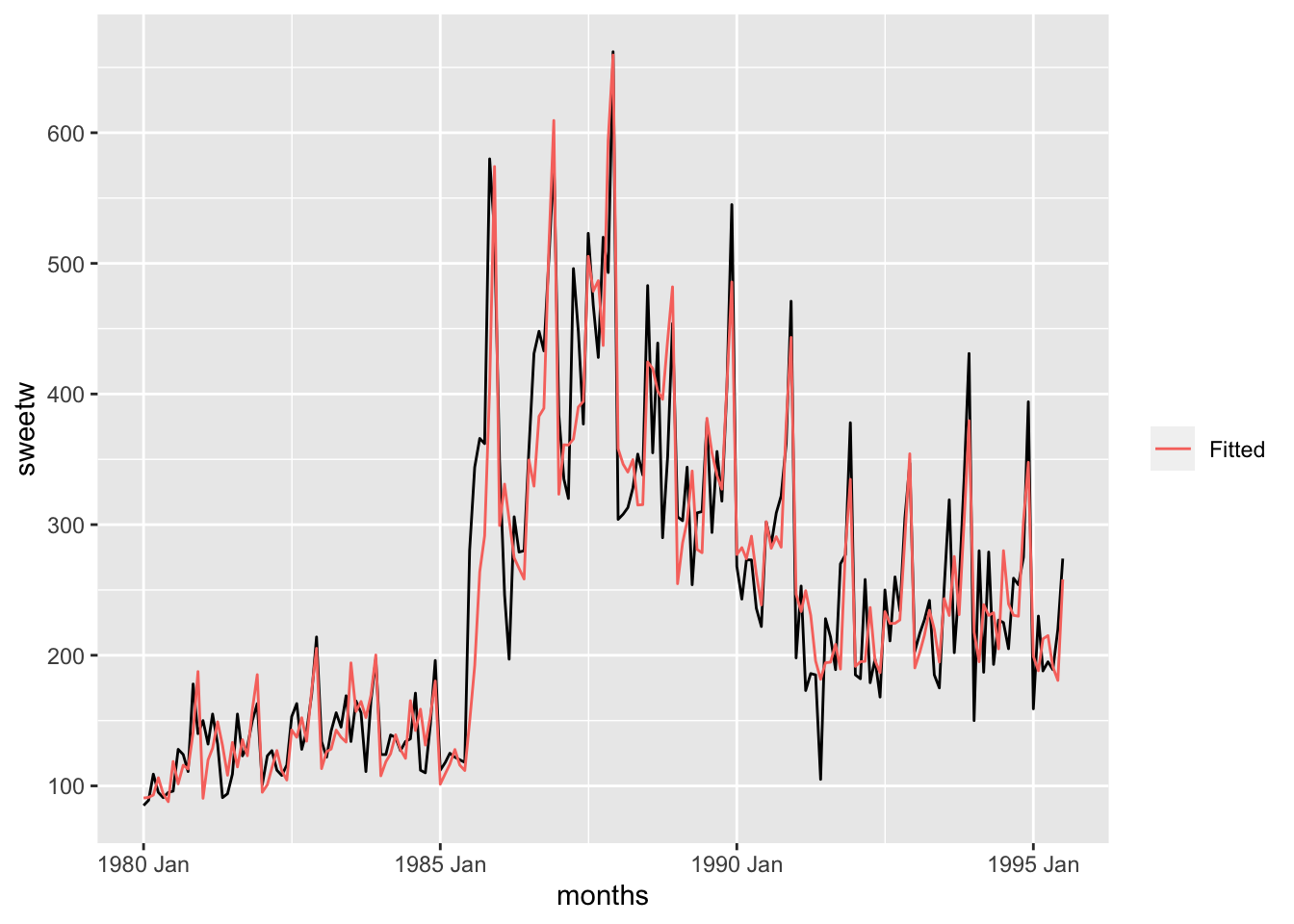

<- read.table ("data/wine.dat" , header = T)# attach (wine.dat) # bad practice <- ts (wine.dat$ sweetw, start = c (1980 ,1 ), freq = 12 )plot (sweetw.ts, xlab= "Time (months)" , ylab = "sales (1000 litres)" )

Tidyverts code

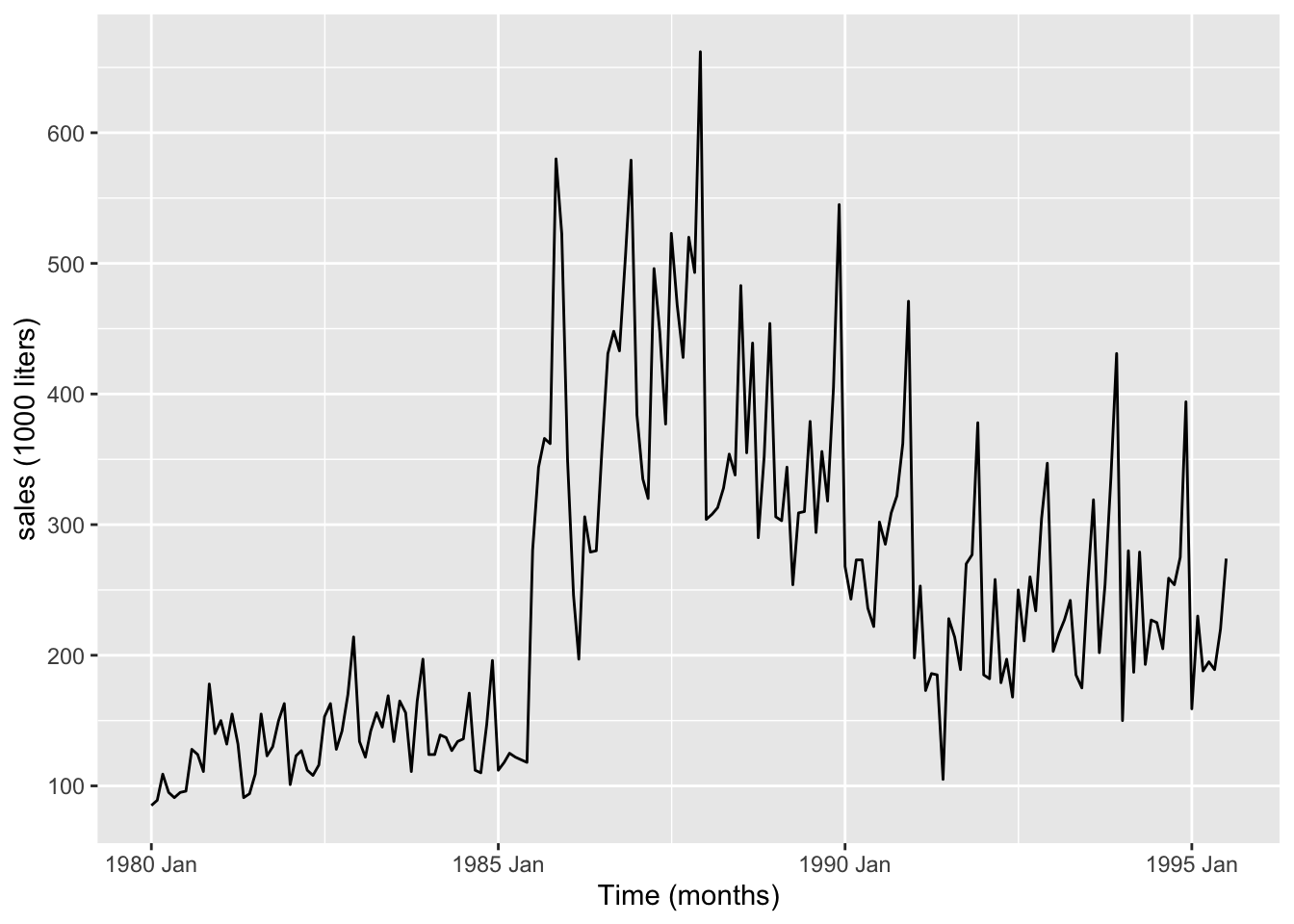

<- read_table ("data/wine.dat" ) |> mutate (dates = seq (ymd ("1980-01-01" ), by = "1 months" ,length.out = n ()),months = yearmonth (dates)<- as_tsibble (select (wine_dat, sweetw, months),index = months)autoplot (sweetw_ts) + labs (x = "Time (months)" ,y = "sales (1000 liters)" )

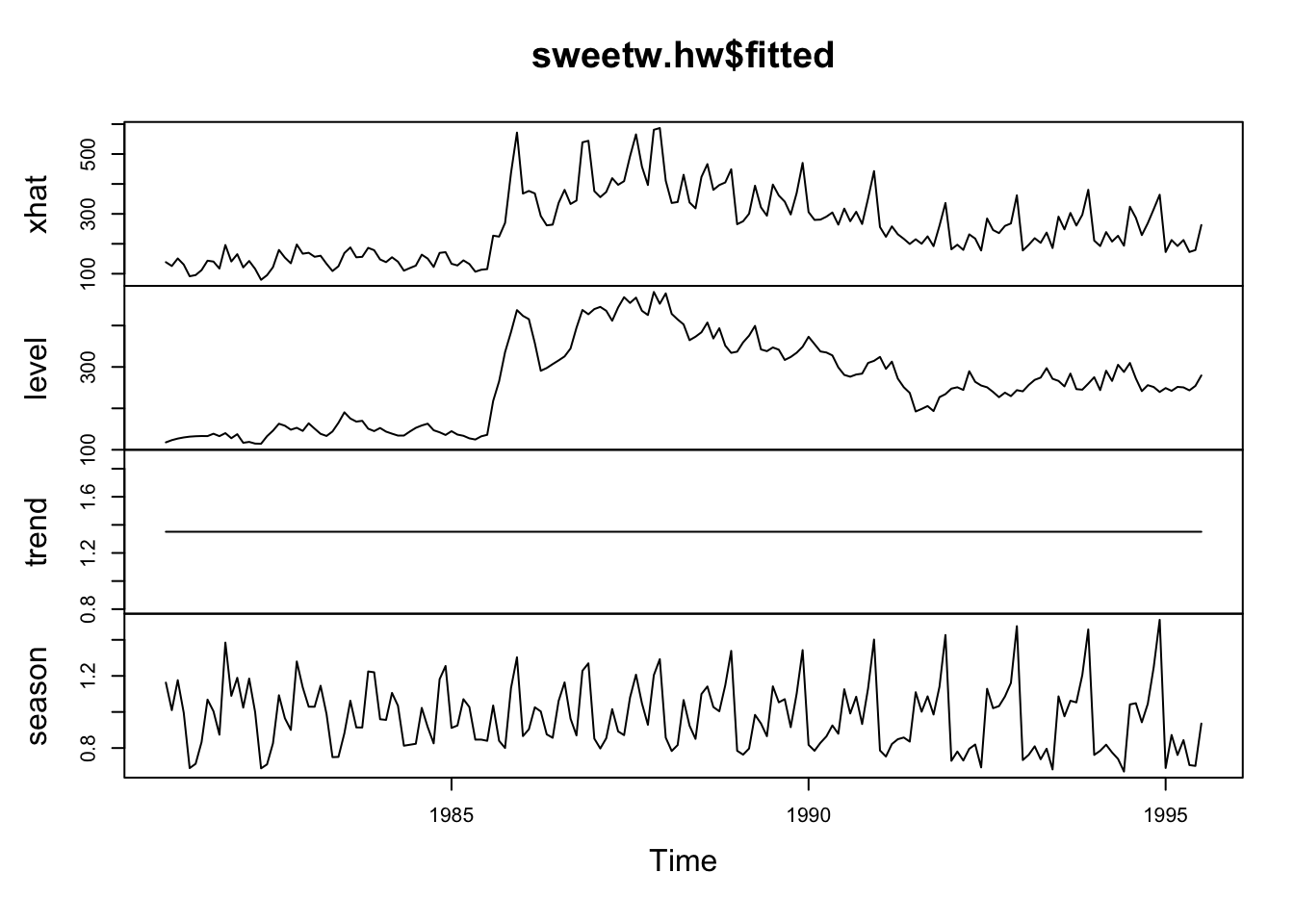

<- HoltWinters (sweetw.ts, seasonal = "multiplicative" ) #not quite the same as book

Holt-Winters exponential smoothing with trend and multiplicative seasonal component.

Call:

HoltWinters(x = sweetw.ts, seasonal = "multiplicative")

Smoothing parameters:

alpha: 0.4086698

beta : 0

gamma: 0.4929402

Coefficients:

[,1]

a 285.6890314

b 1.3509615

s1 0.9498541

s2 0.9767623

s3 1.0275900

s4 1.1991924

s5 1.5463100

s6 0.6730235

s7 0.8925981

s8 0.7557814

s9 0.8227500

s10 0.7241711

s11 0.7434861

s12 0.9472648

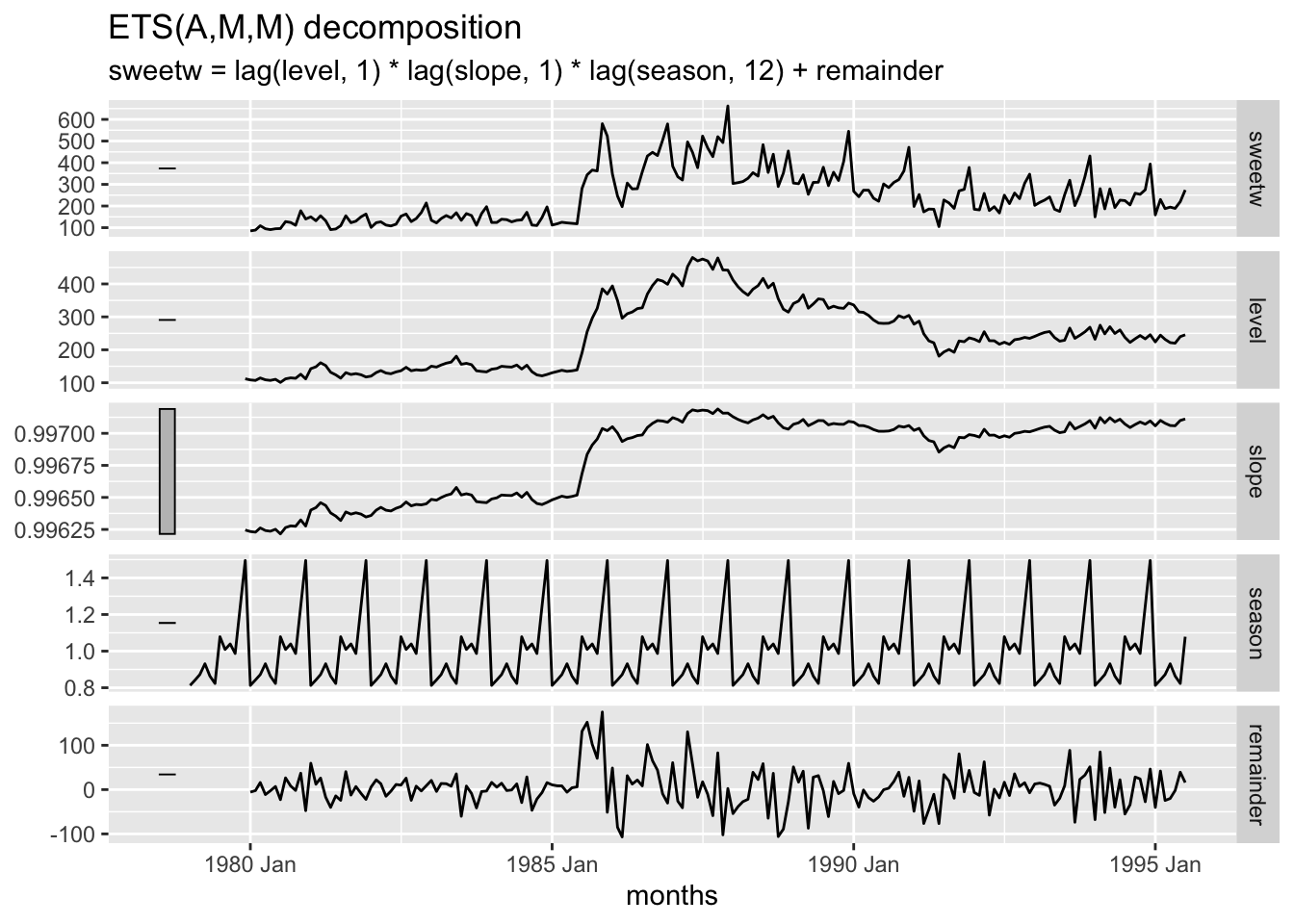

<- sweetw_ts |> model (Multiplicative = ETS (sweetw ~ trend ("M" ) + error ("A" ) + season ("M" ),opt_crit = "amse" , nmse = 1 ))report (sweetw_hw)

Series: sweetw

Model: ETS(A,M,M)

Smoothing parameters:

alpha = 0.4286965

beta = 0.0001905936

gamma = 0.0001968977

Initial states:

l[0] b[0] s[0] s[-1] s[-2] s[-3] s[-4] s[-5]

112.0738 0.9962457 1.495189 1.246035 0.9870751 1.03928 1.008875 1.078576

s[-6] s[-7] s[-8] s[-9] s[-10] s[-11]

0.8232773 0.8637861 0.9308562 0.8717047 0.8427252 0.8126209

sigma^2: 2116.25

AIC AICc BIC

2427.425 2431.046 2482.354

a b s1 s2 s3 s4

285.6890314 1.3509615 0.9498541 0.9767623 1.0275900 1.1991924

s5 s6 s7 s8 s9 s10

1.5463100 0.6730235 0.8925981 0.7557814 0.8227500 0.7241711

s11 s12

0.7434861 0.9472648

# A tibble: 17 × 3

.model term estimate

<chr> <chr> <dbl>

1 Multiplicative alpha 0.429

2 Multiplicative beta 0.000191

3 Multiplicative gamma 0.000197

4 Multiplicative l[0] 112.

5 Multiplicative b[0] 0.996

6 Multiplicative s[0] 1.50

7 Multiplicative s[-1] 1.25

8 Multiplicative s[-2] 0.987

9 Multiplicative s[-3] 1.04

10 Multiplicative s[-4] 1.01

11 Multiplicative s[-5] 1.08

12 Multiplicative s[-6] 0.823

13 Multiplicative s[-7] 0.864

14 Multiplicative s[-8] 0.931

15 Multiplicative s[-9] 0.872

16 Multiplicative s[-10] 0.843

17 Multiplicative s[-11] 0.813

sum (components (sweetw_hw)$ remainder^ 2 , na.rm = T)

sqrt (sweetw.hw$ SSE/ length (wine.dat$ sweetw)) # book has 50.04

autoplot (components (sweetw_hw))

augment (sweetw_hw) |> ggplot (aes (x = months, y = sweetw)) + geom_line () + geom_line (aes (y = .fitted, color = "Fitted" )) + labs (color = "" )

Show the Book code in full

# https://otexts.com/fpp2/holt-winters.html <- read.table ("data/wine.dat" , header = T)# attach (wine.dat) # bad practice <- ts (wine.dat$ sweetw, start = c (1980 ,1 ), freq = 12 )plot (sweetw.ts, xlab= "Time (months)" , ylab = "sales (1000 litres)" )<- HoltWinters (sweetw.ts, seasonal = "multiplicative" ) #not quite the same as book $ coef$ SSEsqrt (sweetw.hw$ SSE/ length (wine.dat$ sweetw)) # book has 50.04 sd (wine.dat$ sweetw)plot (sweetw.hw$ fitted)plot (sweetw.hw)

Show the Tidyverts code in full

<- read_table ("data/wine.dat" ) |> mutate (dates = seq (ymd ("1980-01-01" ), by = "1 months" ,length.out = n ()),months = yearmonth (dates)<- as_tsibble (select (wine_dat, sweetw, months),index = months)autoplot (sweetw_ts) + labs (x = "Time (months)" ,y = "sales (1000 liters)" )<- sweetw_ts |> model (Multiplicative = ETS (sweetw ~ trend ("M" ) + error ("A" ) + season ("M" ),opt_crit = "amse" , nmse = 1 ))report (sweetw_hw)tidy (sweetw_hw)sum (components (sweetw_hw)$ remainder^ 2 , na.rm = T)accuracy (sweetw_hw)$ RMSEsd (sweetw_ts$ sweetw)autoplot (components (sweetw_hw))augment (sweetw_hw) |> ggplot (aes (x = months, y = sweetw)) + geom_line () + geom_line (aes (y = .fitted, color = "Fitted" )) + labs (color = "" )

3.4.3 “Four-year-ahead forecasts” and “air passenger data” Modern Look

Book code

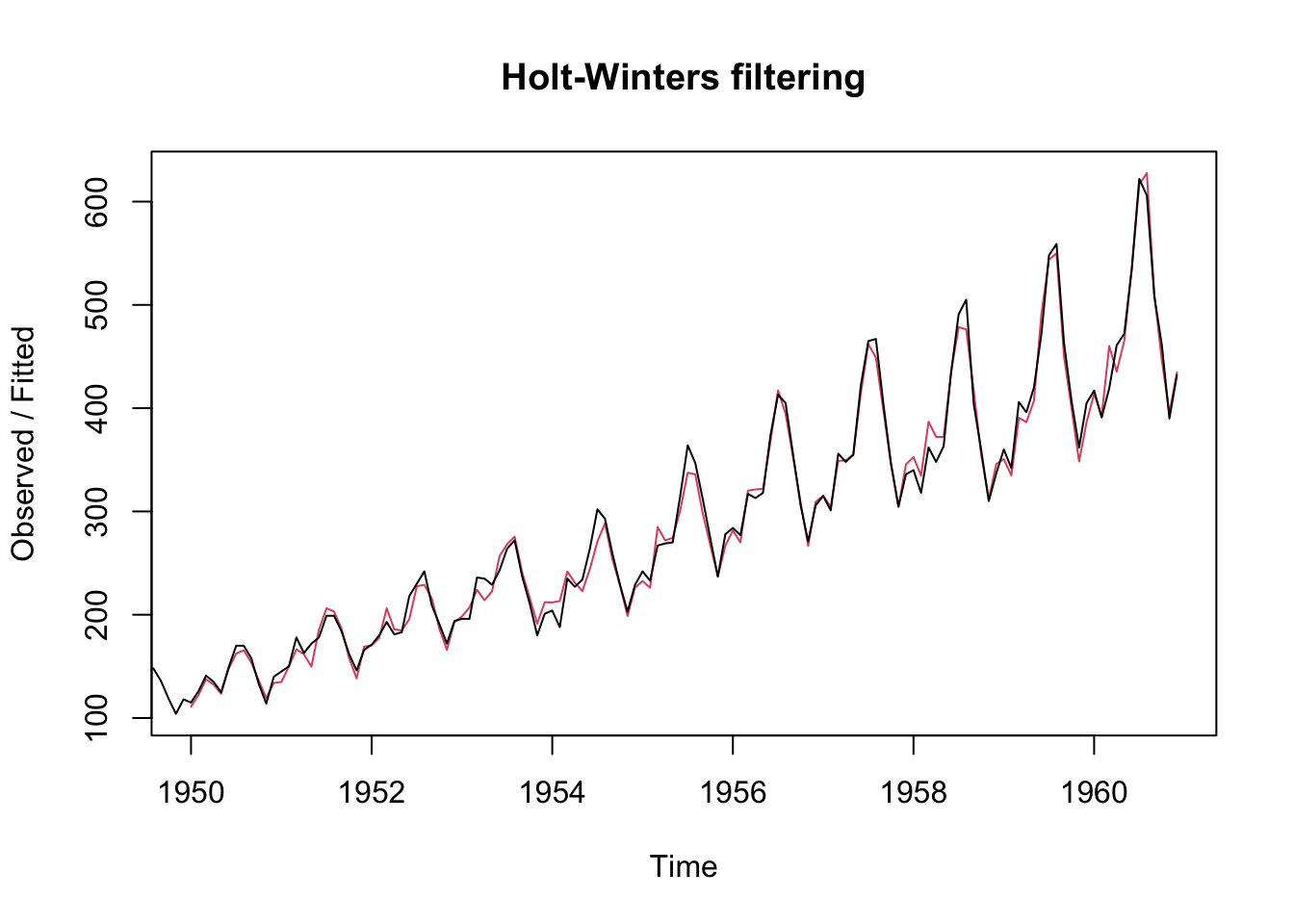

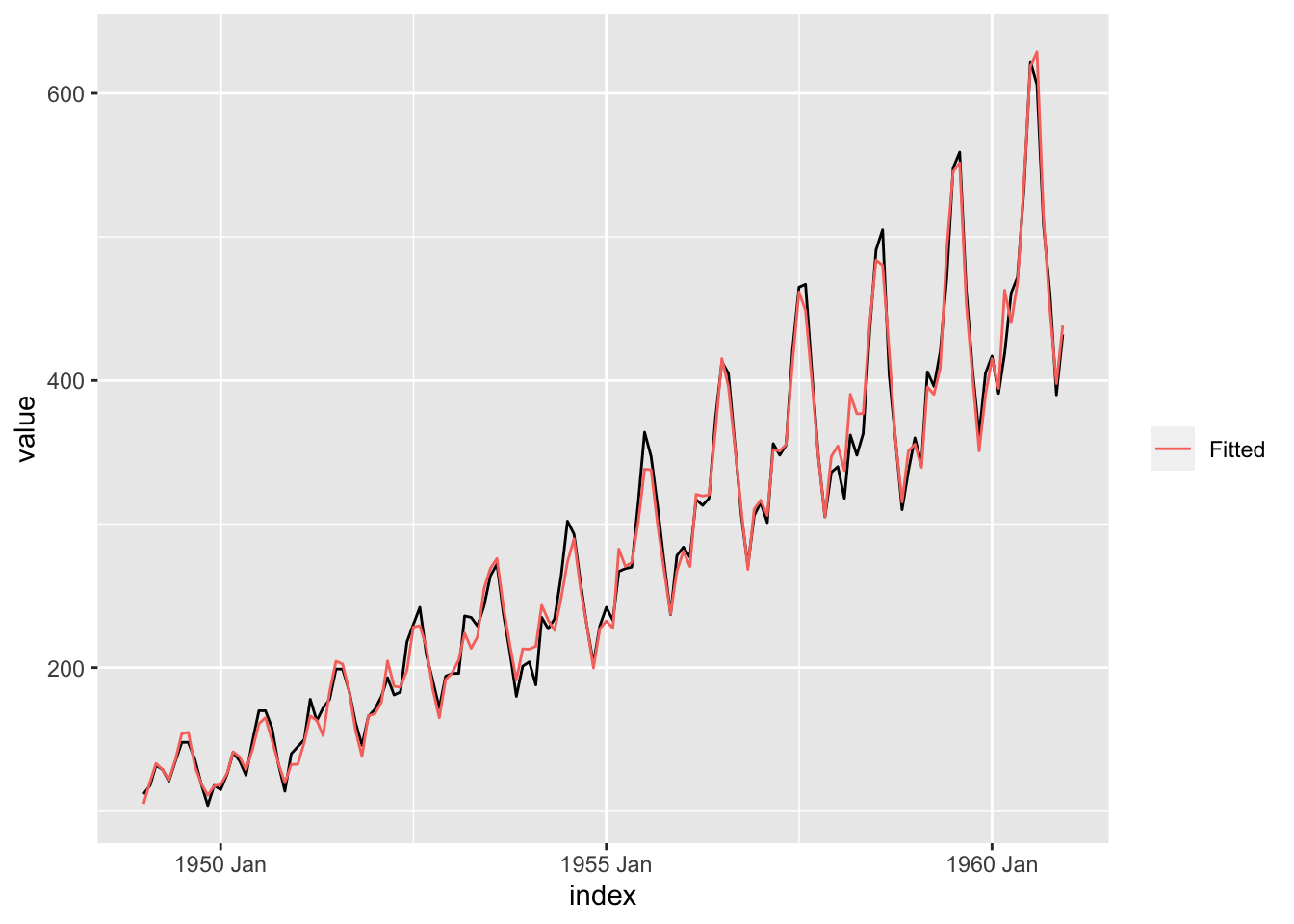

data (AirPassengers)<- AirPassengers<- HoltWinters (AP, seasonal = "mult" )plot (AP.hw)

Tidyverts code

data (AirPassengers)<- as_tsibble (AirPassengers) |> mutate (Year = year (index),Month = month (index)<- ap |> model (Multiplicative = ETS (value ~ trend ("M" ) + error ("A" ) + season ("M" ),opt_crit = "amse" , nmse = 1 ))augment (ap_hw) |> ggplot (aes (x = index, y = value)) + geom_line () + geom_line (aes (y = .fitted, color = "Fitted" )) + labs (color = "" )

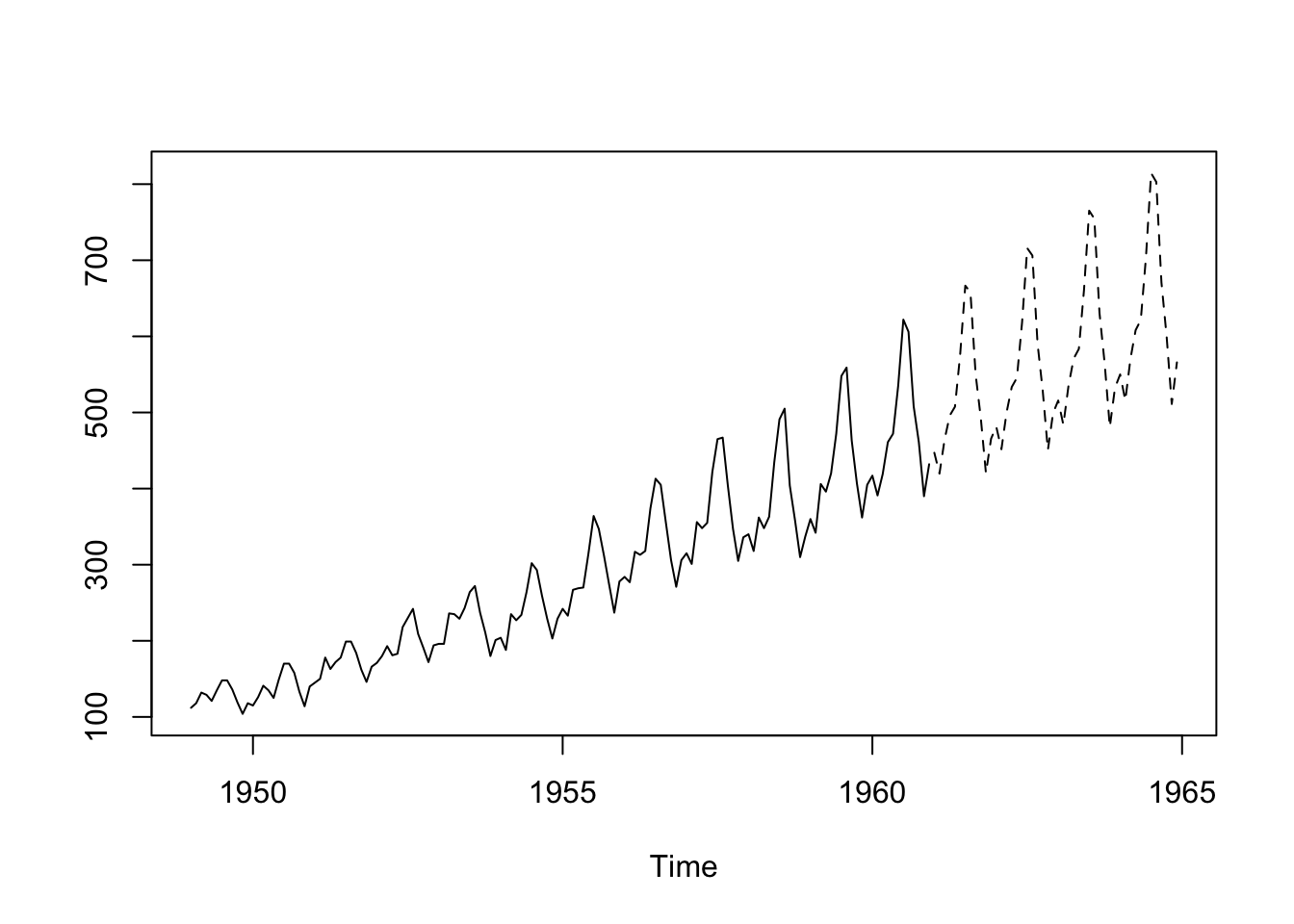

<- predict (AP.hw, n.ahead = 4 * 12 )ts.plot (AP, AP.predict, lty = 1 : 2 )

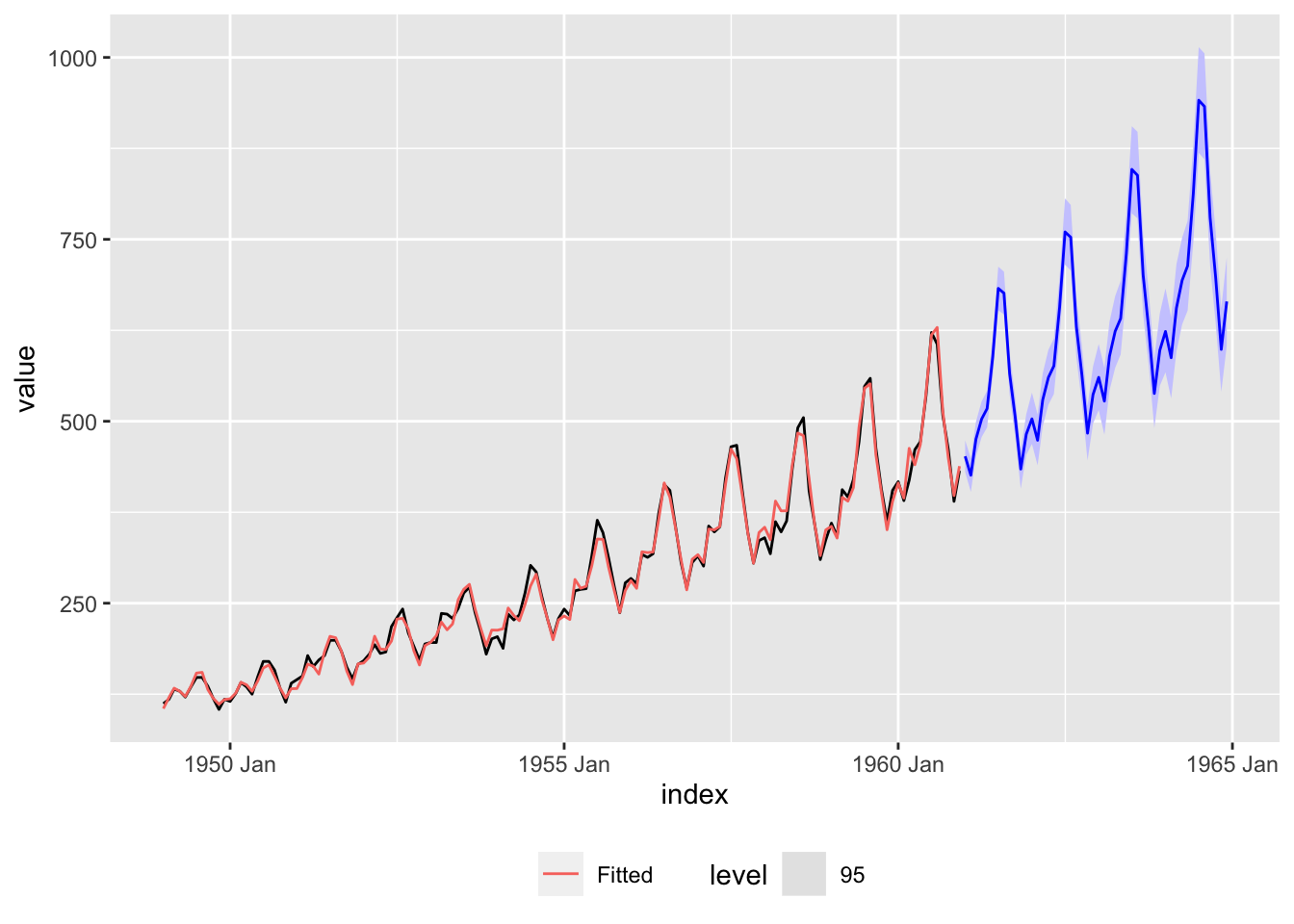

|> forecast (h = "4 years" ) |> autoplot (ap, level = 95 ) + geom_line (aes (y = .fitted, color = "Fitted" ),data = augment (ap_hw)) + scale_color_discrete (name = "" ) + theme (legend.position = "bottom" )

Show the Book code in full

data (AirPassengers)<- AirPassengers<- HoltWinters (AP, seasonal = "mult" )plot (AP.hw)<- predict (AP.hw, n.ahead = 4 * 12 )ts.plot (AP, AP.predict, lty = 1 : 2 )

Show the Tidyverts code in full

data (AirPassengers)<- as_tsibble (AirPassengers) |> mutate (Year = year (index),Month = month (index)<- ap |> model (Multiplicative = ETS (value ~ trend ("M" ) + error ("A" ) + season ("M" ),opt_crit = "amse" , nmse = 1 ))augment (ap_hw) |> ggplot (aes (x = index, y = value)) + geom_line () + geom_line (aes (y = .fitted, color = "Fitted" )) + labs (color = "" )|> forecast (h = "4 years" ) |> autoplot (ap, level = 95 ) + geom_line (aes (y = .fitted, color = "Fitted" ),data = augment (ap_hw)) + scale_color_discrete (name = "" )

3.5 Summary of Modern R commands used in examples